Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

OSC Staff Notice: 81-718 - Summary Report for Investment Fund Issuers 2012

OSC Staff Notice: 81-718 - Summary Report for Investment Fund Issuers 2012

OSC Staff Notice 81-718

Summary Report for

Investment Fund Issuers 2012

Introduction

This third annual Summary Report for Investment Fund Issuers provides an overview of the key activities and initiatives of the Ontario Securities Commission for 2012 that impact investment fund issuers and the fund industry, including:

• key policy initiatives,

• emerging issues and trends,

• disclosure and compliance reviews, and

• recent developments in staff practices.

This report provides information about the status of some of the initiatives the OSC is undertaking to promote clear and concise disclosure in order to assist investors to make more informed investment decisions. The report also provides information about our work to address the sufficiency of regulatory coverage across all investment fund products. It highlights recent product and market developments, as well as our regulatory response to these developments, in order to assist the investment fund industry in understanding and complying with current regulatory requirements.

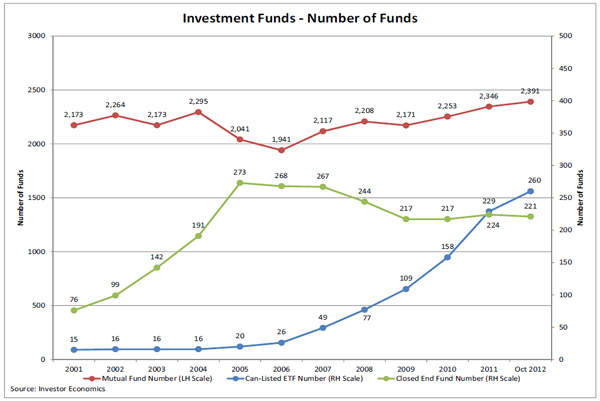

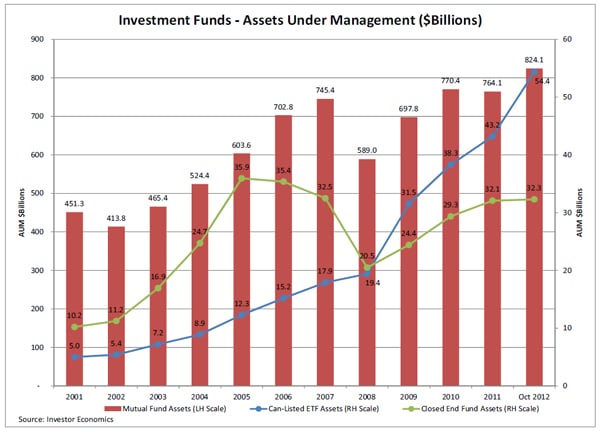

The OSC is responsible for overseeing over 3000 publicly-offered investment funds. Ontario based publicly-offered investment funds hold approximately 80% of the near $900 billion in publicly-offered investment fund assets in Canada.

We administer the regulatory framework for investment funds, including:

• reviewing and assessing product disclosure for all types of investment funds, including prospectuses and continuous disclosure filings,

• considering applications for discretionary relief from securities legislation and rules, and

• taking a leadership role in developing new rules and policies to adapt to the changing environment in the investment fund industry.

We also monitor and participate in investment fund regulatory developments globally, primarily through our work with the International Organization of Securities Commissions (IOSCO). OSC staff participation on the IOSCO C5 Investment Management committee informs our operational and policy work. We discuss our participation with IOSCO further on our website at About Us - International Engagement. In this report, we highlight some of the recent work by IOSCO C5 we think will be of interest to investment fund issuers.

The investment fund products we oversee include both conventional mutual funds and non-conventional investment funds. Non-conventional funds include non-redeemable investment funds such as closed-end funds, mutual funds listed and posted for trading on a stock exchange (ETFs), commodity pools, scholarship plans, labour-sponsored or venture capital funds and flow-through limited partnerships. We discuss the different types of funds further on our website at Investment Funds - Fund Operations.

The ETF market continues to grow steadily, outpacing the growth of conventional mutual funds and closed-end funds. As at October 2012, there were 260 ETFs with assets of approximately $54.4 billion. In comparison, as at the end of 2011, there were 229 ETFs with assets of approximately $43.2 billion, representing an increase in assets of approximately 26%. In contrast, conventional fund assets increased by approximately 8%, and closed-end funds assets remained flat, over the same period.

