OSC Staff Notice 45-715 2017 Ontario Exempt Market Report

OSC Staff Notice 45-715 2017 Ontario Exempt Market Report

OSC STAFF NOTICE 45‐715

2017 ONTARIO EXEMPT MARKET REPORT June

1. EXECUTIVE SUMMARY

The exempt market is an important component of Ontario's capital market.{1} Investments through the exempt market have increased substantially in the last few years. In 2016, Ontario residents invested approximately $72 billion in over 2,500 non-investment fund issuers through prospectus-exempt offerings. Canadian issuers accounted for only 37% (or $27 billion) of the capital raised in Ontario, but represented almost two-thirds of issuers (or approximately 1,600 issuers) participating in Ontario's exempt market in 2016.

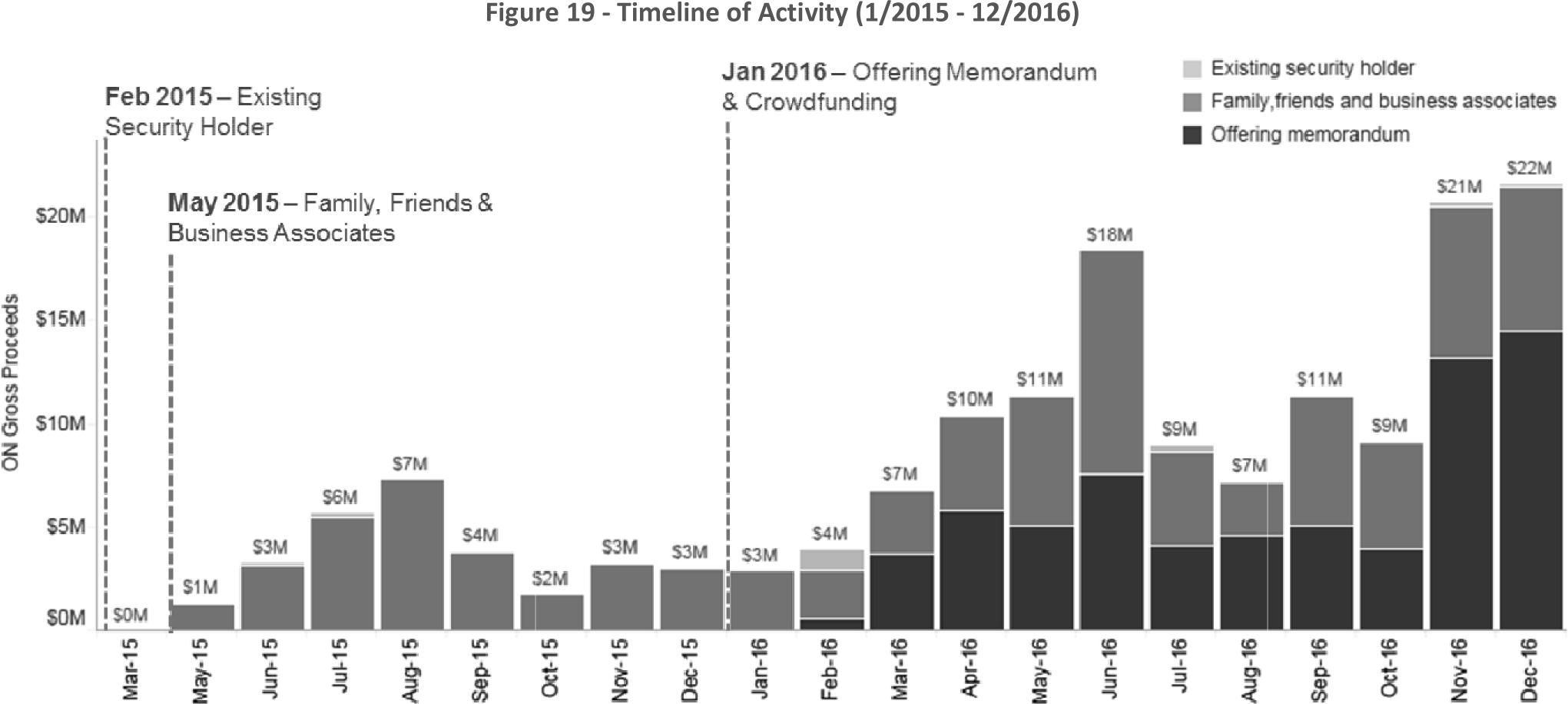

Recently, Canadian regulators adopted new prospectus exemptions to facilitate capital raising opportunities in the exempt market, especially for small and medium-sized enterprises (SMEs).{2} These new prospectus exemptions also formed the basis of the Ontario Securities Commission's (OSC) exempt market reform initiative which were aimed at expanding investment opportunities for all investors, especially retail investors, while maintaining appropriate investor protections. The recently introduced prospectus exemptions included the following:

• Existing security holder exemption -- February 11, 2015

• Family, friends and business associates exemption -- May 5, 2015

• Offering memorandum exemption -- January 13, 2016

• Crowdfunding exemption -- January 25, 2016

This report summarizes capital raising activity by non-investment fund issuers in Ontario's exempt market during 2015 and 2016. Additionally, the report examines capital formation by small Canadian issuers in Ontario's exempt market and the impact of the recently introduced prospectus exemptions.

In 2016, there was increased activity in Ontario's exempt market, especially by Canadian issuers. The key findings highlighted in the report include:

• Approximately 57% of Canadian issuers that participated in Ontario's exempt market were small issuers, which we defined as issuers raising less than $1 million annually. Notwithstanding the large number of small issuers, they only accounted for less than 1% of annual gross proceeds raised by Canadian issuers.

• In 2016, there was a notable increase in both the number of small Canadian issuers (30%) and the gross proceeds raised by these issuers (40%). The increased activity was concentrated among small Canadian issuers in three main industries: natural resources; consumer goods and services; and real estate and mortgage finance.

• Collectively, the new prospectus exemptions have gained traction among a sizeable proportion (25%) of Canadian issuers in the short period that they have been introduced. In 2016, approximately 400 issuers relied on the new prospectus exemptions to raise approximately $133 million, with close to half of these issuers raising capital in Ontario for the first time since 2014.

• Among issuers relying on the new prospectus exemptions, natural resource issuers represented the largest industry group by number of issuers (37%), whereas real estate and mortgage finance issuers accounted for most of the capital raised (70%).

• Accredited investors, mainly institutional investors, contributed over 90% of the total capital invested in the Ontario exempt market. However, most of the capital was invested in large issuers, primarily foreign-based and consisting of financial entities such as banks, private equity funds and asset-backed structured finance vehicles.

• Within the context of the broader Canadian capital market, Ontario's exempt market accounted for less than one-fifth of the total gross proceeds raised by Canadian issuers domestically and less than one-tenth of gross proceeds raised globally.

2. INTRODUCTION

SCOPE OF THE REPORT

With the recent reform of the exempt market regime now complete, the OSC's focus has shifted to monitoring the reforms and assessing whether they are achieving their expected regulatory outcomes, or if further regulatory responses are needed.{3}

The findings in this report provide a snapshot of the current state of Ontario's exempt market and a preliminary assessment of the market impact of these recent reforms from a capital raising perspective. The OSC's compliance and oversight efforts in the exempt market are on-going and outside the scope of this report.{4}

Further, the data and analysis in this report is limited to corporate (non-investment fund) issuers that raised capital from Ontario investors. We excluded investment fund activity to primarily focus on new capital formation by corporate issuers.

The focus of the report is as follows:

• Summarize Ontario exempt market activity and how it compares to the broader Canadian capital market

• Estimate capital formation by small Canadian issuers

• Assess the impact of recently introduced prospectus exemptions

WHAT IS THE EXEMPT MARKET?

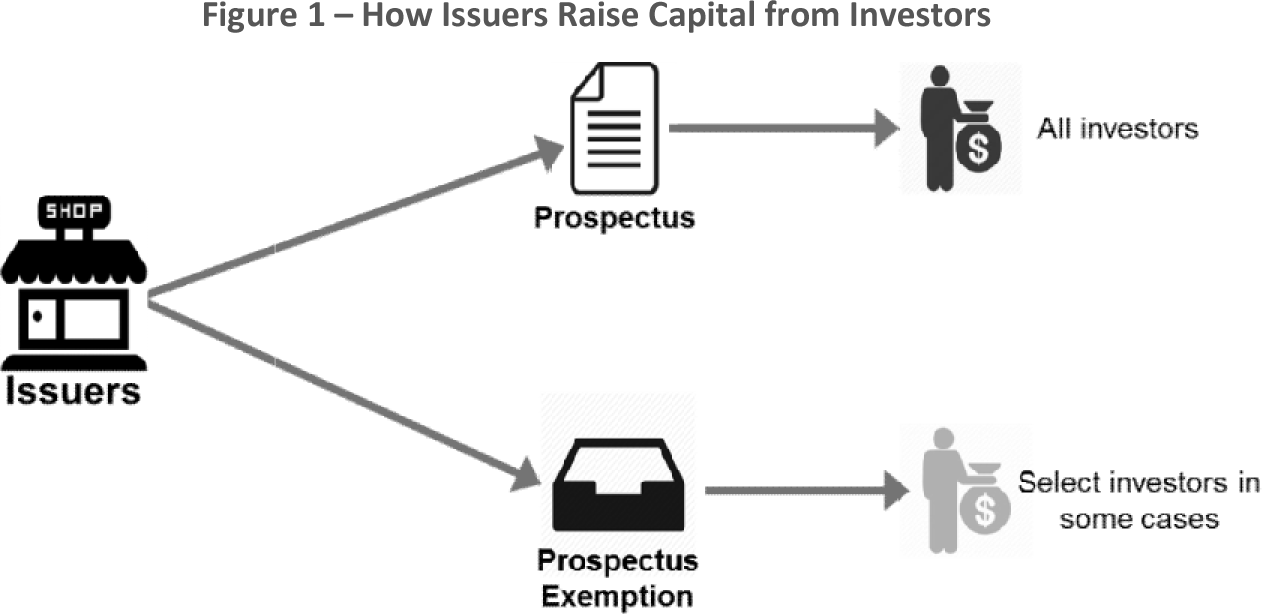

A company seeking to raise capital from investors may, generally, distribute securities either:

• under a prospectus, or

• without a prospectus, in reliance on a prospectus exemption.

