Scheduled outage for OSC Electronic Filing Portal on Thursday, April 25, 2024 from 6:00 to 11:00 pm (EST)

Request for Comments – Material Amendments to CDS Procedures – Real Time CNS Settlement and CNS Settlement Hold – CDS Clearing and Depository Services Inc.

A. DESCRIPTION OF THE PROPOSED CDS PROCEDURE AMENDMENTS

The proposed CDS procedure amendments are intended to address the replacement of the intraday continuous net settlement (CNS) settlement cycles with a real-time CNS settlement process and the implementation of CNS settlement hold functionality.

Currently, CDS's procedures contain information related to the intraday CNS settlement cycles that run at approximately 10:00, 12:00, 14:00 and 15:30 ET. This information will be replaced with information related to the real-time CNS settlement process that will run from system start-up through to the start of payment exchange and information related to CNS settlement hold functionality will be added to CDS's procedures.

B. NATURE AND PURPOSE OF THE PROPOSED CDS PROCEDURE AMENDMENTS

Current intraday CNS settlement cycles are scheduled to run four times each day, with the last cycle running at 15:30 ET. This leaves half an hour between the last intraday CNS settlement cycle and the time that real-time trade-for-trade (TFT) settlement versus payment ends (i.e. 16:00 ET).

This limitation relative to the opportunity to use positions received through the last CNS settlement cycle to facilitate real-time TFT settlement (or vice-versa) may expose participants to settlement and financial risk, such as collateral and capital charges and unexpected cash outlays, as well as added costs to mitigate such risks.

The Debt & Equity Subcommittee of CDS's Strategic Development Review Committee requested a solution to this timing issue between the CNS and TFT modes of settlement.

CDS's proposed solution entails replacing the intraday CNS settlement cycles with a real-time CNS settlement process, and introducing CNS settlement Hold functionality.

The purpose of the proposed CDS procedure amendments is to provide participants with information related to the systemic changes that are required to replace the intraday CNS settlement cycles with the real-time CNS settlement process and CNS settlement Hold functionalities.

C. IMPACT OF THE PROPOSED CDS PROCEDURE AMENDMENTS

The following is a list of identified impacts to participants and/or their service bureaus:

• The limitations posed by the four current intraday CNS settlement cycles will be eliminated as the real-time CNS settlement process will run continuously from system start-up through to the start of payment exchange:

• When a TFT trade (buy) settles between 15:30 and 16:00 ET that position may be used to settle an outstanding-to -deliver CNS position

• When an outstanding-to-receive CNS position settles between 15:30 and 16:00 ET that position may be used to settle a TFT trade (sell)

• An additional half-hour will be available to deliver positions to CNS in order to reduce or eliminate CNS buy-in liabilities before the final buy-in execution list is generated at 14:30 ET (currently the last intraday CNS settlement cycle prior to the generation of the final buy-in execution list runs at approximately 14:00 ET)

• CNS buy-in update notification messages will be received throughout the day as outstanding CNS buy-ins are affected by the real-time CNS settlement process rather than at the conclusion of each of the intraday CNS settlement cycles, as is the case today

• CNS settlement activity may increase (e.g. increase in CNS settlement and CNS buy-in notification messages), resulting in increased CNS settlement costs

• The new Hold CNS functionality (i.e. the ability to change the settlement control indicator from 'Y' to 'N' or vice-versa on outstanding-to-deliver CNS positions) will allow for prioritization according to settlement and/or funding needs (currently participants are only able to place holds on TFT trades)

• Participant or Service Bureau development will be required in order to generate/send CNS position -- Settlement Control Indicator Interlink messages to CDS and process CNS position -- Settlement Control Indicator messages received from CDS

Note: There will be no impact to the BNS/CNS process or to the CNS extraction, netting and mark-to-market processes. However, CNS settlement will not occur when the intraday CNS netting process runs at approximately 13:00 ET.

C.1 Competition

N/A -- CDS is the only provider of securities settlement services in Canada.

C.2 Risks and Compliance Costs

N/A -- No new risks or compliance costs were identified.

C.3 Comparison to International Standards -- (a) Committee on Payment and Settlement Systems of the Bank for International Settlements, (b) Technical Committee of the International Organization of Securities Commissions, and (c) the Group of Thirty

The Group of Thirty's Recommendation 4 states "Synchronize timing between different clearing and settlement systems and associated payment and foreign exchange systems".

Moving to a real-time CNS settlement process will be in keeping with this recommendation as CDS's CNS settlement process will be more closely synchronized with NSCC's CNS settlement process.

No other comparisons to international standards were identified.

D. DESCRIPTION OF THE PROCEDURE DRAFTING PROCESS

D.1 Development Context

CDS's participant procedures were reviewed by CDS staff and references to CNS settlement were identified. Proposed amendments to the procedures related to the replacement of the intraday CNS settlement cycles with a real-time CNS settlement process and the introduction of CNS settlement hold functionality were then incorporated within the existing CDS's participant procedures. The proposed amendments to CDS's participant procedures were then approved by CDS management.

D.2 Procedure Drafting Process

CDS Procedure Amendments are reviewed and approved by CDS's Strategic Development Review Committee ("SDRC"). The SDRC determines or reviews, prioritizes and oversees CDS-related systems development and other changes proposed by participants and CDS. The SDRC's membership includes representatives from the CDS Participant community and it meets on a monthly basis.

These amendments were reviewed and approved by the SDRC on March 24, 2011.

D.3 Issues Considered

N/A - No issues were identified.

D.4 Consultation

The Debt & Equity Subcommittee of the SDRC has been kept apprised of the status of the Real-time CNS Settlement and CNS Settlement Hold project and CDS bulletins related to the project will be released.

D.5 Alternatives Considered

The following alternatives were considered:

• Scheduling an additional BNS/CNS cycle prior to payment exchange

• Allowing participants to deliver securities into CNS to cover outstanding CNS positions

While these options would address the timing issue faced by participants in part, the members of the Debt & Equity Subcommittee of the SDRC preferred moving to a real-time CNS settlement process and implementing CNS settlement hold functionality as this solution would more effectively address the timing issue.

D.6 Implementation Plan

CDS is recognized as a clearing agency by the Ontario Securities Commission pursuant to section 21.2 of the Ontario Securities Act. The Autorité des marchés financiers has authorized CDS to carry on clearing activities in Québec pursuant to sections 169 and 170 of the Québec Securities Act. In addition CDS is deemed to be the clearing house for CDSX®, a clearing and settlement system designated by the Bank of Canada pursuant to section 4 of the Payment Clearing and Settlement Act. The Ontario Securities Commission, the Autorité des marchés financiers and the Bank of Canada will hereafter be collectively referred to as the "Recognizing Regulators".

The amendments to Participant Procedures may become effective upon approval of the amendments by the Recognizing Regulators following public notice and comment.

E. TECHNOLOGICAL SYSTEMS CHANGES

E.1 CDS

Technological system changes are required by CDS in order to replace the intraday CNS settlement cycles with a real-time CNS settlement process and introduce CNS settlement hold functionality.

The required technological system changes will follow CDS's system development life-cycle (SDLC) protocol.

E.2 CDS Participants

Technological system changes would be required by CDS Participants in order to accommodate the new inbound/outbound CNS position settlement control indicator Interlink messages.

E.3 Other Market Participants

Technological system changes would be required by CDS Participant service bureaus in order to accommodate the new inbound/outbound CNS position settlement control indicator Interlink messages (i.e. Hold messages).

F. COMPARISON TO OTHER CLEARING AGENCIES

CNS settlement at NSCC occurs in the evening (batch process) and throughout the day in real-time (i.e. from 07:00 - 15:10 ET).

Moving to a real-time CNS settlement process that will run from system start-up to payment exchange will align CDS's CNS settlement process with NSCC's CNS settlement process.

G. PUBLIC INTEREST ASSESSMENT

CDS has determined that the proposed amendments are not contrary to the public interest.

H. COMMENTS

Comments on the proposed amendments should be in writing and submitted within 30 calendar days following the date of publication of this notice in the Ontario Securities Commission Bulletin to:

Rob Argue

Senior Product Manager, Business Systems Development and Support

CDS Clearing and Depository Services Inc.