As these and other investment products, such as linked note derivative offerings, increase in number, the OSC will continue to assess and respond to product developments and innovations with a view to promoting investor protection and assessing the sufficiency and consistency of regulatory treatment of different investment fund products.

1. Key Policy Initiatives

The OSC continues to play a leading role in several significant policy initiatives with other securities regulators in Canada through the Canadian Securities Administrators (the CSA). This section reports on the status of significant policy initiatives including:

• the CSA's project to modernize investment fund product regulation

• point of sale

• scholarship plans

• mutual fund fees

1.1 Modernization of Investment Fund Product Regulation

The mandate for this initiative is to review the regulation of publicly offered investment funds with a view to developing rules that recognize product developments and trends in the investment fund industry. The initiative is being carried out in two phases.

The CSA concluded phase 1 of this project in February 2012 by publishing amendments to National Instrument 81-102 Mutual Funds (NI 81-102) and National Instrument 81-106 Investment Fund Continuous Disclosure (NI 81-106). The amendments updated certain regulatory requirements for mutual funds in order to keep pace with market and product developments, particularly with respect to ETFs. The amendments also introduced new liquidity and term restrictions on money market fund holdings. The amendments came into force on April 30, 2012, other than amendments relating to money market funds which had a 6 month transition period and came into force on October 31, 2012.

Phase 2 of this initiative, now underway, focuses on developing core investment restrictions and operational requirements for publicly offered non-redeemable investment funds, as outlined in CSA Staff Notice 81-322. Concurrently with this work, which will consist of amendments to NI 81-102, the CSA are also considering amendments to National Instrument 81-104 Commodity Pools (NI 81-104) to create a more comprehensive alternative investment fund framework that will operate in conjunction with the proposed amendments to NI 81-102. We are considering having NI 81-104 apply to both mutual funds and non-redeemable investment funds that invest in assets or use investment strategies that would not be permitted under the proposed amendments to NI 81-102. The CSA's goal is to achieve a more consistent, fair and functional regulatory regime across the investment fund product spectrum. We are also considering ways to help investors better differentiate between investment funds that use alternative investment strategies from those that do not. This may include a naming convention, new prospectus and continuous disclosure requirements and new marketing requirements.

We anticipate that the CSA will be able to finalize some aspects of the proposals for non-redeemable investment funds in advance of others. These include the proposed conflicts of interest provisions, securityholder and regulatory approval requirements, and custodianship requirements. Other aspects, particularly certain proposed investment restrictions that are interrelated with the proposals for NI 81-104, will likely require more time to consider and evaluate. We expect these components will be considered in conjunction with each other and to come into effect at the same time.

As part of this work, we will also be seeking input on proposals to enhance the disclosure requirements for all investment funds related to securities lending, repurchase and reverse repurchase transactions to keep pace with global regulatory developments.

The CSA plans to publish its Phase 2 proposals for comment early in 2013.

1.2 Point of Sale

The Point of Sale (POS) Project is a continuation of the CSA's participation in the project by the Joint Forum of Financial Market Regulators to develop a more effective disclosure regime for conventional mutual funds and segregated funds.

The Fund Facts is central to the POS project and is designed to make it easier for investors to find and use key information. The Fund Facts is in plain language, no more than two pages double-sided and highlights key information that is important to investors, including past performance, risks and the costs of investing in a mutual fund.

On June 18, 2010, the CSA announced its approach to proceed with a staged implementation of the POS Project in CSA Staff Notice 81-319.

Stage 1, which came into force January 1, 2011, requires mutual funds to produce and file the Fund Facts and for it to be available on the mutual fund's or mutual fund manager's website. The Fund Facts must also be delivered or sent to investors free of charge on request.

On August 12, 2011, the CSA published proposed amendments to NI 81-101 Mutual Fund Prospectus Disclosure that set out Stage 2 of the POS Project (2011 Proposal). Stage 2 proposes to allow delivery of the Fund Facts to satisfy the current prospectus delivery requirements to deliver a prospectus within two days of buying a mutual fund. Although delivery of the simplified prospectus will no longer be required, the simplified prospectus must still continue to be made available to investors upon request.