One of the key principles of Canadian securities law is that securities may not be distributed unless a prospectus is filed with a Canadian securities regulator. A prospectus is a comprehensive disclosure document that sets out detailed information about an issuer and describes the securities being issued and the risks associated with purchasing those securities. An issuer that obtains a receipt from a Canadian securities regulator for a prospectus becomes a reporting issuer and can then use the prospectus to offer and sell securities to the public (i.e. all investors). Companies that are reporting issuers must regularly make certain information about their activities and financial status available to the public. These reporting issuers may also choose to publicly list their securities on a Canadian stock exchange such as the Toronto Stock Exchange (TSX).

In certain cases, securities may be offered without a prospectus, in reliance on certain prospectus exemptions. The "exempt market" describes the segment of our capital markets where securities can be sold without the protections afforded by a prospectus. Such offerings are sometimes also referred to as private placements or exempt distributions. Most exemptions from the prospectus requirement are set out in Part XVII of the Securities Act (Ontario) (the Act), OSC Rule 45-501 Ontario Prospectus and Registration Exemptions (OSC Rule 45-501) and National Instrument 45-106 Prospectus Exemptions (NI 45-106). Each prospectus exemption has its own rules about who can sell securities and who can buy securities under the specified exemption.

Generally speaking, each prospectus exemption is premised on a specific policy rationale that justifies not requiring a prospectus and, consequently, the distribution may be limited to certain classes of investors with specific attributes. These prospectus exemptions can help an issuer raise money without incurring the time and expense of preparing a prospectus. Investors who buy securities through prospectus exemptions generally do not have the benefit of ongoing information about the issuer or the security that they are investing in. As well, they often do not have the ability to easily resell the security.

Companies that are reporting issuers may also rely on prospectus exemptions to raise capital.

MARKET PARTICIPANTS

There are three key stakeholders in the exempt market: issuers, investors and, in some transactions, intermediaries such as underwriters or dealers that assist in brokering transactions between issuers and investors. Issuers across all sectors and from both Canadian and foreign jurisdictions can access Ontario's exempt market.

Among investor types, institutional investors (e.g. pension funds and asset management firms) and other non-individual entities (e.g. investment trusts and corporations) typically account for most of the invested capital in the exempt market. The remaining investors are considered to be retail investors, comprised of mostly high-net-worth individuals, angel investors or individuals related to the issuer.

In some exempt market offerings, intermediaries such as underwriters, investment dealers or exempt market dealers may be involved.{5} Traditionally, the intermediary role was delegated to an individual or group of individuals; however, more recently, a few registered on-line portals have also been facilitating these exempt market offerings.

DATA UNDERLYING THE ANALYSIS

The data underlying the analysis in this report is collected from Form 45-106F1 Report of Exempt Distribution ("the Report") filed with the OSC by non-investment fund issuers that raised capital from Ontario investors. Generally, issuers are required to file the Report within 10 days of the first distribution date. Therefore, an issuer in continuous distribution over a period longer than 10 days is required to file multiple Reports to cover the distribution period.

Only certain prospectus exemptions trigger a requirement to file a Report and so the information gathered from the filings does not represent all exempt market activity. For more information on which exemptions require the filing of a Report, see Part 6 of NI 45-106. For example, issuers with fewer than 50 investors (excluding current and former employees) can rely on the private issuer exemption under subsection 73.4(2) of the Act to raise capital and would not be required to file a Report.{6}

The version of the Report in effect prior to June 30, 2016 ("Prior Report") required limited information about the issuer. Further, the data was collected in a less structured format than is the case for the current Report that became effective on June 30, 2016.{7}

The findings in this report incorporate a number of interpretations and assumptions by OSC staff based on knowledge of the Ontario exempt market and experience analyzing the reported information. The information analyzed was obtained from both the Prior Report and the current Report and was provided by filers at a point in time and may have been updated over time to reflect filer amendments.

3. ONTARIO EXEMPT MARKET ACTIVITY

In this section, we provide an overview of capital raising activity in Ontario for 2015 and 2016, identify the types of issuers that have accessed the exempt market, discuss characteristics of prospectus-exempt offerings and assess trends over the period. Lastly, we provide some context to better understand how Ontario's exempt market fits within the broader Canadian capital market.

MARKET SIZE

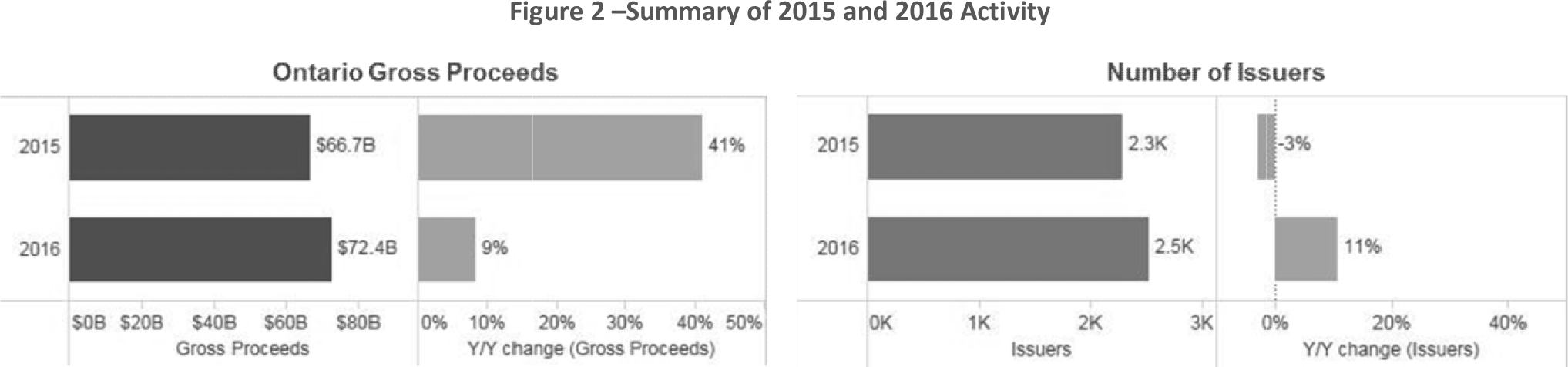

Annual gross proceeds raised from Ontario investors have continued to grow in the last few years. In 2015, annual gross proceeds increased by approximately 40% to $67 billion. In 2016, annual gross proceeds grew by an additional 9% to approximately $72 billion. Despite the large dollar increase in 2015, the number of issuers accessing Ontario's exempt market dropped slightly by 3%, whereas in 2016 there was an 11% increase in issuer participation.

There are several key factors that drive capital raising activity in general, with business or economic sentiment being one of the most important. The large increase in gross proceeds in 2015 was primarily driven by larger U.S. deal activity, whereas in 2016, there appears to have been an increase in the number of Canadian issuers accessing the exempt market. Economic growth expectations were higher in the U.S. than other regions throughout much of 2015.{8} In addition, there were record debt issuances in the U.S prompted by expectations that the Federal Reserve would start raising interest rates by late 2015.{9} In Canada, overall growth has been muted over the last two years with pockets of growth in certain sectors, such as real estate and mining.

ISSUER LOCATION

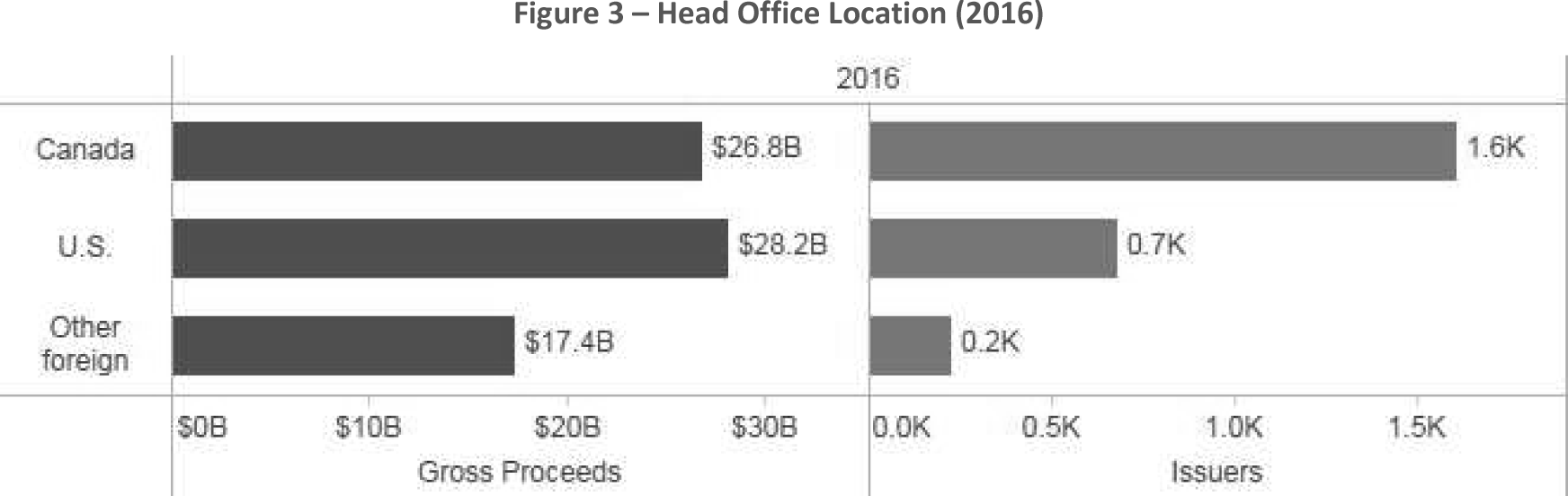

Ontario's exempt market is accessed by both Canadian and foreign issuers. Almost two-thirds of issuers are headquartered in Canada, but a diverse set of foreign issuers are also very active in raising capital from Ontario investors. U.S. based issuers represent the second largest group of exempt market issuers in Ontario. Foreign issuers raised the majority of capital in the Ontario exempt market, and U.S. based issuers accounted for the largest share.