85 Richmond Street West

Toronto, Ontario M5H 2C9

Phone: 416-365-3887

Fax: 416-365-0842

Email: [email protected]

Copies should also be provided to the Autorité des marchés financiers and the Ontario Securities Commission by forwarding a copy to each of the following individuals:

Me Anne-Marie Beaudoin

Manager, Market Regulation

Secrétaire del'Autorité

Capital Markets Branch

Autorité des marchés financiers

Ontario Securities Commission

800, square Victoria, 22e étage

Suite 1903, Box 55,

C.P. 246, tour de la Bourse

20 Queen Street West

Montréal (Québec) H4Z 1G3

Toronto, Ontario, M5H 3S8

Télécopieur: (514) 864-6381

Fax: 416-595-8940

Courrier électronique: [email protected]

e-mail: [email protected]

CDS will make available to the public, upon request, all comments received during the comment period.

I. PROPOSED CDS PROCEDURE AMENDMENTS

Attached at Appendix A are the clean and blacklined versions of the proposed procedural amendments.

Access the proposed amendments to the CDS Procedures on the User documentation revisions web page (http://www.cds.ca/cdsclearinghome.nsf/Pages/-EN-blacklined?Open) and to the CDS Forms (if applicable) on Forms online (Click View by Form Category and in the Select a Form Category list, click External review) on the CDS Services web page (www.cdsservices.ca).

"APPENDIX A"

CHAPTER 1 INTRODUCTION TO TRADE AND SETTLEMENT

Settling trades in CDSX

1.4.1 Trade and settlement cutoff times

The start and cutoff times for trade and settlement activities are indicated in the table below.

Trade and settlement activities in CDSX

ET

MT

PT

Trade reporting and management{1}

7:00 a.m. -

5:00 a.m. -

4:00 a.m. -

Settle trades targeted to settle by TFT settlement through real-time settlement processes

4:00 p.m.{2}

2:00 p.m.

1:00 p.m.

FINet real-time trade settlement

No settlement of FINet netted trades or FINet eligible trades during FINet intraday netting

Settle outstanding CNS positions through real- time settlement processes

No CNS real-time settlement during CNS intraday netting

During payment exchange, security settlement and the

4:00 p.m. -

2:00 p.m. -

1:00 p.m. -

restricted (ACV) TFT settlement occur

5:00 p.m.

3:00 p.m.

2:00 p.m.

No FINet real-time trade settlement

No CNS real-time settlement

After payment exchange, only security TFT settlement

5:00 p.m. -

3:00 p.m. -

2:00 p.m. -

occurs and the ACV edit is no longer applied{1}

7:30 p.m.

5:30 p.m.

4:30 p.m.

No FINet real-time trade settlement

No CNS real-time settlement

System shutdown

7:30 p.m.

5:30 p.m.

4:30 p.m.

Overnight online activity processing of TFT transactions{1}

12:30 a.m. -

10:30 p.m. -

9:30 p.m. -

4:00 a.m.

2:00 a.m.

1:00 a.m.

FINet real-time trade settlement

No CNS real-time settlement

CNS/BNS process

Starts at

Starts at

Starts at

4:00 a.m.

2:00 a.m.

1:00 a.m.

{1} These times may vary depending on the progress of the batch schedule.

{2} Start of payment exchange

CDSX runs separate payment exchanges for Canadian and U.S. dollar activities. Both payment exchanges are expected to start at 4:00 p.m. ET (2:00 p.m. MT, 1:00 p.m. PT). However, for various reasons, the start and end of the payment exchanges may be altered for one or both currencies.

CHAPTER 8

Settlement of trades

Trades are settled in CDSX in one of the modes of settlement indicated in the table below.

For information on the settlement of FINet trades, see FINet real-time settlement on page 50.

Mode of settlement

Description

Trade-for-trade (TFT) settlement

Trades targeted to settle by TFT are settled on an individual basis

Continuous net settlement (CNS)

Trades targeted to settle by CNS that have reached value date are netted daily with outstanding unsettled or partially settled quantities. The positions involved in these trades must be held in the participant's general account, in order to be considered for settlement

Unsettled quantities (i.e., "fails") are maintained by CDSX as outstanding positions. The seller has the to-deliver position and the buyer has the to-receive position for the quantities that have not settled. CDSX maintains CNS outstanding positions by ledger, security, currency and clearing organization

Trades reported to CDSX with certificate-based settlement (CBS) as the mode of settlement are not considered for settlement.

It is the participant's responsibility to manage their positions in their general account (GA000) If participants do not want shares in a certain security to settle in CNS, they must do one of the following:

• Remove the position from their general account prior to the start of the CNS/BNS Process

• Remove the position from their general account during the day when the real-time CNS settlement process is running

• Place outstanding to deliver positions on hold.

ACV edit on settlement

CDSX supports both Canadian dollar and U.S. dollar settlement.

The aggregate collateral value (ACV) edit is applied up to the end of the Canadian dollar payment exchange period only. During the payment exchange period, a modified ACV edit is applied. Once payment exchange is complete, the ACV edit is not applied. For more information, refer to Participating in CDS Services.

CHAPTER 8 SETTLEMENT OF TRADES

Settlement cutoff times

8.1 Settlement cutoff times

The cutoff times for settlement activities are indicated in the table below. If necessary, CDS sends a broadcast message to all participants to inform them of any changes in cutoff times.

Settlement activities

ET

MT

PT

Real-time TFT settlement{1}

7:00 a.m. -

5:00 a.m. -

4:00 a.m. -

7:30 p.m.

5:30 p.m.

4:30 p.m.

Real-time CNS settlement

7:00 a.m. -

5:00 a.m. -

4:00 a.m. -

No CNS real-time settlement during CNS intraday netting

4:00 p.m.

2:00 p.m.

1:00 p.m.

Restricted TFT settlement period

4:00 p.m. -

2:00 p.m. -

1:00 p.m. -

7:30 p.m.

5:30 p.m.

4:30 p.m.

Real-time TFT settlement{1}

12:30 a.m. -

10:30 p.m. -

9:30 p.m. -

4:00 a.m.

2:00 a.m.

1:00 a.m.

CNS/BNS process

Starts at

Starts at

Starts at

4:00 a.m.

2:00 a.m.

1:00 a.m.

{1} These times may vary depending on the progress of the batch schedule.

8.2 Restricted TFT settlement

At the start of payment exchange, CDSX no longer settles Canadian and U.S. dollar funds. The restriction is placed on Canadian dollar TFT settlements during the Canadian payment exchange period, and U.S. dollar settlements during the U.S. payment exchange period.

If a pending TFT trade affects a ledger that has holiday settlement restrictions, the status of the TFT trade is changed from pending to confirmed on the restriction date.

If a funds holiday settlement restriction exists for a ledger and the pending TFT trade does not involve funds, the status of the TFT trade remains pending until the transaction settles.

8.3 Real-time TFT settlement

CDSX provides a real-time settlement facility for trades targeted to settle by TFT. Settlement occurs when the trade meets the settlement criteria. This settlement facility continually evaluates trades based on the changing circumstances of the participants in the trades.

When evaluating trades targeted to settle by TFT, CDSX does one of following:

• Settles the trade

• Leaves the trade in a confirmed status but does not settle it

• Assigns a pending settlement status (see Pending trades on page 74).

The table below indicates the settlement criteria for trades targeted to settle by TFT. All of the settlement criteria must be met for CDSX to process the trades.

Settlement criteria for trades targeted to settle by TFT

The trade will be considered for settlement if . . .

The trade will settle if . . .

The trade is confirmed

__________

__________

The trade has reached value date

__________

__________

Both participants' settlement control indicators are set to Y

__________

__________

Neither party is suspended

__________

__________

Neither party has a holiday settlement restriction placed on their ledger

__________

__________

The security is CDSX-eligible

__________

__________

The seller has sufficient ledger position in the security in the trade

__________

__________

The buyer has sufficient available funds in the currency of the trade

__________

__________

Both the buyer and the seller have sufficient ACV

__________

__________

8.3.1 Pending trades

When CDSX assigns a pending status to a TFT trade, a two-character pending reason code displays in the STATUS field. The first character identifies the party at fault (B for buyer, S for seller) and the second identifies the reason why the transaction is pending (S for insufficient securities, F for insufficient funds or C for insufficient ACV).