In response to stakeholder feedback, particularly from investor advocates, to the 2011 Proposal, on June 21, 2012, the CSA published for second comment changes to the Fund Facts. These changes focused primarily on the presentation of risk in the Fund Facts document. The comment period expired on September 6, 2012. We received 33 comment letters from stakeholders.

In the June, 2012 publication, we committed that before finalizing any changes to the Fund Facts content, the CSA would test the proposed changes with investors. The results of this testing would inform what changes the CSA would make to the Fund Facts before finalizing Stage 2. This testing was completed in October 2012. The CSA expects to publish final materials for Stage 2 proposals by Summer 2013.

Concurrent with this work, the CSA is working on a CSA risk rating methodology in response to feedback received that we should mandate a risk methodology for use in the Fund Facts. The CSA expects to consult on this methodology and to publish it for comment on a separate timeframe from the Stage 2 proposals.

In stage 3, the CSA will complete its review and consideration of the issues related to point of sale delivery for mutual funds, as well as publish for further comment any proposed rules that would implement point of sale delivery for mutual funds. As part of this work, we will also consider the applicability of a Fund Facts-type document and point of sale delivery for other types of publicly offered investment funds.

1.3 Scholarship Plans

We have been continuing to work with the CSA to update and improve the disclosure rules that govern scholarship plans, which are a type of investment fund product used by Canadians to save for their children's education.

Amendments to National Instrument 41-101 General Prospectus Requirements (NI 41-101) and proposed new Form 41-101F3 Information Required in a Scholarship Plan Prospectus were first published for comment on March 24, 2010, and then for a second comment period on November 25, 2011. After reviewing the comments received and further considering the proposals, several changes have been made and the CSA published the new prospectus form in final form on January 10, 2013.

The proposals aim to improve the prospectus disclosure provided by scholarship plans by introducing a prospectus form tailored to reflect the unique features of this product. This is an important investor-focused initiative. We know that many investors have trouble understanding the features and complexity of scholarship plans. The new Form 41-101F3 will require scholarship plans to provide investors with key information in a simple, accessible and comparable format to assist them in making a more informed investment decision.

Central to the new prospectus form is the Plan Summary document. Similar to the Fund Facts for mutual funds, it is written in plain language, will be no more than four pages, and highlights the potential risks and the costs of investing in a scholarship plan. It will form part of the prospectus, but will be bound separately.

The CSA expect that adoption of the new prospectus form will lead to more understandable and effective disclosure for investors, enabling them to better understand the possible outcomes and risks associated with investing in scholarship plans.

Following final publication in January 2013, we anticipate the new prospectus form to come into force in Spring 2013.

1.4 Mutual Fund Fees

On December 13, 2012, the CSA published for comment Consultation Paper 81-407 Mutual Fund Fees which examines the mutual fund fee structure in Canada and identifies potential investor protection and fairness issues arising from that structure. The Consultation Paper further sets out various topics for discussion in order to determine whether any regulatory responses are needed to address the issues identified.

The Consultation Paper is the first step in the CSA's public consultations on this topic. Some of the options discussed would impact mutual funds or mutual fund manufacturers directly, and others would impact those who sell the product.

While the focus of this paper is on mutual funds, the CSA recognize that there are other investment fund products whose fee structure may raise similar investor protection and fairness issues for investors. Accordingly, we anticipate that any regulatory initiative we might ultimately undertake would assess whether the same initiative should also apply to other investment funds and comparable securities products.

Before considering any of these options further, the CSA intend to consult extensively with investors and industry participants, and will continue to closely monitor and assess the effects of existing regulatory reforms in Canada, such as the POS initiative, and around the world.

The comments on the Consultation Paper will help inform a roundtable the CSA plans to hold with investors and industry participants in 2013. The comments and discussions will also help the CSA determine what, if any, regulatory responses might be appropriate.

The comment period on the Consultation Paper closes on April 12, 2013.

2. Emerging Issues and Trends

2.1 Pre-Paid Forward Structures in Prospectus Offerings

We continue to consider the use of forward purchase agreements (prepaid forwards) by both mutual funds and non-redeemable investment funds (closed-end funds). We discussed this topic in the December 2011 edition of the Investment Funds Practitioner. In the prepaid forward structure, the fund proposes to pay an amount at the outset of the agreement, which could be substantially all of the fund's assets, to a counterparty. The counterparty is obligated to deliver the performance of a reference fund to the fund at a later date.