In 2016, approximately 1,600 Canadian issuers raised capital from Ontario investors representing a 22% increase from the previous year. Despite this increase, annual gross proceeds raised over the last two years remained relatively flat, indicating a drop in the average offering size of Canadian issuers.

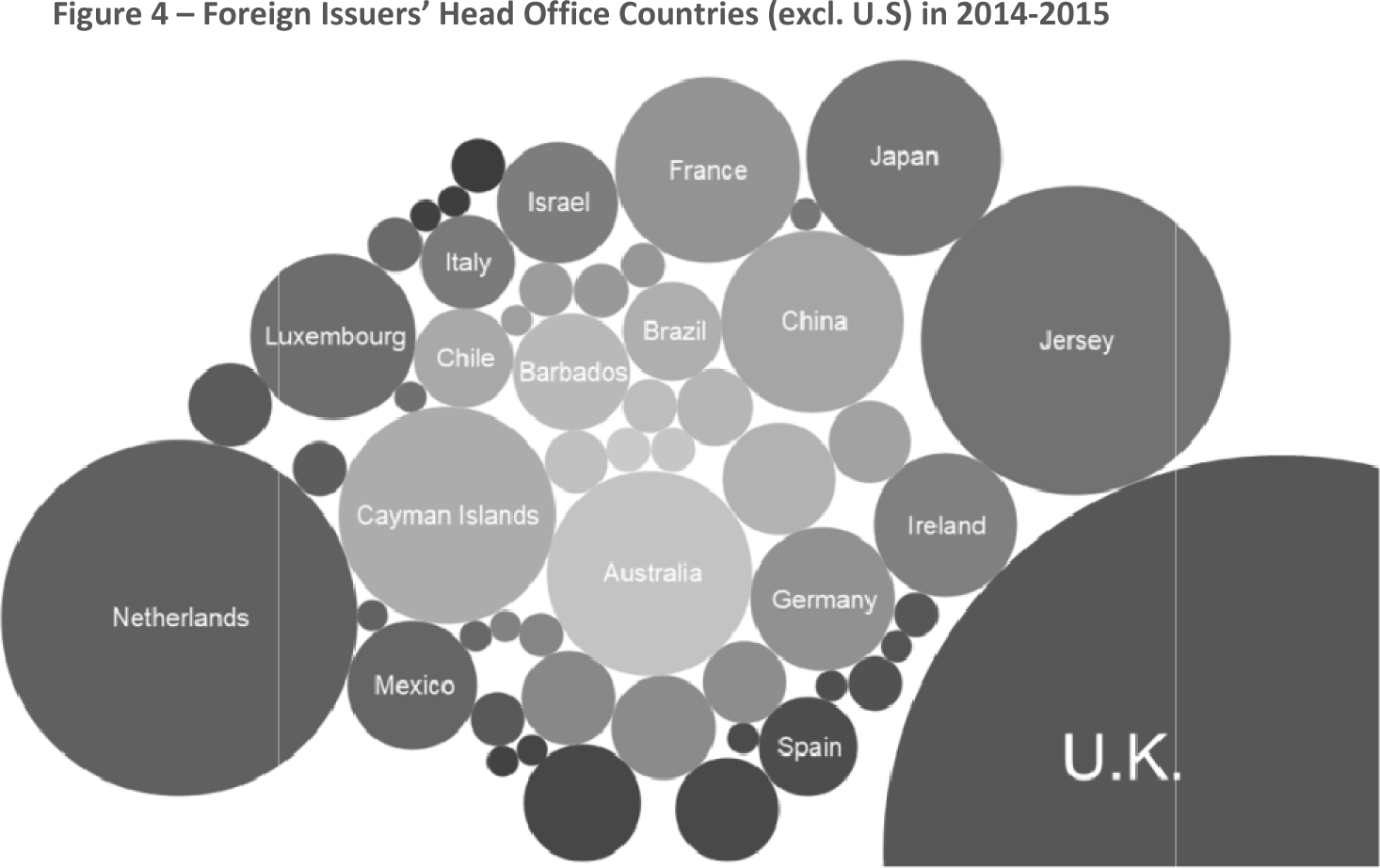

In contrast, foreign issuers experienced an increase in annual gross proceeds raised (13%) while the number of foreign issuers fell slightly by approximately 4% over the same period. Most foreign-based issuers are established businesses or multinationals capable of attracting international investment dollars. Among the non U.S.-based foreign issuers, many were financial entities headquartered in popular off-shore financial centers such as Luxembourg, Jersey and the Cayman Islands.

INDUSTRY GROUPS

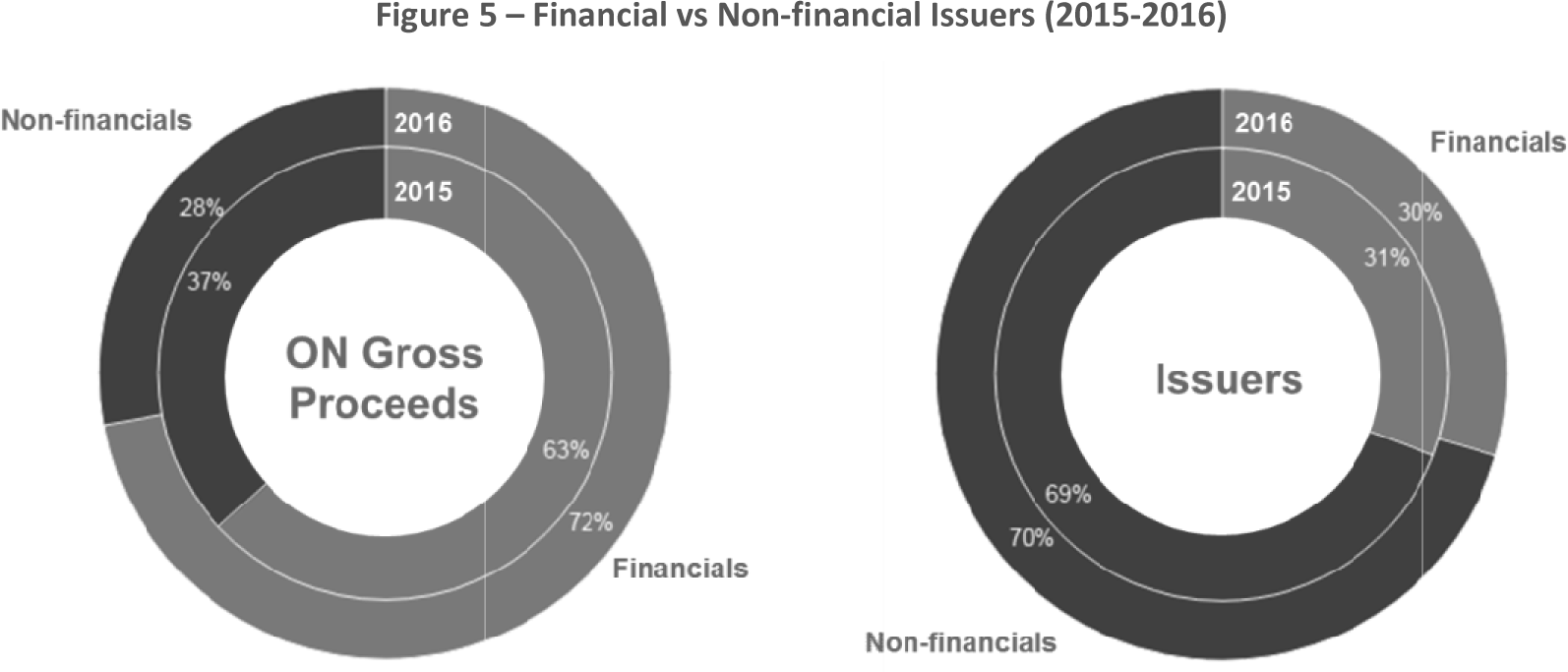

Financial issuers represented less than one-third of all issuers that raised capital in Ontario's capital market in 2016, but accounted for over 70% of the gross proceeds raised. Not surprisingly, the average or median offering size for financial issuers was several times larger than for non-financial issuers. This breakdown between financial and non-financial issuers is consistent across issuers based in Canada and abroad, in both exempt and public markets.