Pending transactions are reconsidered for settlement if the participant's circumstances change and settlement conditions are met.

8.4 CNS/BNS process

The CNS/BNS process is a batch net settlement process that increases settlement efficiency by combining the settlement of trades targeted to settle by CNS and TFT. The goal of the combined process is to allow CNS and TFT activities to net against each other and to reduce a participant's requirements for security positions, funds, cap, credit and collateral.

The CNS/BNS process occurs once per day after the overnight online period and is currently scheduled to execute around 4:00 a.m. ET (2:00 a.m. MT, 1:00 a.m. PT).

CHAPTER 8 SETTLEMENT OF TRADES

CNS/BNS Process

8.4.1 CNS trade extraction and netting for settlement

CDSX extracts trades that are targeted to settle by CNS based on the following extraction criteria:

• Exchange and non-exchange trades are considered

• The mode of settlement is CNS

• The trade status is C

• The value date is less than or equal to the current business date

• There is no CDS holiday settlement restriction for the currency of the trade

• The security is eligible for CNS

• The participants' ledgers are not suspended.

If the extraction criteria is met, the trade is netted, marked and considered for settlement by CNS.

CDS may "allot" a trade to settle by TFT if the trade is not extracted due to the following:

• The security is not eligible to settle by CNS

• Either participant is not eligible for the CNS service

• Either participant's ledger is suspended.

Once extracted, CNS trades are marked and netted with current CNS outstanding positions. Once netted, the new outstanding positions are also marked. Marks are applied directly against the deliverer's and receiver's funds accounts.

Note: Lines of credit and/or caps are not drawn upon for negative marks being applied.

8.4.2 Settlement during the CNS/BNS process

If the conditions for settlement are met, the CNS/BNS process attempts settlement based on defined settlement priority. The conditions for settlement are the same as those for real-time TFT and CNS settlement.

To review the conditions for settlement, see Settlement criteria for trades targeted to settle by TFT on page 74 and Settlement criteria for real-time continuous net settlement on page 76.

The settlement priority for the CNS/BNS process is as follows:

• Domestic U.S. dollar TFT trades flagged as mandatory cash from TSX

• Domestic Canadian dollar TFT trades flagged as mandatory cash from TSX

• DTCC Canadian dollar TFT settlement

• Domestic Canadian dollar TFT settlement

• Domestic U.S. dollar CNS to-receive positions with buy-ins

• Domestic Canadian dollar CNS to-receive positions with buy-ins

• Domestic U.S. dollar CNS outstanding positions

• Domestic Canadian dollar CNS outstanding positions.

During the CNS/BNS process, CNS positions settle entirely or partially, and trades targeted to settle by TFT settle entirely or are made pending.

8.5 Real-time CNS settlement process

Unlike the CNS/BNS process, which processes trades targeted to settle by TFT and CNS together, the real-time CNS settlement process only processes outstanding CNS positions. This process runs throughout the business day and executes independently of the real-time TFT settlement process.

Once CDSX determines that the criteria for CNS settlement have been met (see Settlement criteria for real-time continuous net settlement on page 76), the real-time CNS settlement facility attempts to settle outstanding CNS positions based on the following settlement priority:

• Domestic U.S. dollar CNS to-receive positions with buy-ins

• Domestic Canadian dollar CNS to-receive positions with buy-ins

• Domestic U.S. dollar CNS outstanding positions

• Domestic Canadian dollar CNS outstanding positions.

Since real-time CNS settlement executes while other online settlement functions are also processing, the settlement priority noted above cannot be guaranteed.

CDSX maintains the buy-in priority, which ensures that participants who have been bought in can only deliver to receivers with a buy-in position. The buy-in priority is maintained throughout the day.

8.5.1 Settlement criteria for real-time continuous net settlement

The following criteria must be met for CNS to consider settlement of outstanding positions:

• Both the deliverer and receiver are eligible for the CNS service

• The security is CNS-eligible

• Both participants are not suspended

• Both participants do not have holiday settlement restrictions placed on their ledger

• The outstanding to deliver position is not on hold.

CHAPTER 8 SETTLEMENT OF TRADES

Calculating CNS marks

Settlement or partial settlement occurs if:

• Sellers have all or some ledger positions in the security for which they are in a to-deliver position

• Buyers have sufficient available funds to accept all or some of the delivery for which they are in a to-receive position

• Both the deliverer and receiver have sufficient ACV to deliver or receive all or some of the delivery.

8.5.2 Intraday marking of CNS outstanding positions

CDSX provides a facility to re-mark CNS outstanding positions intraday in the following circumstances:

• Current value trades are extracted intraday

• Intraday market prices change sufficiently to warrant revaluation of outstanding positions.

8.5.3 Intraday extraction, marking and netting of CNS trades

CDSX provides a facility to extract current value trades that are targeted to settle by CNS. Intraday extraction, netting and marking is executed if CNS-eligible trades are settled in a same-day environment. When trade extraction is executed intraday, the intraday marking of outstanding positions also occurs.

Intraday extraction may also be scheduled or executed on an ad hoc basis.

8.6 Calculating CNS marks

CDSX applies marking calculations to CNS trades and outstanding CNS positions.

Trades

The mark difference on a CNS trade is calculated as follows:

- - - - - - - - - - - - - - - - - - - -

(Marking price -- Trade price)

Quantity x

____________________

Units

- - - - - - - - - - - - - - - - - - - -

The value of units varies depending on whether the trade is equity or debt based. For equity, units is equal to one. For debt, units is equal to 100.

If the mark difference exceeds two decimal places, the value is truncated to two decimal places.

CHAPTER 8 SETTLEMENT OF TRADES

Monitoring settlements using CDSX

Outstanding CNS positions

The mark difference on an outstanding CNS position is calculated as follows:

- - - - - - - - - - - - - - - - - - - -

(Marking price -- Previous marking price)

Quantity x

____________________

Units

- - - - - - - - - - - - - - - - - - - -

The value of units varies depending on whether the security is equity or debt. For equity, units is equal to one. For debt, units is equal to 100.

If the mark difference is negative (i.e., debit to the participant), the value is rounded up to two decimal places.

If the mark difference is positive (i.e., credit to the participant), the value is truncated to two decimal places.

8.7 Monitoring settlements using CDSX

Participants can monitor their settlements on an intraday basis in CDSX by following the procedures for:

• Inquiring on exchange trades on page 22

• Inquiring on non-exchange trades on page 35.

For CNS, participants may also follow the procedures for Inquiring on CNS outstanding positions on page 78.

The next day, participants may review the CNS activities on the appropriate report. For more information on the trade, settlement and CNS-related reports, refer to CDS Reporting Procedures.

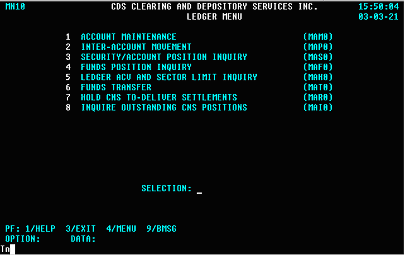

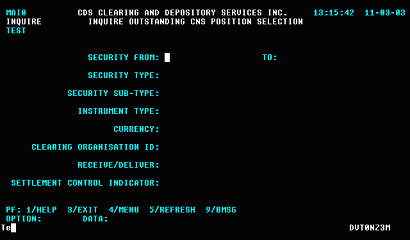

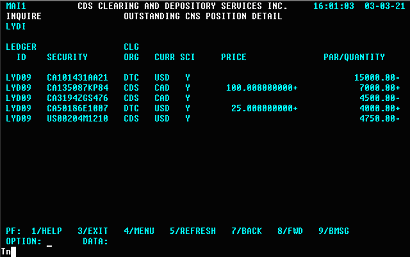

8.7.1 Inquiring on CNS outstanding positions

To inquire on CNS outstanding positions:

1. Log on to CDS systems. For more information, refer to Participating in CDS Services.

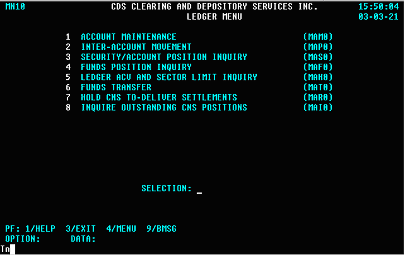

2. On the CDS Clearing and Depository Services Inc. Main Menu, type the number identifying CDSX -- Customer Functions in the SELECTION field and press ENTER. The CDSX -- Customer Functions Menu on page 10 displays.