Staff have expressed concern about the use of prepaid forwards by investment funds because of the fund's exposure to the counterparty and the credit risk of the counterparty. We also view a prepaid forward, which transfers substantially all of the fund's assets to a counterparty, to change the nature of the fund from a portfolio of diversified holdings to a concentrated investment in one asset that is essentially an unsecured obligation of the counterparty.

To date, OSC staff have generally not recommended discretionary relief for mutual funds to use prepaid forwards. For closed-end funds, which do not require relief to use prepaid forwards, we have, through our prospectus reviews, allowed prepaid forwards only if the risks identified above are mitigated. This has included requiring the counterparty to post collateral for the benefit of the fund (subject to the terms described in the December 2011 Investment Funds Practitioner), and requiring the fund's prospectus to describe the terms of the prepaid forward and include a textbox on the cover page disclosing the fund's counterparty exposure and related risks.

As part of our re-examination of the use by investment funds of prepaid forwards, we have been meeting with counterparties to these agreements to discuss the parameters which could mitigate the concerns we have identified. The requirements under consideration include providing prospectus disclosure of what happens if there is a default or bankruptcy of the counterparty, daily posting of the collateral on the fund manager's website, and prescribing custodianship requirements for the collateral.

We will continue to consider this issue with a view to providing further guidance on the use of prepaid forwards by both mutual funds and closed-end funds in the Investment Funds Practitioner or an OSC staff notice.

2.2 Fund Names

We have noted fund names in preliminary prospectus filings that are not consistent with the fund's investment objectives or investment strategies. We discussed this topic in the April 2012 edition of the Investment Funds Practitioner.

In naming new funds, staff expects that fund managers will consider selecting names which closely reflect the fund's investment objectives, and which distinguish the fund from other funds.

2.3 Foreign Index Participation Units

We noted a continued trend in discretionary relief applications by mutual funds for exemptions from the fund on fund provisions in NI 81-102 to permit top funds to invest in foreign ETFs that, but for the fact that they are not listed on a stock exchange in Canada or the United States, would meet the definition of an index participation unit (IPU) in NI 81-102. For the purposes of this discussion, we refer to these foreign ETFs as Foreign IPUs. The Foreign IPUs for which discretionary relief has been sought to date have included ETFs listed on stock exchanges in the U.K., Germany, Ireland, and China.

The concept of an IPU in NI 81-102 was initially created at a time when there was a limited number of ETFs that tracked broad based diversified indices in Canada and the United States. Since this initial concept, we have observed over the past few years a proliferation in the number of product offerings from index providers, particularly ETFs, that track an index that may not qualify as a "market index" as that term is used in the definition of an IPU in NI 81-102. Staff believes that a market index should be one that is constituted in a manner that is consistent with the investment restrictions set out in NI 81-102. We discussed ETFs and IPUs in last year's branch report. We also discussed market indices and IPUs in the May 2011 edition of the Investment Funds Practitioner.

In considering whether to recommend discretionary relief to allow investments in Foreign IPUs, we have been asking for submissions detailing:

• whether the Foreign IPUs hold the securities that are included in a "widely quoted market index";

• the use, if any, of complex swap-based synthetic index replication strategies in the Foreign IPUs;

• whether the regulatory framework under which the Foreign IPUs operate is substantially similar to the regulatory framework of Canada; and

• the reasons as to why the top fund needs access to the Foreign IPU, and why it cannot meet its investment objectives in a manner that complies with the fund on fund provisions set out in NI 81-102.

To date, staff has been reluctant to recommend discretionary relief in instances where the Foreign IPUs use a synthetic index replication strategy because of its complexity and opacity. Staff has otherwise been prepared to consider recommending discretionary relief to allow investments in Foreign IPUs up to a specified limit in instances where it is demonstrated that the investment in Foreign IPUs is consistent with, and fundamental to, the investment objectives of the fund, and that the regulatory regime of the Foreign IPUs is substantially similar to the regulatory regime in Canada.