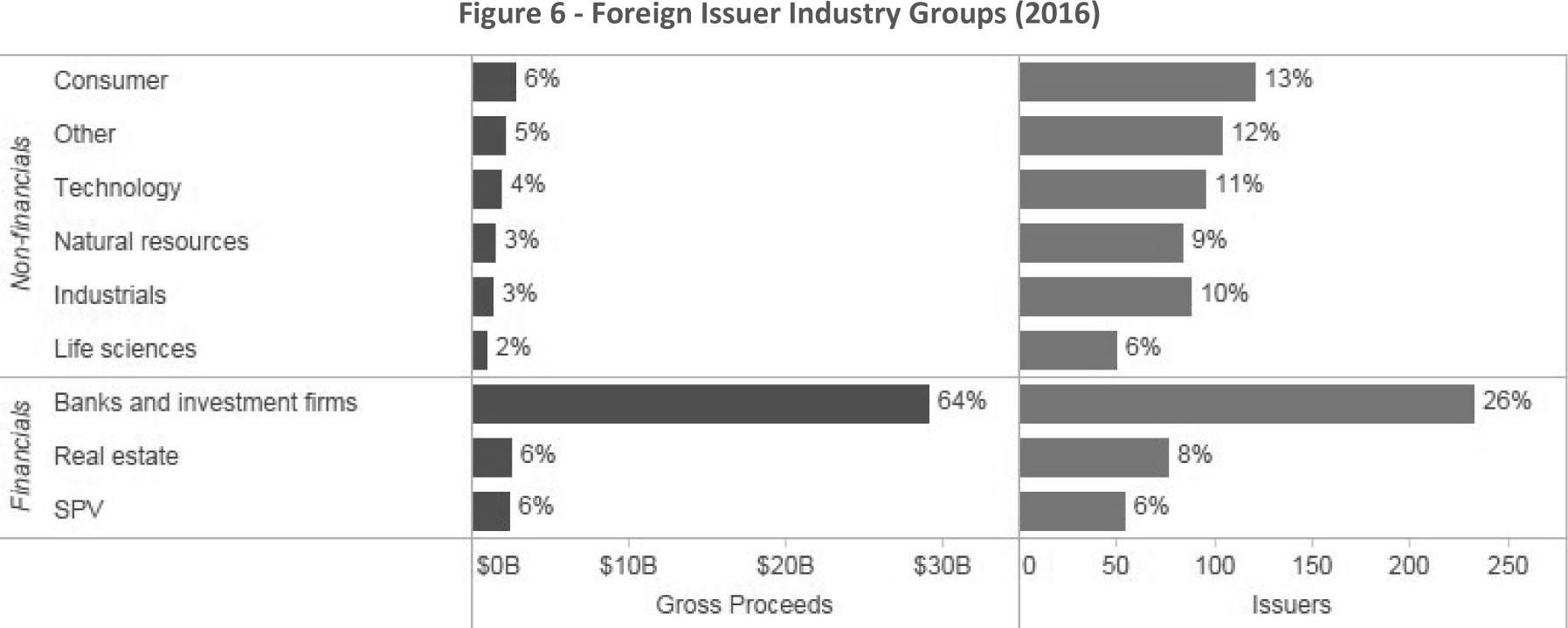

Among foreign issuers, financial issuers consisting primarily of banks and investment firms (like private equity funds) were the most predominant industry group.{10} This industry group represented over a quarter of all foreign issuers and accounted for almost $30 billion, or 64% of total gross proceeds raised by foreign issuers. The total capital raised across other foreign industry groups was significantly smaller, although in aggregate they account for a disproportionately larger number of issuers.

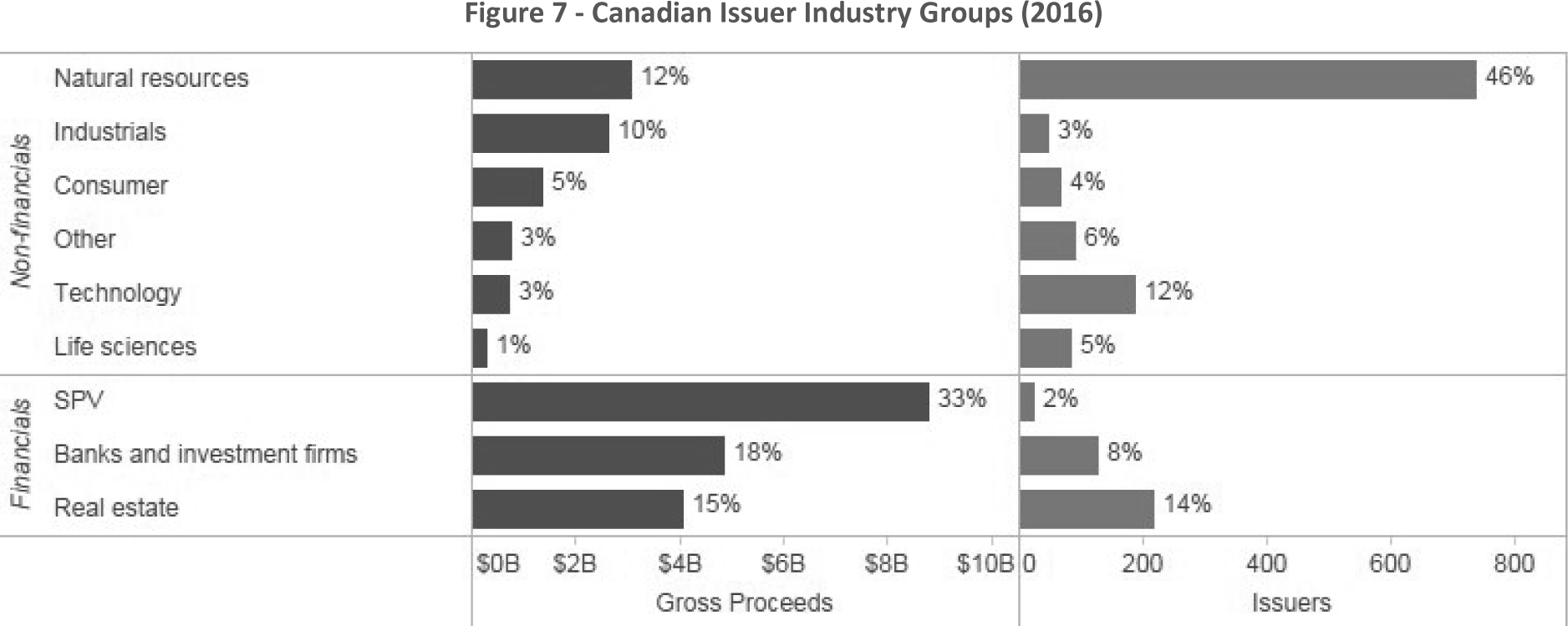

Ontario's exempt market is an important financing source for Canadian issuers, especially those in the junior mining industry. In 2016, more than 700 mining and energy ("natural resources") issuers raised approximately $3 billion from Ontario investors. Issuers in the natural resources sector (predominantly mining) accounted for almost half of all Canadian issuers in Ontario's exempt market and raised more capital than other non-financial sectors, but had the lowest average and median offering sizes of any industry group. Technology, media and telecom ("technology") and healthcare, biotech and pharmaceutical ("life sciences") issuers were also quite active by number of issuers, accounting for almost 20% of Canadian issuers but raised less than 5% of gross proceeds in 2016.

For Canadian issuers, special purpose vehicles and similar financing entities ("SPV") raised the most capital, approximately $9 billion or 33% of total gross proceeds in 2016. Examples of these issuers include asset-securitization vehicles that primarily structured large debt offerings backed by consumer auto loans and credit card receivables. SPV issuers accounted for less than 2% of all Canadian issuers in 2016, and therefore raised the highest average and median offerings amounts compared to Canadian issuers in other industry groups.

The unprecedented growth in Canadian property prices and low interest rates have fueled much of the investment activity in real estate and mortgage finance ("real estate") issuers in recent years. Real estate issuers raised approximately $4 billion or 15% of gross proceeds in 2016 and were the second largest group of Canadian issuers (14%) in the exempt market in 2016. Most of these real estate issuers were real estate investment trusts (REITs) or mortgage investment entities (MIEs).