3. Type the number identifying Ledger Menu in the SELECTION field and press ENTER.

The Ledger Menu on page 79 displays.

Ledger Menu

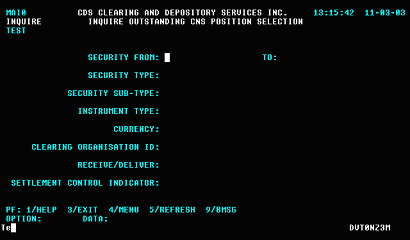

4. Type the number identifying Inquire Outstanding CNS Positions in the SELECTION field and press ENTER. The Inquire Outstanding CNS Positions Selection screen on page 79 displays.

Inquire Outstanding CNS Positions Selection screen

5. Complete the fields as indicated in the table below.

Field

Description

SECURITY FROM, TO

A range of security numbers (a partial or full security number may be entered)

If these fields are completed, the SECURITY TYPE, SECURITY SUB-TYPE and INSTRUMENT TYPE must be left blank

SECURITY TYPE

D -- Debt

E -- Equity

SECURITY SUB-TYPE

AB -- Asset-backed issue

MB -- Market bond

MM -- Money market issue

PK -- Package

SI -- Strip

INSTRUMENT TYPE

Code identifying the instrument type

CURRENCY

CAD -- Canadian dollar

USD -- U.S. dollar

CLEARING ORGANIZATION ID

Code of the clearing organization:

CDS -- Domestic CNS positions

RECEIVE/DELIVER

Code identifying the type of CNS outstanding position:

R -- Outstanding to-receive positions

D -- Outstanding to-deliver positions

SCI

Settlement control indicator for the position:

Y -- Submit the position for settlement

N -- Do not settle the position

6. Press ENTER. The Outstanding CNS Positions Detail screen on page 81 displays.

Outstanding CNS Positions Detail screen

7. Review the details on the screen.

Field

Description

SCI

Settlement control indicator for the position:

Y -- Submit the position for settlement

N -- Do not settle the position

PRICE

Price against which the outstanding position is expected to settle

PAR/QUANTITY

Total outstanding position

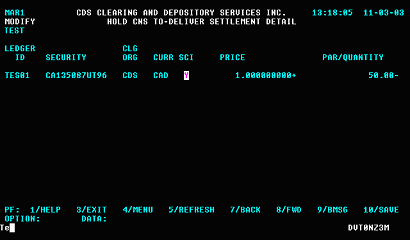

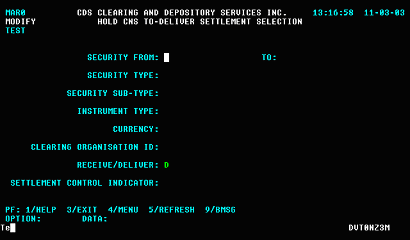

8.7.2 Holding CNS to deliver settlements

To hold CNS to deliver positions:

1. Log on to CDS systems. For more information, refer to Participating in CDS Services.

2. On the CDS Clearing and Depository Services Inc. Main Menu, type the number identifying CDSX -- Customer Functions in the SELECTION field and press ENTER. The CDSX -- Customer Functions Menu displays.

3. Type the number identifying Ledger Menu in the SELECTION field and press ENTER. TheLedger Menu on page 79 displays.

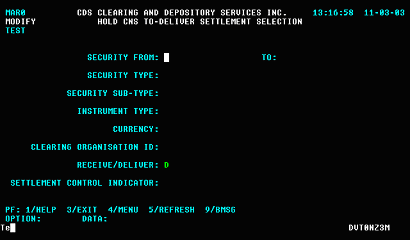

4. Type the number identifying Hold CNS To-Deliver Settlements in the SELECTION field and press ENTER. The Hold CNS To-Deliver Settlement Selection screen displays.

Hold CNS To-Deliver Settlement Selection screen

5. Complete the fields as indicated in the table below.

Field

Description

SECURITY FROM, TO

A range of security numbers (a partial or full security number may be entered)

If these fields are completed, the SECURITY TYPE, SECURITY SUB- TYPE and INSTRUMENT TYPE must be left blank

SECURITY TYPE

D -- Debt

E -- Equity

SECURITY SUB- TYPE

Code identifying the security sub-type:

AB -- Asset-backed issue

MB -- Market bond

MM -- Money market issue

PK -- Package

SI -- Strip

INSTRUMENT TYPE

Code identifying the instrument type

CLEARING ORGANISATION ID

Code identifying the clearing organization:

CDS -- Domestic CNS positions

RECEIVE/DELIVER

Code identifying the type of CNS outstanding position:

R -- Outstanding to-receive positions

D -- Outstanding to-deliver positions

SCI

Settlement control indicator for the position:

Y -- Submit the position for settlement

N -- Do not settle the position

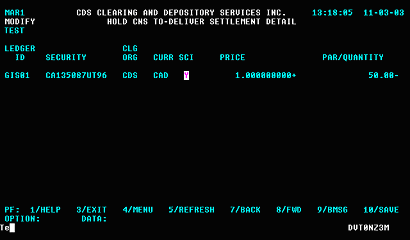

6. Press ENTER. The Hold CNS To-deliver Settlement Detail displays.

Note: Outstanding to receive positions cannot be placed on hold. Holds are automatically removed at the end of the day.

Hold CNS To-Deliver Settlement Detail screen

7. Complete the fields as indicated in the table below.

Field

Description

SCI

Settlement control indicator for the position:

Y -- Submit the position for settlement

N -- Do not settle the position

PRICE

Price against which the outstanding position is expected to settle

PAR/QUANTITY

Total outstanding position

8. Press Enter to validate the information and press PF10 to save.

CHAPTER 9 BUYING IN OUTSTANDING CNS POSITIONS

Life cycle of a buy-in

9.1.1 Buy-in statuses

During the buy-in process, the status of the buy-in may change to reflect its current state. The table below details all the possible statuses of a buy-in.

Status

Name

Description

I

Intent

Intent to buy-in is entered, saved and confirmed

IX

Partially processed intent

Intent not yet accepted by the system

E

Execute

Buy-in is in execute status

EX

Next day execute

Buy-in is scheduled for execution on next business day

C

Cancelled

Buy-in is cancelled

CX

Pending cancellation

Cancellation not yet accepted by the system

XP

Expired

Receiver failed to execute buy-in before the cutoff time

NP

Not processed

Buy-in cannot be processed (unavailability of outstanding CNS positions)

9.1.2 Execution days

The table below indicates the execution days for buy-ins, depending on the entry time and the clearing organization.

Entry day

Entry time

Clearing organization

Execution day

Day 1

Between 4:00 p.m. and 4:45 p.m. ET (2:00 p.m. and 2:45 p.m. MT,

CDS

Day 3 (N+2)

1:00 p.m. and 1:45 p.m. PT)

Day 1

Between 4:45 p.m. and 7:30 p.m. ET (2:45 p.m. and 5:30 p.m. MT,

CDS

Day 4 (N+3)

1:45 p.m. and 4:30 p.m. PT)

Note: The Buy-In Intent Entry screen on page 88 is enabled at 4:00 p.m. ET (2:00 p.m. MT, 1:00 p.m. PT) daily. This process is separate from and unaffected by the payment exchange process.

For example, a buy-in that was entered on day 1 between 4:00 p.m. and 4:45 p.m. ET (2:00 p.m. and 2:45 p.m. MT, 1:00 p.m. and 1:45 p.m. PT) with CDS as the clearing organization, is scheduled to execute on day 3, provided that the receiver changes the status of the buy-in to execute (E). If the status is not changed to E by execution date, the buy-in is automatically cancelled.