2.4 Exposure to Commodities

We reviewed an increasing number of discretionary relief applications from investment funds with objectives aimed at providing investors with exposure to physical commodities, particularly precious metals. These funds directly hold the underlying commodity, or invest indirectly in the underlying commodity by investing in futures contracts or by investing in an ETF that tracks the price of that underlying commodity or directly holds the underlying commodity.

This trend appears to be driven by a growing acceptance of commodities as a separate asset class that may provide the benefit of diversification for a "traditional" portfolio consisting of stocks, bonds and cash, as well as by the desire of product manufacturers to capitalize on the growing retail demand for commodity-linked investments.

To date, staff have generally been prepared to recommend discretionary relief for mutual funds, other than precious metal mutual funds, to permit investments of up to 10% of the net asset value of the fund in gold and/or silver, to achieve this asset diversification. Staff have also recommended relief to permit funds with objectives to provide exposure to a particular sector or industry to invest up to 10% of their net asset value in physical commodities related to the sector or industry.

However, staff have generally taken the view that investments in physical commodities by conventional mutual funds, other than precious metal funds, in excess of 10% of net asset value are not consistent with the nature of a mutual fund as a diversified portfolio of securities.

2.5 Increase in Linked Note Offerings

There was an increase in the number of linked note pricing supplements filed during the course of 2012. CSA Staff Notice 44-304 Linked Notes Distributed Under the Shelf Prospectus System sets out staff's concerns about disclosure provided in the shelf prospectus relating to the linked notes, as well as the process for requesting the pre-clearance of linked notes under the shelf prospectus system.

We continue to review the supplements filed for pre-clearance that are offering "novel" derivatives. As part of our reviews:

• staff have expressed concerns about some novel underlying interests that consist of actively managed portfolios. In those instances, we have raised comments regarding the transparency of the underlying interest, and whether the linked note or the underlying interest should be subject to some additional requirements similar to those that apply to investment funds.

• staff have expressed concern with structures where discretion could be exercised by the issuer of the linked notes in any material calculations affecting the linked notes. In such instances, staff have asked that an independent calculation agent be used.

• we reviewed some supplements that had not been filed for pre-clearance, and raised comments in instances where the supplement included disclosure such as past performance data that was potentially misleading.

• we asked filers to provide, among other things, continuous disclosure regarding the linked notes on a website and to refer investors to the site in the supplement; and disclosure of all fees payable by holders of the notes, including fees paid to dealers.

We will continue reviewing these supplements with a view to informing what regulatory changes or guidance may be appropriate in connection with novel offerings filed under National Instrument 44-102 Shelf Distributions.

3. Disclosure and Compliance Reviews

On an ongoing basis, OSC staff review the prospectus and continuous disclosure filings of Ontario-based investment funds. Risk-based criteria are used to select investment funds for reviews of their disclosure documents. We may also choose to conduct targeted reviews of a particular industry segment or on a particular topic. In addition to our prospectus and continuous disclosure reviews, the Investment Funds (IF) Branch works closely with staff in the Compliance and Registrant Regulation (CRR) Branch on issues related to fund manager compliance and identifying possible emerging issues. This can sometimes lead to us conducting joint reviews.

3.1 Continuous Disclosure Reviews

This section discusses some of our reviews and findings in connection with:

• advertising and marketing materials

• yield/income funds

• risk ratings in Fund Facts

• review of portfolio holdings

3.1.1 Advertising and Marketing materials

We commenced a targeted review of advertising and marketing materials of investment funds. A key objective of this review is to raise awareness for preparers of advertising and marketing materials that staff are monitoring advertising activities and looking beyond technical compliance with the OSC's marketing rules to determine if overall the information presented is potentially misleading to retail investors.

As part of this initiative, in addition to continuing ad hoc reviews of advertising materials based on staff's monitoring, dedicated IF Branch staff have been selecting advertising and marketing materials of 4 to 6 investment fund managers to review on a quarterly basis. These reviews cover conventional mutual funds, closed-end funds, exchange-traded funds, commodity pools, and labor sponsored investment funds.

As part of the review, staff have been asking the selected investment fund manager for all advertisements and marketing materials appearing in newspapers, presentations, brochures, the internet, television and radio ads, social media, fund manager websites, email blasts, and green sheets during the previous quarter. Staff also ask for a description of the policies and procedures relating to the investment fund manager's marketing activities.