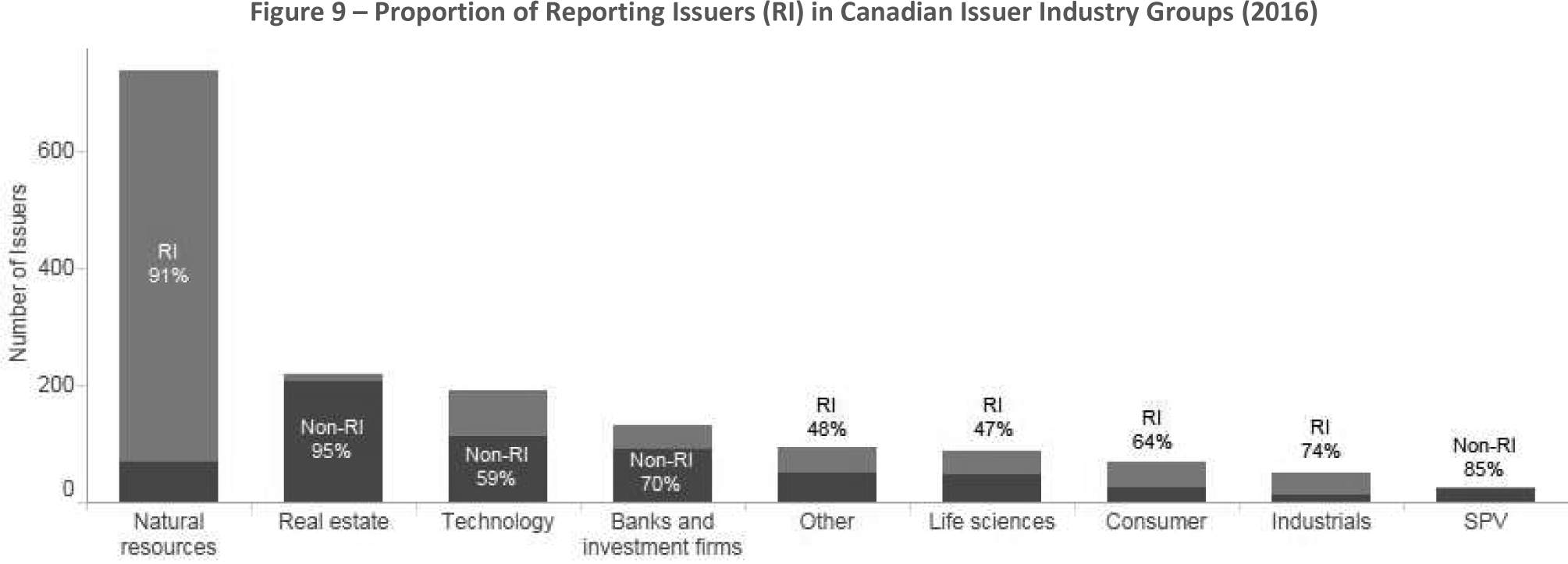

REPORTING ISSUERS

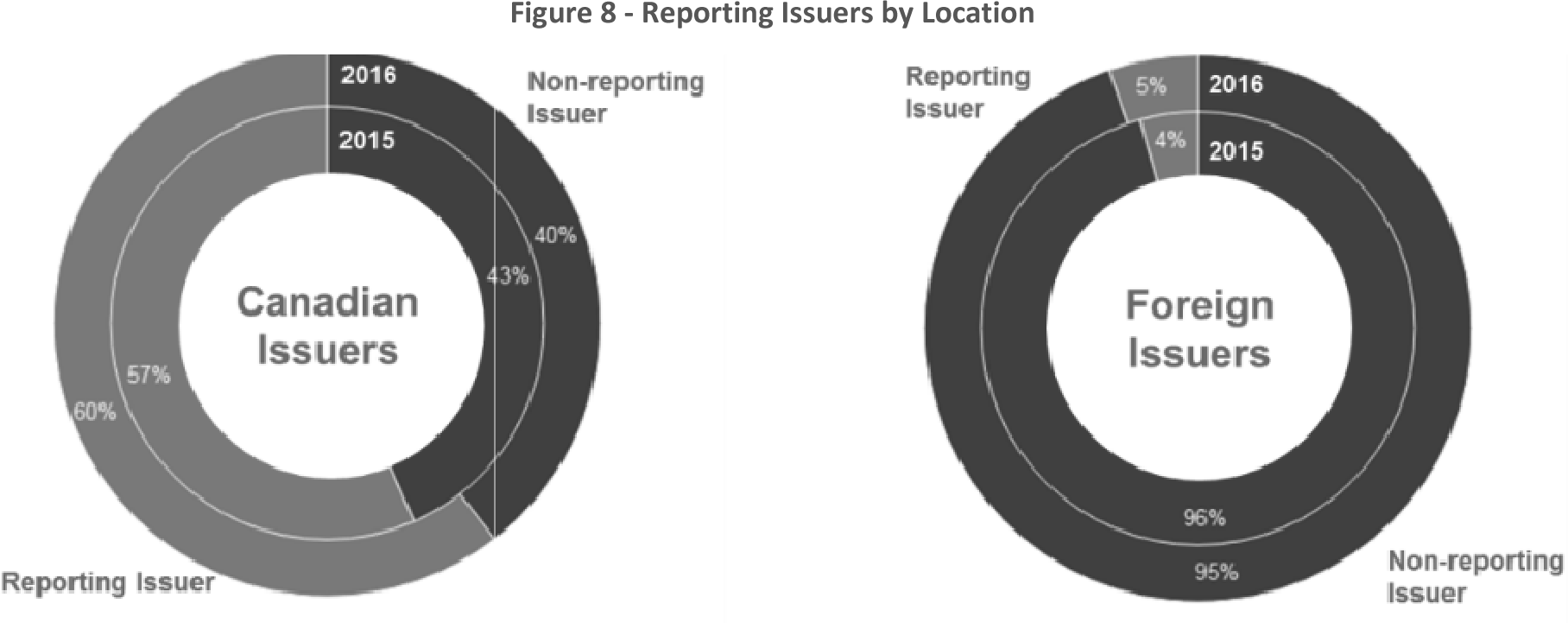

Although most reporting issuers are listed on one of three Canadian stock exchanges and can access capital through prospectus offerings, they account for 60% of exempt market activity by Canadian issuers. Although 95% of foreign issuers participating in Ontario's exempt market are non-reporting in Canada, some are publicly listed entities in their home jurisdictions and have associated reporting obligations.

Reporting issuers, especially those listed on the TSX Venture (TSXV) exchange have commonly relied on the exempt market for secondary or follow-on financings. In 2016, approximately 70% of Canadian reporting issuers that raised capital in the exempt market were in the natural resources industry. Within industry groups, reporting issuers accounted for the majority (90%) of all Canadian natural resources issuers in Ontario's exempt market and also a sizable proportion of issuers in other non-financial industry groups. However, most Canadian financial issuers that raised capital in Ontario's exempt market, especially in the real estate industry, were non-reporting issuers.

PROSPECTUS EXEMPTION RELIED ON

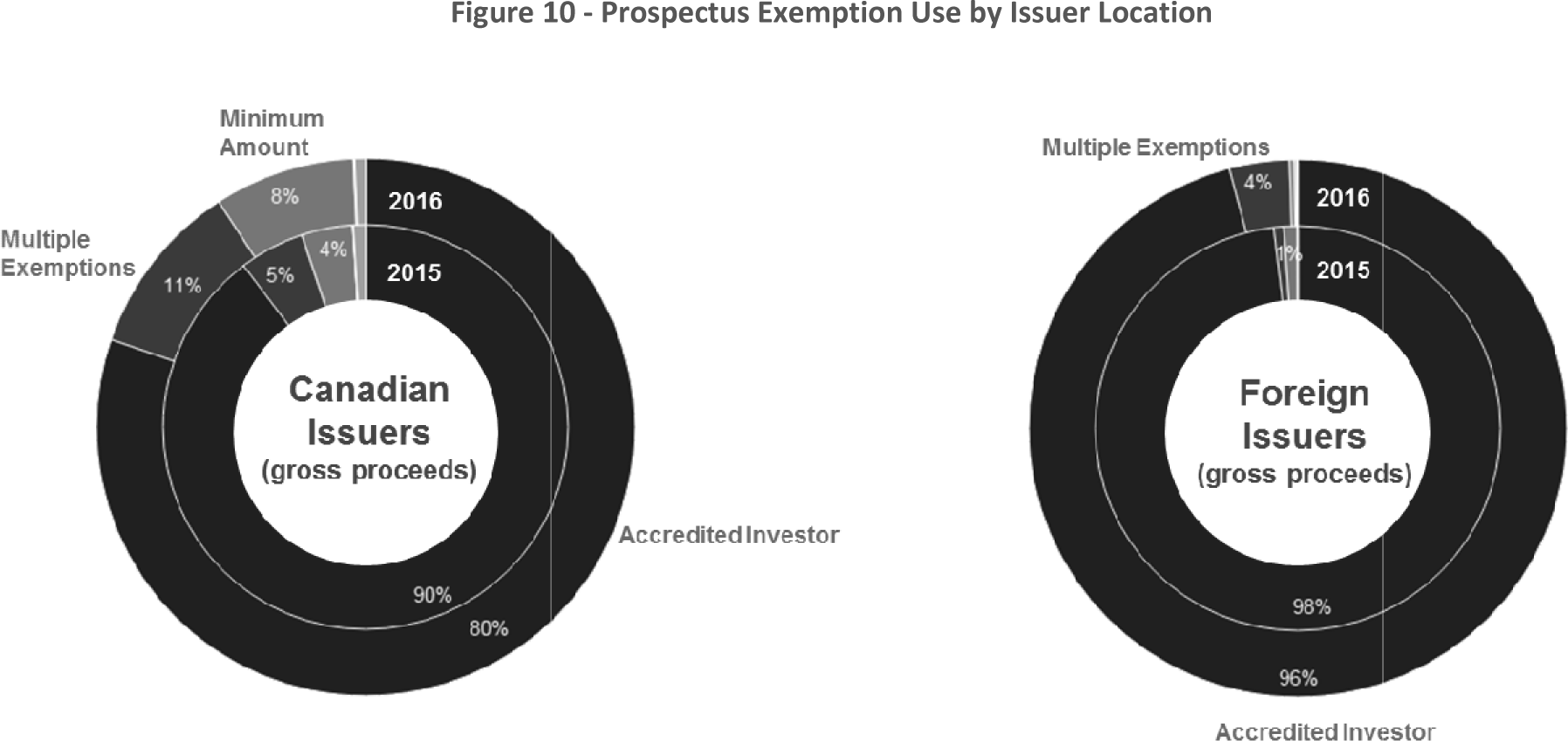

An investor may need to satisfy certain criteria in order to invest under a specific prospectus exemption. For example, the family, friends and business associates exemption allows issuers to raise capital from investors who qualify as family members, close personal friends or close business associates of the principals of the issuer. Alternatively, the accredited investor exemption is limited to persons who qualify as accredited investors{11}. Accredited investors are a vital funding source for issuers in the exempt market and represent a wide spectrum of investors, from high income or high net-worth individual investors to institutional investors such as pension funds, insurance firms and asset management firms.