Note: CDSX automatically manages Canadian holidays when determining the execution date. For example, if a receiver enters a Canadian dollar buy-in request on Monday and Wednesday is a Canadian holiday with Canadian dollar settlement restrictions, CDSX automatically establishes the execution date as Thursday. For more information, refer to CDSX Procedures and User Guide.

CHAPTER 9 BUYING IN OUTSTANDING CNS POSITIONS

Deliver buy-in positions

9.4 Deliverer buy-in activities

Deliverers can inquire on their buy-in liabilities, request an extension and produce a maximum execute liability (MEL) report.

Note: A deliverer may satisfy its buy-in maximum liability by the actual settlement of the failed-to-deliver CDS position. This liability may be covered during the period from the date on which the buy-in intent was received until 2:30 p.m. ET (12:30 p.m. MT, 11:30 a.m. PT) on the execution date.

A deliverer is not relieved of their buy-in liability during the above period, even if it has moved from a short position to a flat or long position due to netting.

A deliverer may be held liable if settlement of the fail-to-deliver CNS position occurs after 2:30 p.m. ET (12:30 p.m. MT, 11:30 a.m. PT).

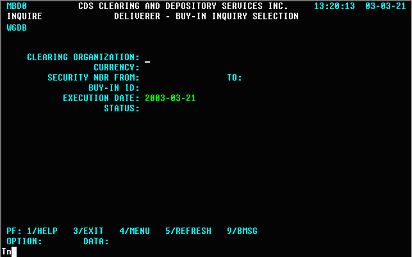

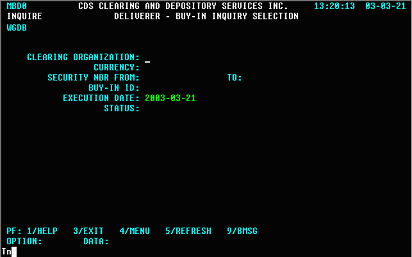

9.4.1 Inquiring on a buy-in

To inquire on the details of liability records:

1. Access the Buy-In Menu on page 87. For more information, see Accessing the Buy-In Menu on page 87.

2. Type the number identifying Deliverer Inquire Buy-In in the SELECTION field and press ENTER. The Deliverer -- Buy-In Inquiry Selection screen on page 100 displays.

Deliverer -- Buy-In Inquiry Selection screen

CHAPTER 10

CCP fails-to-receive interest mark and fee

CDS generates an interest mark to automatically compensate deliverers for losses incurred due to the inability of receivers to receive securities in CNS and FINet. Participants failing to receive are responsible for these interest marks. CDS applies a CCP fails-to-receive fee to discourage receivers from failing to settle in CNS and FINet.

The interest mark and fee are only applicable if the deliverer could not deliver its securities.

10.1 Fails-to-receive interest mark

To distribute the interest costs, CDS uses an fails-to-receive interest mark. This mark is applied in accordance with the following rules:

• The interest mark is applied to the ledgers in the same manner as other marks

• The interest mark does not draw down on caps or lines of credit

• ACV is not impacted by positive and negative marks

• After conversion of any negative USD interest marks to Canadian dollars, the negative interest marks are included in the mark-to-market component of the IRMS collateral requirements. For more information, refer to Participating in CDS Services.

10.1.1 Calculation of the CNS fails-to-receive interest mark

The total fails-to-receive interest mark is calculated based upon the value of shares that a deliverer could not deliver in CNS on the current day multiplied by a benchmark rate, multiplied by the number of days to the next business day. If there is more than one failed receiver for a specific delivery, the portion of the mark that a failed receiver is responsible for is prorated based on their failed quantity.

The calculation is run at 5:30 p.m. ET (3:30 p.m. MT, 2:30 p.m. PT) each business day using settlement information.

Fails-to-receive interest marks are credited to the deliverer's funds account and debited from the receiver's funds account. The currency of the fails-to-receive interest marks depends upon the currency associated with the outstanding CNS position. These funds movements are effective the following business day.

Canadian dollar and U.S. dollar benchmark rates are established as follows:

• Canadian dollars -- Bank of Canada target for overnight rate + 50 basis points

• U.S. dollars -- Federal Funds Rate + 50 basis points

CHAPTER 1 INTRODUCTION TO TRADE AND SETTLEMENT

Settling trades in CDSX

1.4.1 Trade and settlement cutoff times

The start and cutoff times for trade and settlement activities are indicated in the table below.

|

Trade and settlement activities in CDSX |

ET |

MT |

PT |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|||

|

Trade reporting and management{2} |

7:00 a.m. - |

5:00 a.m. - |

4:00 a.m. - |

|

|

|||

|

Settle trades targeted to settle by TFT settlement through real-time settlement processes |

4:00 p.m.{3} |

2:00 p.m. |

1:00 p.m. |

|

|

|||

|

FINet real-time trade settlement |

|

|

|

|

|

|||

|

No settlement of FINet netted trades or FINet eligible trades during FINet intraday netting |

|

|

|

|

|

|||

|

Settle outstanding CNS positions through real- time settlement processes |

|

|

|

|

|

|||

|

No CNS real-time settlement during CNS intraday netting |

|

|

|

|

|

|||

|

During payment exchange, security settlement and the restricted (ACV) TFT |

4:00 p.m. - |

2:00 p.m. - |

1:00 p.m. - |

|

|

|||

|

No FINet real-time trade settlement |

5:00 p.m. |

3:00 p.m. |

2:00 p.m. |

|

|

|||

|

No CNS real-time settlement |

|

|

|

|

|

|||

|

After payment exchange, only securityTFT settlement |

5:00 p.m. - |

3:00 p.m. - |

2:00 p.m. - |

|

|

|||

|

occurs and the ACV edit is no longer applied{1} |

7:30 p.m. |

5:30 p.m. |

4:30 p.m. |

|

|

|||

|

No FINet real-time trade settlement |

|

|

|

|

|

|||

|

No CNS real-time settlement |

|

|

|

|

|

|||

|

System shutdown |

7:30 p.m. |

5:30 p.m. |

4:30 p.m. |

|

|

|||

|

Overnight online activity processing of TFT |

12:30 a.m - |

10:30 p.m. - |

9:30 p.m. - |

|

|

|||

|

transactions{1} |

4:00 a.m. |

2:00 a.m. |

1:00 a.m. |

|

|

|||

|

FINet real-time trade settlement |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|||

|

No CNS real-time settlement |

|

|

|

|

|

|||

|

CNS/BNS process |

Starts at |

Starts at |

Starts at |

|

|

|||

|

|

4:00 a.m. |

2:00 a.m. |

1:00 a.m. |

{1}

These times may vary depending on the progress of the batch schedule.{2} These times may vary depending on the progress of the batch schedule.

{3} Start of payment exchange

CHAPTER 8 SETTLEMENT OF TRADES

Settlement cut-off times

CHAPTER 8

Settlement of trades

Trades are settled in CDSX in one of the modes of settlement indicated in the table below.

For information on the settlement of FINet trades, see FINet real-time settlement on page 50.

Mode of settlement

Description

Trade-for-trade (TFT) settlement

Trades targeted to settle by TFT are settled on an individual basis

Book-based settlement where trades are settled on an individual basis. Partial settlement cannot occur

Continuous net settlement (CNS)

Book-based settlement wheretTrades targeted to settle by CNS that have reached value date are netted daily with outstanding unsettled or partially settled quantities. The positions involved in these trades must be held in the participant's general accountat thestart of the CNS/BNS process or any scheduled intraday CNSprocess, in order to be considered forCNSsettlement

Unsettled quantities (i.e., "fails") are maintained by CDSX as outstanding positions. The seller has the to-deliver position and the buyer has the to-receive position for the quantities that have not settled. CDSX maintains CNS outstanding positions by ledger, security, currency and clearing organization

. Periodically, CDSXattempts to settle these outstanding positions

For example, when a participant sells 100 shares of security A and buys 80 shares of security A, the participant has a net CNS to-deliver position of 20 shares of security A. If the participant didnot complete the net delivery to CDS, the CNS process creates anCNS outstanding to-deliver position, which is carried forward to the next CNS settlement or CNS netting processTrades reported to CDSX with certificate-based settlement (CBS) as the mode of settlement are not considered for settlement.