A few common or recurring issues that we have noted during our reviews to date include:

• inappropriate use of hypothetical data

• use of unsupportable statements

• failure to provide a balanced message on risk/reward

• internet ads without the required appropriate warning language

• lack of adherence to the requirement to provide standard performance

• use of misleading headlines, or headlines that suggest a degree of safety, a lack of risk, or phenomenal skills or results.

Our reviews have resulted in investment fund managers :

• removing certain advertisements that we brought to their attention

• materially changing their sales communications

• reviewing and revising their policies and procedures

• re-training their staff involved in producing and approving their marketing materials.

We expect to publish our observations and guidance arising from this review in Spring 2013.

3.1.2 Yield/Income Funds

We reviewed the prospectuses of a sample of investment funds that make regular distributions to investors. The scope of this review included the distribution policies and the investment fund manager's decision making process on the form and amount of the distributions.

We identified a number of issues, including:

• Funds paying distributions in excess of the fund's increase in net asset value from operations. In these instances, while such distributions are essentially a return to the investor of their own capital, the use of terminology such as "yield" or "income" in the fund's name implies underlying performance or earnings;

• Funds paying distributions in the form of reinvested units unless, for funds held in non-registered plans, the investor expressly chooses to receive cash distributions. In staff's view, receiving reinvested units may conflict with the funds' stated focus of providing investors with a regular income stream.

You can find further details regarding this review in the April 2012 Investment Funds Practitioner. In addition to identifying staff's concerns, the Practitioner communicated OSC staff's expectations regarding disclosure that should be provided in prospectuses and continuous disclosure documents to highlight the nature of the distributions, indicate why distributions were made despite the shortfall in earnings, and what investor action is needed if cash distributions are desired.

We will continue to monitor these offerings through our prospectus reviews with a view to informing what regulatory changes or guidance may be appropriate.

3.1.3 Risk Ratings In Fund Facts

We continued to carry out a focused review of the risk ratings assigned to mutual funds in the Fund Facts document with a view to identifying outliers, and asking the mutual fund managers to provide submissions to support the determination of the risk rating of the mutual fund. We introduced the scope of this focused review in last year's summary report.

We identified mutual funds with risk ratings of "low to medium" or "medium" compared with peer funds with risk ratings of "medium to high" and "high". Where we challenged the risk rating of the mutual fund relative to the risk classification methodology used by the manager, as identified in the simplified prospectus, we relied upon objective data and benchmarks to support our analysis.

As a result of the review, some mutual fund managers changed the fund risk rating, increasing the rating from "medium" to "medium to high". In these instances, staff asked that an amended and restated Fund Facts be filed to reflect the change. OSC staff generally take the view that an increase to a mutual fund's risk rating is a material change under securities legislation.

3.1.4 Review of Portfolio Holdings

The scope of this review was introduced in last year's summary report. During the year, the IF Branch completed its targeted review of portfolio holdings by investment funds. We reported our findings in OSC Staff Notice 81-717 Report on Staff's Continuous Disclosure Review of Portfolio Holdings by Investment Funds, which was published in August, 2012.

3.2 Compliance and Registrant Regulation Branch and Investment Fund Manager Compliance Reviews

In November 2012, staff of the CRR Branch published OSC Staff Notice 33-738 OSC Annual Summary Report for Dealers, Advisers and Investment Fund Managers. The primary purpose of the Staff Notice is to assist registrants, including investment fund managers (IFMs), in complying with their regulatory obligations under Ontario securities law. The Staff Notice summarizes new and proposed rules and initiatives impacting registrants, current trends in deficiencies from compliance reviews of registrants (and suggested practices to address them), and current trends in registration issues.

Section 5.5 of the Staff Notice contains information specifically for IFMs, from the reviews carried out by the CRR Branch. Topics included:

• insufficient oversight of outsourced functions and service providers

• valuation of restricted securities

• inappropriate expenses charged to funds

• inadequate insurance coverage

• marketing practices

Also during the year, the CRR Branch published Multilateral Instrument 32-102 Registration Exemptions for Non-Resident Investment Fund Managers (MI 32-102) containing the registration requirements that apply in Ontario, Quebec, and Newfoundland and Labrador to non-resident IFMs, which include international and domestic IFMs who do not have a place of business in the province.