Foreign issuers have predominantly raised capital under the accredited investor exemption. Canadian issuers have also primarily used the accredited investor exemption which accounts for approximately 90% of gross proceeds raised in Ontario. The minimum amount exemption was relied on to raise the second highest amount of capital (approximately $2 billion or 8% of gross proceeds in 2016) among Canadian issuers. All other exemptions account for less than 2% of capital raised in the exempt market by Canadian issuers. However, when analyzing the proportion of issuers that relied on these prospectus exemptions, the recently introduced family, friends and business associates exemption was the second most relied on exemption after the accredited investor exemption.

An issuer can rely on more than one exemption to raise capital either from investors within the same jurisdiction or across Canada. In 2016, about 30% of Canadian issuers relied on multiple prospectus exemptions which accounted for about 11% of gross proceeds raised. Among these issuers, the accredited investor exemption was predominantly used and also accounted for most of the capital raised under multiple prospectus exemptions.

TYPE OF SECURITIES OFFERED

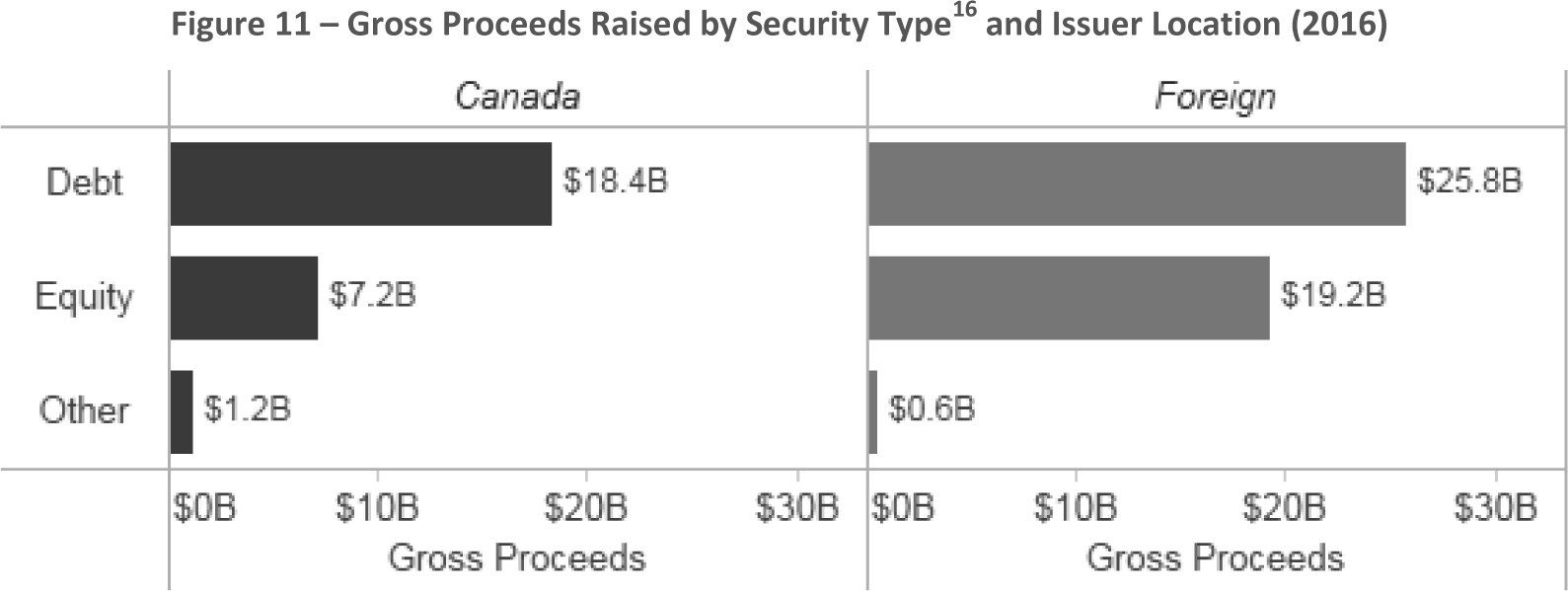

In recent years, low interest rates have made debt a much more attractive financing option for issuers.{12} For both Canadian and foreign issuers, debt offerings raised more capital than equity offerings. This is commonly observed within the broader capital markets as well (see below). According to the pecking order theory, certain firms tend to prefer debt over equity to finance their business.{13} Although the choice is inherently more complex for most issuers, some empirical evidence supports this theory, especially among larger firms with less volatile earnings and net positive cash flows.{14} For small issuers, especially in the high-growth and knowledge-based industries, obtaining debt capital is more challenging than equity capital.{15}

16 The "Other" category included securities that could not be classified as either debt or equity related securities and also instances where multiple security types were issued.

Financial issuers raised the largest share of debt capital proceeds through notes, bonds and debentures of varying rates, seniority and maturities. Many institutional investors, especially pension plans and insurance firms, allocate a sizeable proportion of their investments to fixed income securities which provide income-paying assets that match their long-term liabilities.{17}

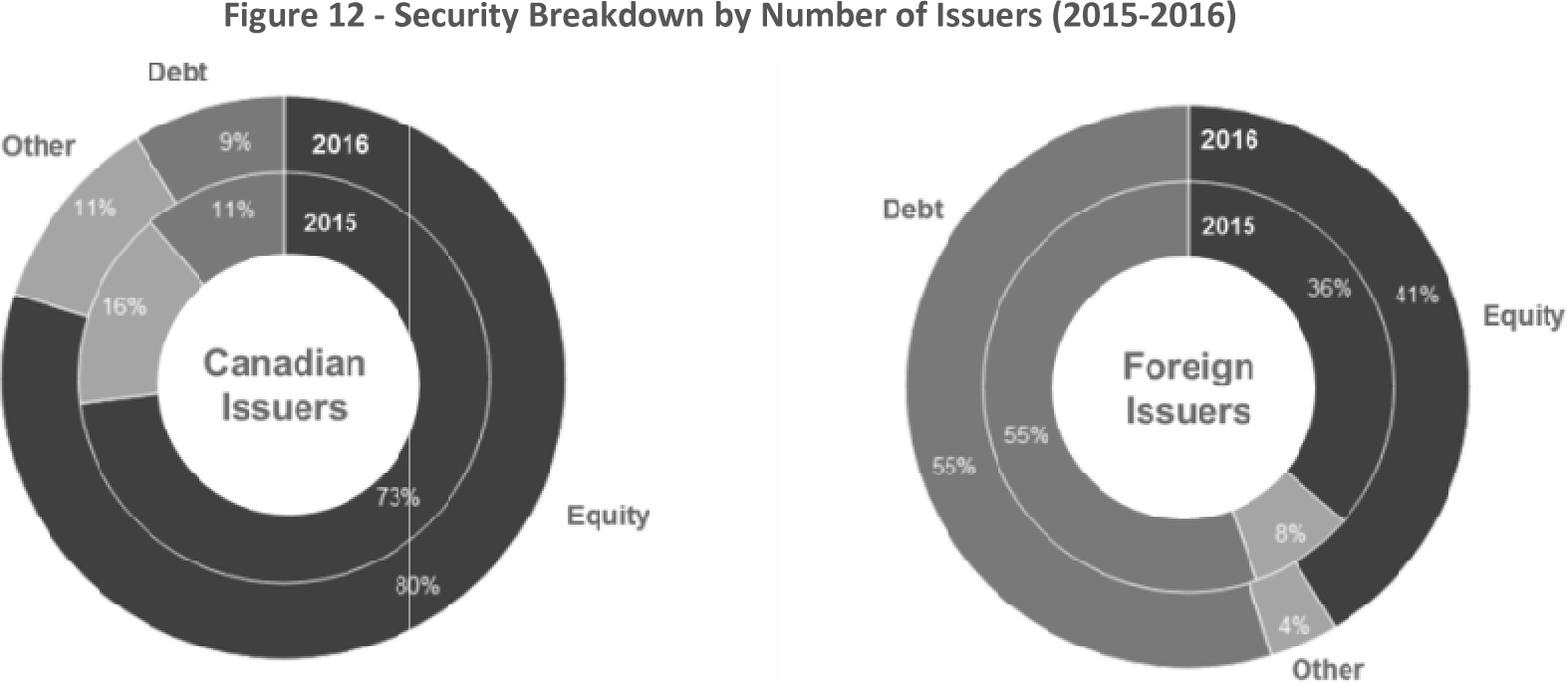

Given the heavy concentration of junior mining issuers, it is not surprising that most Canadian issuers distributed equity securities. Excluding mining issuers, three out of four Canadian issuers raised capital by issuing some form of equity security in 2016. Less than 10% of Canadian issuers offered debt securities, but these issuers raised the most capital (68% or $18.2 billion) in 2016. SPV issuers were responsible for approximately $9 billion or 50% of the debt proceeds raised by Canadian issuers over the same period.

Similarly, among foreign issuers, debt was offered by financial issuers such as banks and insurance firms, followed closely by large multinationals and blue chip issuers from a range of non-financial industry groups. Close to half of all foreign issuers that raised equity capital were private equity firms and similar investment entities. The remaining foreign issuers that distributed equity represented a mix of non-financial industries.