It is the participant's responsibility to manage their positions in their general account (GA000).

For example, iIf participants do not want shares in a certain security to settle in CNS, they must do one of the following:• rRemove the

securityposition from their general account prior to the start of the CNS/BNS processor any scheduled intraday CNS process• Remove the position from their general account during the day when the real-time CNS settlement process is running

• Place outstanding to deliver positions on hold. -

ACV edit on settlement

CDSX supports both Canadian dollar and U.S. dollar settlement.

The aggregate collateral value (ACV) edit is applied up to the end of the Canadian dollar payment exchange period only. During the payment exchange period, a modified ACV edit is applied. Once payment exchange is complete, the ACV edit is not applied. For more information, refer to Participating in CDS Services.

8.1 Settlement cutoff times

The cutoff times for settlement activities are indicated in the table below. If necessary, CDS sends a broadcast message to all participants to inform them of any changes in cutoff times.

Settlement activities

ET

MT

PT

Real-time TFT settlement{1}

7:00 a.m. -

5:00 a.m. -

4:00 a.m.

7:30 p.m.

5:30 p.m.

- 4:30 p.m.

Intraday netting

1:00 p.m.

11:00 a.m.

10:00 a.m.

Real-time CNS settlement

Intraday CNS7:00 a.m. -

5:00 a.m. -

4:00 p.m.

No CNS real-time settlement during CNS intraday netting

4:00 a.m. -

2:00 p.m.

1:00 p.m.

10:00 a.m.

8:00 a.m.

7:00 a.m.

12:00 p.m.

10:00 a.m.

9:00 a.m.

2:00 p.m.

12:00 p.m.

11:00 a.m.

3:30 p.m.

1:30 p.m.

12:30 p.m.

Restricted TFT settlement period

4:00 p.m. -

2:00 p.m. -

1:00 p.m. -

7:30 p.m.

5:30 p.m.

4:30 p.m.

Real-time TFT settlement{1}

12:30 a.m. -

10:30 p.m. -

9:30 p.m. -

4:00 a.m.

2:00 a.m.

1:00 a.m.

CNS/BNS process

Starts at

Starts at

Starts at

4:00 a.m.

2:00 a.m.

1:00 a.m.

{1} These times may vary depending on the progress of the batch schedule.

8.2 Restricted TFT settlement

At the start of payment exchange, CDSX no longer settles Canadian and U.S. dollar funds. The restriction is placed on Canadian dollar TFT settlements during the Canadian payment exchange period, and U.S. dollar settlements during the U.S. payment exchange period.

If a pending TFT trade affects a ledger that has holiday settlement restrictions, the status of the TFT trade is changed from pending to confirmed on the restriction date.

If a funds holiday settlement restriction exists for a ledger and the pending TFT trade does not involve funds, the status of the TFT trade remains pending until the transaction settles.

CHAPTER 8 SETTLEMENT OF TRADES

Real-time TFT settlement

8.3 Real-time TFT settlement

CDSX provides a real-time settlement facility for trades targeted to settle by TFT. Settlement occurs when the trade meets the settlement criteria. This settlement facility continually evaluates trades based on the changing circumstances of the participants in the trades.

When evaluating trades targeted to settle by TFT, CDSX does one of following:

• Settles the trade

• Leaves the trade in a confirmed status but does not settle it

• Assigns a pending settlement status (see Pending trades on page 75).

The table below indicates the settlement criteria for trades targeted to settle by TFT. All of the settlement criteria must be met for CDSX to process the trades.

Settlement criteria for trades targeted to settle by TFT

The trade will be considered for settlement if . . .

The trade will settle if . . .

The trade is confirmed

[check]

[check]

The trade has reached value date

[check]

[check]

Both participants' settlement control indicators are set to Y

[check]

[check]

Neither party is suspended

[check]

[check]

Neither party has a holiday settlement restriction placed on their ledger

[check]

[check]

For trades targeted to settle by TFT, tThe security is CDSX-eligible[check]

[check]

The seller has sufficient ledger position in the security in the trade

[check]

The buyer has sufficient available funds in the currency of the trade

[check]

Both the buyer and the seller have sufficient ACV

[check]

CHAPTER 8 SETTLEMENT OF TRADES

CNS/BNS process

8.3.1 Pending trades

When CDSX assigns a pending status to a TFT trade, a two-character pending reason code displays in the STATUS field. The first character identifies the party at fault (B for buyer, S for seller) and the second identifies the reason why the transaction is pending (S for insufficient securities, F for insufficient funds or C for insufficient ACV).

Pending transactions are reconsidered for settlement if the participant's circumstances change and settlement conditions are met.

8.4 CNS/BNS process

The CNS/BNS process is a batch net settlement process that increases settlement efficiency by combining the settlement of trades targeted to settle by CNS and TFT.

The CNS component processes the CNS trades and the BNS component processes the TFT trade.The goal of the combined process is to allow CNS and TFT activities to net against each other and to reduce a participant's requirements for security positions, funds, cap, credit and collateral.The CNS/BNS process occurs once per day after the overnight online period and is currently scheduled to execute around 4:00 a.m. ET (2:00 a.m. MT, 1:00 a.m. PT).

8.4.1 CNS

Ttrade extraction and netting forthe CNS/BNS processsettlementCDSX extracts trades that are targeted to settle by CNS based on the following extraction criteria:

• Exchange and non-exchange trades are considered

• The mode of settlement is CNS

• The trade status is C

•

Both participants' settlement indicators are set to Y• The value date is less than or equal to the current business date

• There is no CDS holiday settlement restriction for the currency of the trade

• The security is eligible for CNS

• The participants' ledgers are not suspended.

If the extraction criteria is met, the trade is netted, marked and considered for settlement by CNS.

CDS

is notified and, depending on the circumstances,may "allot" a trade to settle by TFT if the trade is not extracted due to the following:• The security is not eligible to settle by CNS

• Either participant is not eligible for the CNS service

• Either participant's ledger is suspended.

Once extracted, CNS trades are marked and netted with current CNS outstanding positions. Once netted, the new outstanding positions are also marked. Marks are applied directly against the deliverer's and receiver's funds accounts.

Note: Lines of credit and/or caps are not drawn upon for negative marks being applied.

The CNS/BNS process marks trades and CNS outstanding positions based on the latest market prices received from external sources.

Trades targeted to settle by TFT are also extracted for inclusion in the CNS/BNSprocess. The eligibility requirements are consistent with trades targeted to settle byCNS.8.4.2 Settlement during the CNS/BNS process

If the conditions for settlement are met, the CNS/BNS process attempts settlement based on defined settlement priority. The conditions for settlement are the same as those for real-time TFT

settlementand CNS settlement.intraday continuous net settlement (CNS).To review the conditions for settlement, see Settlement criteria for trades targeted to settle by TFT on page 74 and Settlement criteria for real-time continuous net settlement on page 77.

The settlement priority for the CNS/BNS process is as follows:

• Domestic U.S. dollar TFT trades flagged as mandatory cash from TSX

• Domestic Canadian dollar TFT trades flagged as mandatory cash from TSX

• DTCC Canadian dollar TFT settlement

• Domestic Canadian dollar TFT settlement

• Domestic U.S. dollar CNS to-receive positions with buy-ins

• Domestic Canadian dollar CNS to-receive positions with buy-ins

• Domestic U.S. dollar CNS outstanding positions

• Domestic Canadian dollar CNS outstanding positions.

During the CNS/BNS process, CNS positions settle entirely or partially, and trades targeted to settle by TFT settle entirely or are made pending.