Under MI 32-102, the registration of all non-resident IFMs that have a significant connecting factor to Ontario is required unless they can rely on one of the available exemptions. Existing non-resident IFMs that are acting as an IFM in Ontario must have applied for registration by December 31, 2012.

For more information, see MI 32-102.

4. Outreach, Consultation and Education

We continue our efforts to be transparent regarding practices and procedures that impact investment fund issuers in as timely a manner as possible. Our intent in doing so is to better enable fund managers and their advisors to avoid potential regulatory issues when they are at the planning stage for a new fund or transaction.

4.1 Investment Funds Product Advisory Committee (IFPAC)

The OSC's IFPAC was established in August, 2011. The IFPAC, which is currently comprised of 13 members, advises OSC staff specifically on emerging product developments and innovations occurring in the investment fund industry, and discusses the impact of these developments and emerging issues. The IFPAC also acts as one source of feedback to OSC staff on the development of policy and rule-making initiatives to promote investor protection, fairness and market efficiency across all types of publicly offered investment fund products. The IFPAC meets quarterly and is chaired by Rhonda Goldberg, Director of the Investment Funds Branch. The IFPAC members serve a two year term. The initial two year term expires in 2013, and we expect to solicit applications for membership in Spring 2013. You can find a list of current IFPAC members on the OSC website.

Topics of discussion with the IFPAC have included the increasing use and complexity of derivatives; trends in structured products; and emerging asset classes (such as commodities) and foreign products/indices.

In addition to the IFPAC, OSC staff continue to meet frequently with stakeholders, including investment fund managers and their advisors, investor advocates and subject matter experts on various topics to inform our policy and operational work. In May, 2012, Som Seif, founder of Claymore Investments Inc., worked with OSC staff in a consultant capacity, to discuss investment fund product trends, and capital market developments generally.

OSC Staff also continue to hold regular meetings with staff of the U.S. Securities and Exchange Commission. These meetings help to ensure that our regulatory approaches to product development are consistent and that opportunities for regulatory arbitrage between our markets are minimized.

4.2 The Investment Funds Practitioner

The Investment Funds Practitioner is an overview of recent and topical issues arising from applications for discretionary relief, prospectuses and continuous disclosure documents that investment fund issuers file with the OSC and that are reviewed by the IF Branch. It is intended to assist investment fund managers and their advisors who regularly prepare public disclosure documents and applications for discretionary relief on behalf of investment funds.

The Practitioner is also intended to make fund managers more broadly aware of some of the issues we have raised in connection with our reviews and how we have resolved them. The Practitioner can be found on our website at Information for Investment Funds.

We have published 3 editions of the Investment Funds Practitioner since last year's summary report: December 2011, April 2012 and November 2012. We welcome suggestions for future topics.

4.3 IFRS Transition Update

In March 2012, we published CSA Staff Notice 81-320 (Revised) Update on International Financial Reporting Standards (IFRS) for Investment Funds to update the investment fund industry on the deferral of the IFRS mandatory changeover date for investment funds in Canada to January 2014. The deferral was to continue to allow the International Accounting Standards Board (IASB) additional time to consider proposals for an "investment entity" to be exempt from the general IFRS requirement to consolidate entities that the investment entity may control. The Staff Notice reminded investment funds that want to use IFRS for financial statements for periods beginning before January 1, 2014 that they must apply for discretionary relief from the current requirement to prepare financial statements in accordance with Canadian generally accepted accounting principles, and that their discretionary relief application must identify any issues that early adoption may create with respect to their financial disclosure.

In October 2012, the IASB published Investment Entities, which introduced the exception, for investment entities, to the general IFRS principle that all subsidiaries must be consolidated.

The direction and clarity provided by this publication will now allow CSA staff to finalize the proposed amendments to NI 81-106 that were originally published in October 2009, in anticipation of the adoption of IFRS by investment funds in Canada. We expect to publish the proposed amendments to NI 81-106 in final form in the Fall of 2013, ahead of the mandatory changeover date of January 1, 2014.

4.4 IOSCO C5 Investment Management

In 2010, the G20 requested that the Financial Stability Board (FSB), in collaboration with other international standard setting bodies, develop recommendations to strengthen the oversight and regulation of the shadow banking system, which includes money market funds (MMFs). In Fall 2011, the FSB asked IOSCO to undertake a review of potential regulatory reforms of MMFs that would mitigate their susceptibility to runs and other systemic risks, and to develop policy recommendations. OSC staff participated on the IOSCO C5 working group formed to respond to the FSB's request.