FINANCING SIZE

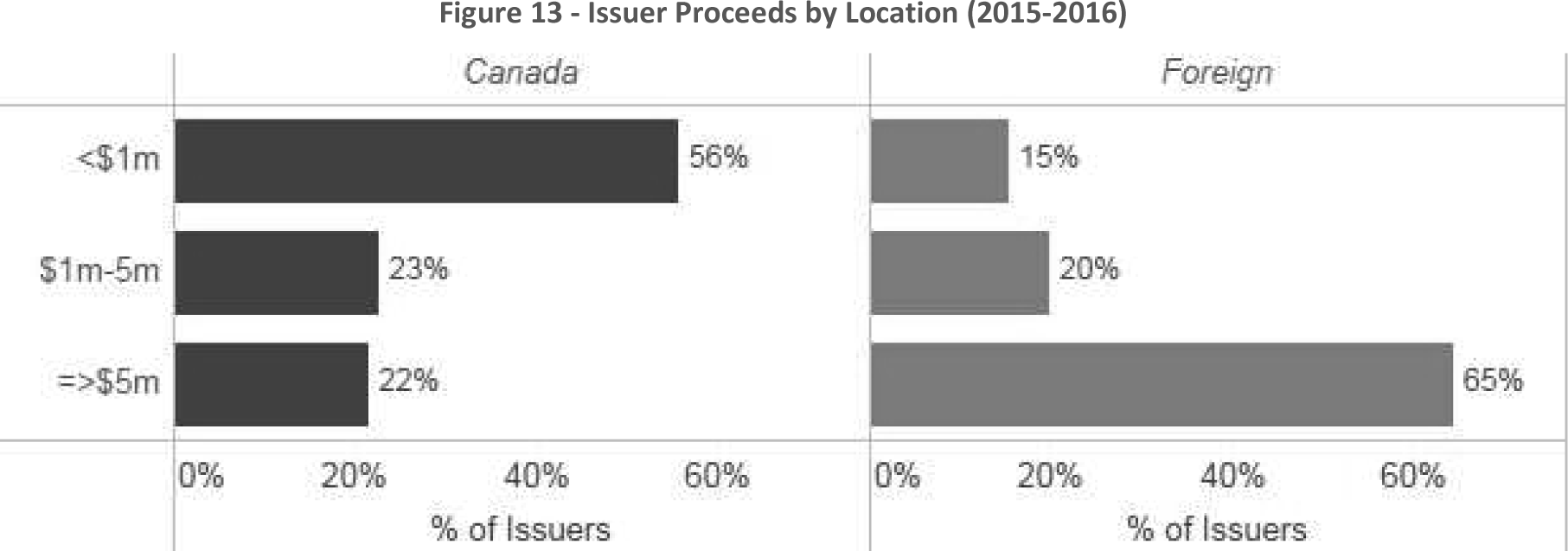

A comparison of issuers' average annual offering sizes further confirms that most foreign issuers in the exempt market raised more capital than Canadian issuers. Over the last two years, approximately 65% of foreign issuers raised an annual average of at least $5 million compared to just 22% of Canadian issuers. Furthermore, over half of all Canadian issuers in the exempt market raised on average under $1 million annually compared to just 15% of foreign issuers.

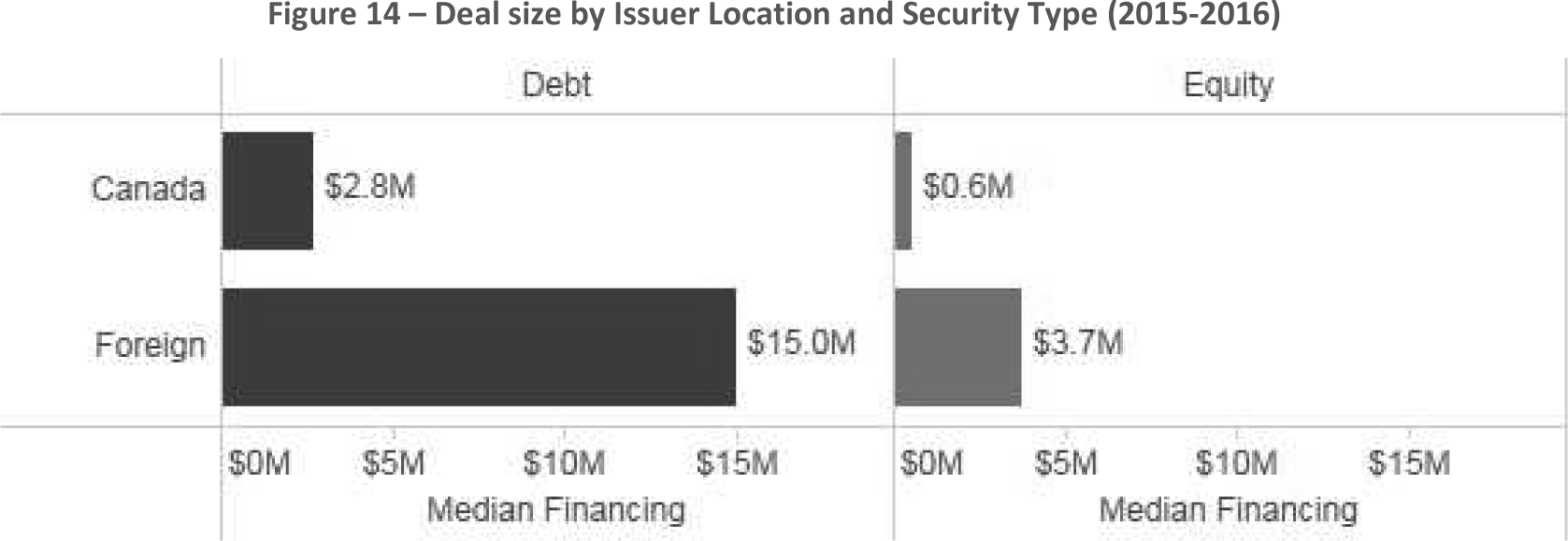

The lower average and median financing sizes of Canadian issuers compared to foreign issuers was consistent across debt and equity offerings as well. The median financing size of Canadian debt issuers was five times lower than the median financing size of foreign issuers. Similarly, half of all equity offerings by Canadian issuers were less than $600,000, whereas the median financing size for foreign issuers was closer to $4 million.

COMPARISONS WITH THE BROADER CANADIAN CAPITAL MARKET

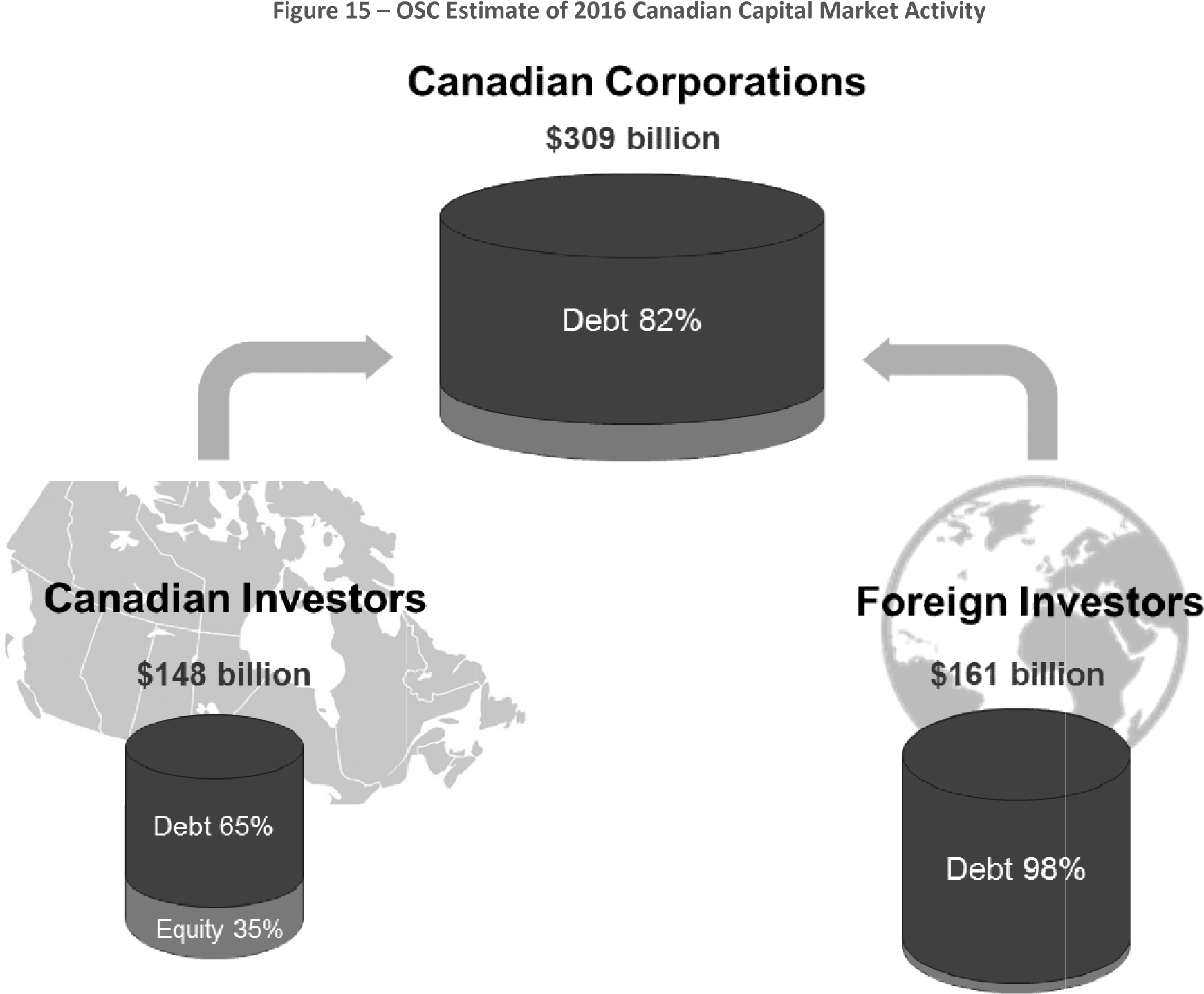

Canadian corporations issued approximately $309 billion in securities through both private (which includes the exempt market) and public market offerings in 2016.{18} Canadian investors accounted for less than half of that amount or approximately $148 billion, with the remainder coming from foreign investors. In comparison, Ontario residents invested approximately $27 billion in Canadian issuers in 2016 through exempt market offerings that triggered a filing requirement with the OSC.{19}