CHAPTER 8 SETTLEMENT OF TRADES

IntradayReal-time CNS settlement process8.5

IntradayReal-time CNS settlement processUnlike the CNS/BNS process, which processes trades targeted to settle by TFT and CNS together, the

intradayreal-time CNS settlement process only processes outstanding CNS positionstrades targeted to settle by CNS. This processis scheduled at various periodsruns throughout the business day and executesat the same time butindependently of the real-time TFT settlement process.While the otherintraday CNS processes only involve settlement, the 2:00 p.m. ET (12:00 p.m. MT, 11:00 a.m. PT) intraday CNS process also includes trades that are extracted and netted subsequent to the running of CNS/BNS.Once CDSX determines that the

CNScriteriaconditionsfor CNS settlement have been met (see Settlement criteria for real-time continuous net settlement on page 77), theintradayreal-time CNS settlement facility attempts to settle outstanding CNS positions based on the following settlement priority:• Domestic U.S. dollar CNS to-receive positions with buy-ins

• Domestic Canadian dollar CNS to-receive positions with buy-ins

• Domestic U.S. dollar CNS outstanding positions

• Domestic Canadian dollar CNS outstanding positions.

Since

intradayreal-time CNS settlement executes while other online settlement functions are also processing, the settlement priority noted above cannot be guaranteed.CDSX maintains the buy-in priority, which ensures that participants who have been bought in can only deliver to receivers with a buy-in position. The buy-in priority is maintainedthroughout the day.

for all intraday CNS cycles with the exception of thelast scheduled execution. During the last scheduled execution, the settlement of abought-in position can be delivered to a receiver who does not have a buy-in.8.5.1 Settlement criteria for real-time continuous net settlement

The following criteria must be met for CNS to consider settlement of outstanding positions:

• Both the deliverer and receiver are eligible for the CNS service

• The security is CNS-eligible

• Both participants are not suspended

• Both participants do not have holiday settlement restrictions placed on their ledger.

• The outstanding to deliver position is not on hold.

Settlement or partial settlement occurs if:

• Sellers have all or some ledger positions in the security for which they are in a to-deliver position

• Buyers have sufficient available funds to accept all or some of the delivery for which they are in a to-receive position

• Both the deliverer and receiver have sufficient ACV to deliver or receive all or some of the delivery.

8.5.2 Intraday marking of CNS outstanding positions

CDSX provides a facility to re-mark CNS outstanding positions intraday in the following circumstances:

• Current value trades are extracted intraday

• Intraday market prices change sufficiently to warrant revaluation of outstanding positions.

8.5.3 Intraday extraction, marking and netting of CNS trades

CDSX provides a facility to extract current value trades that are targeted to settle by CNS. Intraday extraction, netting and marking is executed if CNS-eligible trades are settled in a same-day environment. When trade extraction is executed intraday, the intraday marking of outstanding positions also occurs.

Intraday extraction may also be scheduled or executed on an ad hoc basis.

CHAPTER 8 SETTLEMENT OF TRADES

Calculating CNS marks

8.6 Calculating CNS marks

CDSX applies marking calculations to CNS trades and outstanding CNS positions.

Trades

The mark difference on a CNS trade is calculated as follows:

- - - - - - - - - - - - - - - - - - - -

(Marking price -- Trade price)

Quantity x

____________________

Units

- - - - - - - - - - - - - - - - - - - -

The value of units varies depending on whether the trade is equity or debt based. For equity, units is equal to one. For debt, units is equal to 100.

If the mark difference exceeds two decimal places, the value is truncated to two decimal places.

Outstanding CNS positions

The mark difference on an outstanding CNS position is calculated as follows:

- - - - - - - - - - - - - - - - - - - -

(Marking price -- Previous marking price)

Quantity x

____________________

Units

- - - - - - - - - - - - - - - - - - - -

The value of units varies depending on whether the security is equity or debt. For equity, units is equal to one. For debt, units is equal to 100.

If the mark difference is negative (i.e., debit to the participant), the value is rounded up to two decimal places.

If the mark difference is positive (i.e., credit to the participant), the value is truncated to two decimal places.

CHAPTER 8 SETTLEMENT OF TRADES

Monitoring settlements using CDSX

8.7 Monitoring settlements using CDSX

Participants can monitor their settlements on an intraday basis in CDSX by following the procedures for:

• Inquiring on exchange trades on page 22

• Inquiring on non-exchange trades on page 35.

For CNS, participants may also follow the procedures for Inquiring on CNS outstanding positions on page 79.

The next day, participants may review the CNS activities on the appropriate report. For more information on the trade, settlement and CNS-related reports, refer to CDS Reporting Procedures.

8.7.1 Inquiring on CNS outstanding positions

To inquire on CNS outstanding positions:

1. Log on to CDS systems. For more information, refer to Participating in CDS Services.

2. On the CDS Clearing and Depository Services Inc. Main Menu, type the number identifying CDSX -- Customer Functions in the SELECTION field and press ENTER. The CDSX -- Customer Functions Menu on page 10 displays.

3. Type the number identifying Ledger Menu in the SELECTION field and press ENTER. The Ledger Menu on page 80 displays.

Ledger Menu

4. Type the number identifying Inquire Outstanding CNS Positions in the SELECTION field and press ENTER. The Inquire Outstanding CNS Positions Selection screen on page 80 displays.

Inquire Outstanding CNS Positions Selection screen

5. Complete the fields as indicated in the table below.

Field

Description

SECURITY FROM, TO

A range of security numbers (a partial or full security number may be entered)

If these fields are completed, the SECURITY TYPE, SECURITY SUB-TYPE and INSTRUMENT TYPE must be left blank

SECURITY TYPE

D -- Debt

E -- Equity

SECURITY SUB-TYPE

AB -- Asset-backed issue

MB -- Market bond

MM -- Money market issue

PK -- Package

SI -- Strip

INSTRUMENT TYPE

Code identifying the instrument type

CURRENCY

CAD -- Canadian dollar

USD -- U.S. dollar

CLEARING ORGANIZATION ID

Code of the clearing organization:

CDS -- Domestic CNS positions

RECEIVE/DELIVER

Code identifying the type of CNS outstanding position:

R -- Outstanding to-receive positions

D -- Outstanding to-deliver positions

SCI

Settlement control indicator for the position:

Y -- Submit the position for settlement

N -- Do not settle the position

6. Press ENTER. The Outstanding CNS Positions Detail screen on page 81 displays. Outstanding CNS Positions Detail screen

7. Review the details on the screen.

Field

Description

SCI

Settlement control indicator for the position:

Y -- Submit the position for settlement

N -- Do not settle the position

PRICE

Price against which the outstanding position is expected to settle

PAR/QUANTITY

Total outstanding position

8.7.2 Holding CNS to deliver settlements

To hold CNS to deliver positions:

1. Log on to CDS systems. For more information, refer to Participating in CDS Services.

2. On the CDS Clearing and Depository Services Inc. Main Menu, type the number identifying CDSX -- Customer Functions in the SELECTION field and press ENTER. The CDSX -- Customer Functions Menu displays.

3. Type the number identifying Ledger Menu in the SELECTION field and press ENTER.

The Ledger Menu on page 80 displays.

4. Type the number identifying Hold CNS To-Deliver Settlements in the SELECTION field and press ENTER. The Hold CNS To-Deliver Settlement Selection screen displays.

Hold CNS To-Deliver Settlement Selection screen

5. Complete the fields as indicated in the table below.

Field

Description

SECURITY FROM, TO

A range of security numbers (a partial or full security number may be entered)

If these fields are completed, the SECURITY TYPE, SECURITY SUB- TYPE and INSTRUMENT TYPE must be left blank

SECURITY TYPE

D -- Debt

E -- Equity

SECURITY SUB-TYPE

Code identifying the security sub-type:

AB -- Asset-backed issue

MB -- Market bond

MM -- Money market issue

PK -- Package

SI -- Strip

INSTRUMENT TYPE

Code identifying the instrument type

CLEARING ORGANISATION ID

Code identifying the clearing organization:

CDS -- Domestic CNS positions

RECEIVE/DELIVER

Code identifying the type of CNS outstanding position:

R -- Outstanding to-receive positions

D -- Outstanding to-deliver positions

SCI

Settlement control indicator for the position:

Y -- Submit the position for settlement

N -- Do not settle the position

6. Press ENTER. The Hold CNS To-deliver Settlement Detail displays.

Note: Outstanding to receive positions cannot be placed on hold. Holds are automatically removed at the end of the day.