In April 2012, IOSCO published a consultation paper providing an analysis of the systemic risks posed by MMFs and outlining potential reform options for their regulation. IOSCO finalized its recommendations to the FSB and published them in October 2012. In November, the FSB endorsed the recommendations as an effective framework for strengthening the resilience of MMFs to risks.

The IOSCO recommendations are intended to provide a common framework for the global regulation of MMFs, while recognizing that the size, features and systemic relevance of MMFs differ across jurisdictions. The recommendations relate to improving the valuation of MMF portfolios, implementing measures for liquidity management in both normal and stressed market conditions, and requiring MMFs that maintain a constant NAV to convert to variable NAV where workable, and if not, to include safeguards to reinforce their resilience and ability to face significant redemptions.

As discussed earlier in this summary report under "Modernization of Investment Fund Product Regulation", the CSA amended NI 81-102 earlier in 2012 to introduce new liquidity and term restrictions on MMF holdings.

Other current initiatives of the IOSCO Investment Management committee include articulating principles for the valuation of collective investment schemes, for liquidity risk management and for the regulation of ETFs. IF Branch staff participated in the smaller working group established for the ETF project. Final publications of these papers are expected shortly. The Committee will also be working on defining criteria to identify "non-bank" systemically important financial institutions (in the area of asset management).

5. Feedback and Contact Information

If you have any questions regarding, or feedback on, our third annual summary report, please send them to [email protected].

You can find additional information regarding investment funds and the IF Branch on our website.

We have also attached a list of IF Branch staff at the end of this report.

INVESTMENT FUNDS BRANCH

|

NAME |

|

|

|

|

|

Goldberg, Rhonda -- Director |

|

|

|

|

|

Chan, Raymond -- Manager |

|

|

|

|

|

McKall, Darren -- Manager |

|

|

|

|

|

Nunes, Vera -- Manager |

|

|

|

|

|

Alamsjah, Rosni -- Administrative Assistant |

|

|

|

|

|

Asadi, Mostafa -- Legal Counsel |

|

|

|

|

|

Bahuguna, Shaill -- Administrative Support Clerk |

|

|

|

|

|

Barker, Stacey -- Senior Accountant |

|

|

|

|

|

Bent, Christopher -- Legal Counsel |

|

|

|

|

|

Buenaflor, Eric -- Financial Examiner |

|

|

|

|

|

De Leon, Joan -- Review Officer |

|

|

|

|

|

Fraser, Amy -- Review Officer |

|

|

|

|

|

Gerra, Frederick -- Legal Counsel |

|

|

|

|

|

Huang, Pei-Ching -- Senior Legal Counsel |

|

|

|

|

|

Jaisaree, Parbatee -- Administrative Assistant |

|

|

|

|

|

Joshi, Meenu -- Accountant |

|

|

|

|

|

Kearsey, Ian -- Legal Counsel |

|

|

|

|

|

Kwan, Carina -- Legal Counsel |

|

|

|

|

|

Lee, Irene -- Legal Counsel |

|

|

|

|

|

Leonardo, Tracey -- Administrative Assistant |

|

|

|

|

|

Mainville, Chantal -- Senior Legal Counsel |

|

|

|

|

|

Nania, Viraf -- Senior Accountant |

|

|

|

|

|

Oseni, Sarah -- Senior Legal Counsel |

|

|

|

|

|

Paglia, Stephen -- Senior Legal Counsel |

|

|

|

|

|

Persaud, Violet -- Review Officer |

|

|

|

|

|

Russo, Nicole -- Review Officer |

|

|

|

|

|

Schofield, Melissa -- Senior Legal Counsel |

|

|

|

|

|

Thomas, Susan -- Senior Legal Counsel |

|

|

|

|

|

Tjon, Stephanie -- Legal Counsel |

|

|

|

|

|

Tong, Louisa -- Administrative Assistant |

|

|

|

|

|

Welsh, Doug -- Senior Legal Counsel |

|

|

|

|

|

Yu, Sovener -- Accountant |

|

|

|

|

|

Zaman, Abid -- Accountant |

|