Hold CNS To-Deliver Settlement Detail screen

7. Complete the fields as indicated in the table below.

Field

Description

SCI

Settlement control indicator for the position:

Y -- Submit the position for settlement

N -- Do not settle the position

PRICE

Price against which the outstanding position is expected to settle

PAR/QUANTITY

Total outstanding position

8. Press Enter to validate the information and press PF10 to save.

CHAPTER 9 BUYING IN OUTSTANDING CNS POSITIONS

Life cycle of a buy-in

9.1.1 Buy-in statuses

During the buy-in process, the status of the buy-in may change to reflect its current state. The table below details all the possible statuses of a buy-in.

Status

Name

Description

I

Intent

Intent to buy-in is entered, saved and confirmed

IX

Partially processed intent

Intent not yet accepted by the system

E

Execute

Buy-in is in execute status

EX

Next day execute

Buy-in is scheduled for execution on next business day

C

Cancelled

Buy-in is cancelled

CX

Pending cancellation

Cancellation not yet accepted by the system

XP

Expired

Receiver failed to execute buy-in before the cutoff time

NP

Not processed

Buy-in cannot be processed (unavailability of outstanding CNS positions)

9.1.2 Execution days

The table below indicates the execution days for buy-ins, depending on the entry time and the clearing organization.

Entry day

Entry time

Clearing organization

Execution day

Day 1

Between 4:00 p.m. and 4:45 p.m. ET (2:00 p.m. and 2:45 p.m. MT,

CDS

Day 3 (N+2)

1:00 p.m. and 1:45 p.m. PT)

Day 1

Between 4:45 p.m. and 7:30 p.m. ET (2:45 p.m. and 5:30 p.m. MT,

CDS

Day 4 (N+3)

1:45 p.m. and 4:30 p.m. PT)

Note: The Buy-In Intent Entry screen on page 88 is enabled at 4:00 p.m. ET (2:00 p.m. MT, 1:00 p.m. PT) daily. This process is separate from and unaffected by the

final intraday CNS settlement andpayment exchangeprocesseprocesss.For example, a buy-in that was entered on day 1 between 4:00 p.m. and 4:45 p.m. ET (2:00 p.m. and 2:45 p.m. MT, 1:00 p.m. and 1:45 p.m. PT) with CDS as the clearing organization, is scheduled to execute on day 3, provided that the receiver changes the status of the buy-in to execute (E). If the status is not changed to E by execution date, the buy-in is automatically cancelled.

Note: CDSX automatically manages Canadian holidays when determining the execution date. For example, if a receiver enters a Canadian dollar buy-in request on Monday and Wednesday is a Canadian holiday with Canadian dollar settlement restrictions, CDSX automatically establishes the execution date as Thursday. For more information, refer to CDSX Procedures and User Guide.

CHAPTER 9 BUYING IN OUTSTANDING CNS POSITIONS

Deliverer buy-in activities

9.4 Deliverer buy-in activities

Deliverers can inquire on their buy-in liabilities, request an extension and produce a maximum execute liability (MEL) report.

Note: A deliverer may satisfy its buy-in maximum liability by the actual settlement of the failed-to-deliver CDS position. This liability may be covered during the period from the date on which the buy-in intent was received until 2:

030 p.m. ET (12:030 p.m. MT, 11:030 a.m. PT) on the execution date.The actual settlement occurs in the 2:30 p.m. ET (12:30 p.m. MT, 11:30 a.m. PT) CNS intraday cycle.A deliverer is not relieved of

itstheir buy-in liability during the above period, even if it has moved from a short position to a flat or long position due tosettling of tradesduring that timenetting.A deliverer may be held liable if settlement of the fail-to-deliver CNS position occurs after 2:30 p.m. ET (12:30 p.m. MT, 11:30 a.m. PT)

9.4.1 Inquiring on a buy-in

To inquire on the details of liability records:

1. Access the Buy-In Menu on page 87. For more information, see Accessing the Buy-In Menu on page 87.

2. Type the number identifying Deliverer Inquire Buy-In in the SELECTION field and press ENTER. The Deliverer -- Buy-In Inquiry Selection screen on page 100 displays.

Deliverer -- Buy-In Inquiry Selection screen

CHAPTER 10

CCP fails-to-receive interest mark and fee

CDS generates an interest mark to automatically compensate deliverers for losses incurred due to the inability of receivers to receive securities in CNS and FINet. Participants failing to receive are responsible for these interest marks. CDS applies a CCP fails-to-receive fee to discourage receivers from failing to settle in CNS and FINet.

The interest mark and fee are only applicable if the deliverer could not deliver its securities.

10.1 Fails-to-receive interest mark

To distribute the interest costs, CDS uses an fails-to-receive interest mark. This mark is applied in accordance with the following rules:

• The interest mark is applied to the ledgers in the same manner as other marks

• The interest mark does not draw down on caps or lines of credit

• ACV is not impacted by positive and negative marks

• After conversion of any negative USD interest marks to Canadian dollars, the negative interest marks are included in the mark-to-market component of the IRMS collateral requirements. For more information, refer to Participating in CDS Services.

10.1.1 Calculation of the CNS fails-to-receive interest mark

The total fails-to-receive interest mark is calculated based upon the value of shares that a deliverer could not deliver in CNS on the current day multiplied by a benchmark rate, multiplied by the number of days to the next business day. If there is more than one failed receiver for a specific delivery, the portion of the mark that a failed receiver is responsible for is prorated based on their failed quantity.

If shares being deliveredthrough TFT settlement are received after the CNS delivery was attempted in the lastCNS cycle, the fails-to-receive interest mark is not applied.The calculation is run at 5:30 p.m. ET (3:30 p.m. MT, 2:30 p.m. PT) each business day using settlement information.

contained in the last CNS cycle of the day.Fails-to-receive interest marks are credited to the deliverer's funds account and debited from the receiver's funds account. The currency of the fails-to-receive interest marks depends upon the currency associated with the outstanding CNS position. These funds movements are effective the following business day.

Canadian dollar and U.S. dollar benchmark rates are established as follows:

• Canadian dollars -- Bank of Canada target for overnight rate + 50 basis points

• U.S. dollars -- Federal Funds Rate + 50 basis points

The benchmark rate is adjusted in CDSX on the day the rate change is announced.

CHAPTER 10 CCP FAILS TO RECEIVE INTEREST MARK AND FEE

Fails to receive interest mark

10.1.2 Calculation of the FINet fails-to-receive interest mark

The FINet fails-to-receive interest mark is calculated based upon the par value that a deliverer could not deliver on a given day multiplied by a benchmark rate, multiplied by the number of days to the next business day. If there is more than one failed receiver for a specific delivery, the portion of the mark that a failed receiver is responsible for is prorated based on their failed quantity.

The calculation is run at 4:00 p.m. ET (2:00 p.m. MT, 1:00 p.m. PT) each business day. FINet trades are not allowed to settle once CAD payment exchange begins.

Fails-to-receive interest marks are credited to the deliverer's funds account and debited from the receiver's funds account. These funds movements are effective on the following business day.

The Canadian dollar benchmark rate is established as follows:

• Canadian dollars -- Bank of Canada target for overnight rate + 50 basis points

The benchmark rate is adjusted in CDSX on the day when the rate change is announced.

10.1.3 Fails-to-receive fee

In addition to the CNS and FINet fails-to-receive marks, a fails-to-receive fee is charged to receivers who fail to settle in the CNS and/or FINet services. A maximum of one CCP fails-to-receive fee is charged per day, per receiver, per CCP service.

For more information, refer to Fees on CDS's website (www.cds.ca).

10.1.4 Monitoring interest marks

Participants can monitor interest marks through the following:

• The Daily Transaction report. For information, refer to CDS Reporting Procedures.

• The Fails-to-receive Mark Detail Report. For information, refer to CDS Reporting Procedures.

• The Settled Transactions report. For information, refer to CDS Reporting Procedures.

• The Ledger update -- mark-to-market transaction file. For more information, refer to CDS Batch and Interactive Services -- Technical Information.

• The Ledger position update notification to participants file. For more information, refer to CDS Batch and Interactive Services -- Technical Information.