Hence, the Ontario exempt market accounted for less than 20% of the gross proceeds raised by Canadian issuers domestically and less than 10% of gross proceeds raised by Canadian issuers globally. The difference of approximately $121 billion ($148 billion -- $27 billion) in domestic proceeds raised by Canadian issuers can be attributed to the following three components:

• public market offerings;

• exempt market offerings in other Canadian jurisdictions; and

• senior debt issued by Canadian financial institutions which are carved out of prospectus and reporting requirements.{20}

Debt issued by financial institutions represents a significant proportion of the capital raised in both the Ontario exempt market and the broader Canadian capital market.{21} It is important to note that the Canada-wide statistics are captured through the reporting obligations of intermediaries (i.e. underwriters and dealers) and, therefore, would mostly capture large to medium-sized offerings. Smaller transactions in the broader Canadian exempt market would not be captured in the Statistics Canada data but may be required to be reported under certain prospectus exemptions.

Lastly, as discussed above, there is a portion of exempt market activity that remains unknown because insubstantial amounts were raised or the offerings involved closely-held issuers with fewer than 50 investors (excluding current and former employees). These issuers would not be captured in the data we have presented.

4. CAPITAL FORMATION BY SMALL CANADIAN ISSUERS

Facilitating capital formation for issuers, particularly small issuers, has been an important priority for the OSC. Capital allocation, especially in the exempt market, is largely opaque. Further, the information gap is worse for small businesses because there are limited or no reporting requirements and financing sources are highly fragmented.{22} In this section, we focus further on Canadian issuer activity and estimate the scope of capital formation by small Canadian issuers.

ESTIMATING SMALL CANADIAN ISSUERS

Industry Canada estimates that as of December 2015, there were approximately 1.17 million businesses with employees and approximately 98% of these businesses were small businesses.{23} Industry Canada has traditionally identified businesses with fewer than 500 employees as SMEs. Small businesses are identified as having between 5 and 100 employees and micro-businesses as having fewer than 5 employees. Statistics Canada uses a combination of employment size thresholds that are identical to Industry Canada, but also includes revenues to define SMEs.

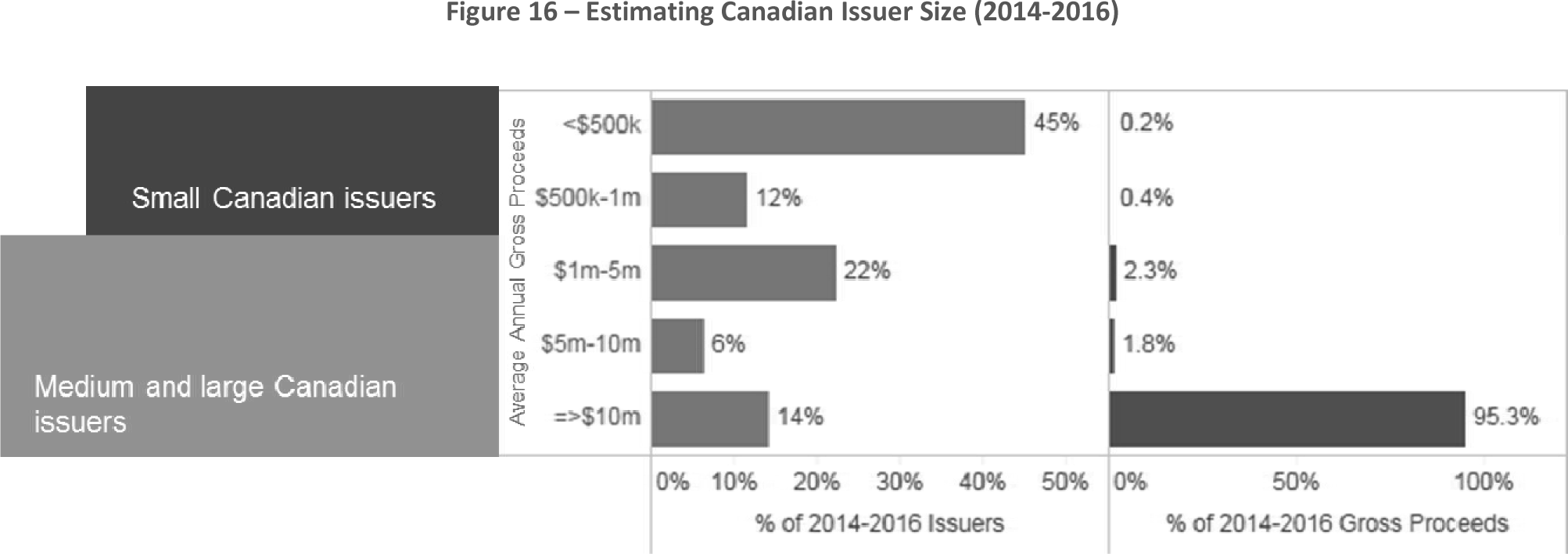

In the absence of these metrics, we rely on the annual amounts raised by an issuer as a proxy for issuer size.{24} Intuitively and based on our observations, the relative size of an issuer has been found to broadly correlate with how much capital an issuer raises. Although, there may be some instances of issuers raising amounts outside their typical range, the overall correlation between issuer size and offering size appears to be strong, especially for offerings of under $1 million. Issuers raising proceeds under $1 million were predominantly small businesses. Transaction costs for capital market offerings increase as firms grow larger and become more complex; therefore, offering sizes of below $1 million may not be feasible or even sufficient to cover transaction cost of most large issuers. Accordingly, for the purposes of our analysis, we consider Canadian issuers to be "small" issuers if they raised less than $1 million annually.{25}

SMALL CANADIAN ISSUERS IN ONTARIO'S EXEMPT MARKET

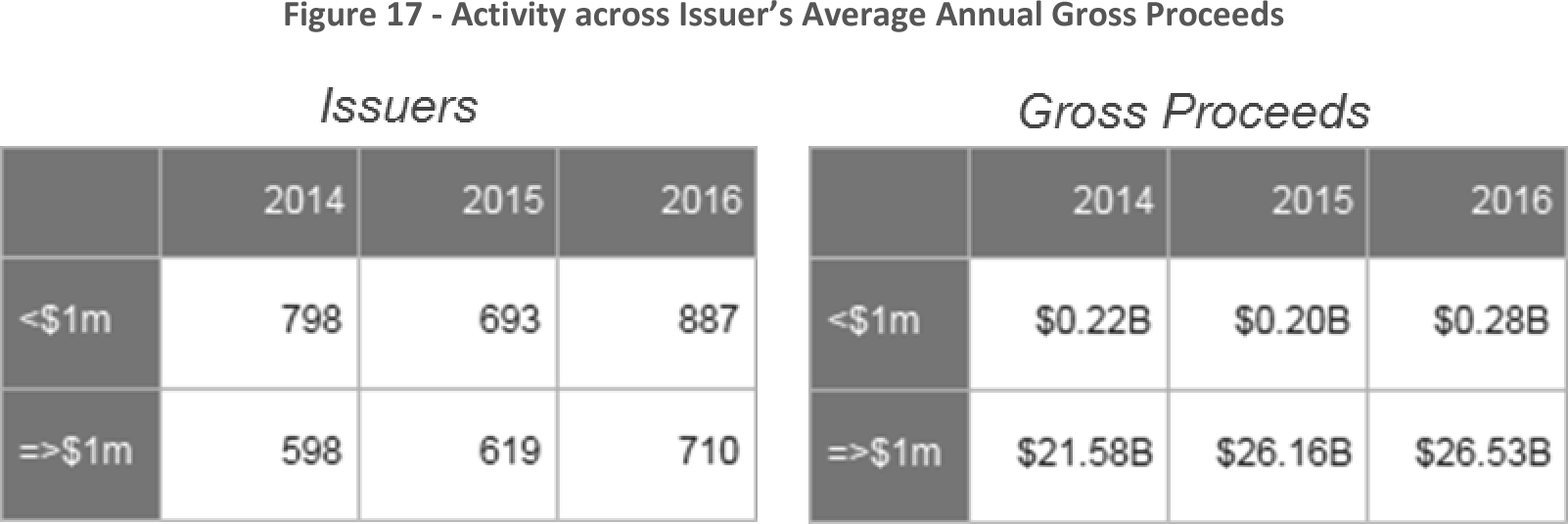

We estimate that between 2014 and 2016, approximately 57% of Canadian issuers in Ontario's exempt market were small issuers. However, these issuers represented less than $300 million or 1% of gross proceeds raised in Ontario's exempt market by Canadian issuers annually.

There has been a notable increase in small Canadian issuer activity within the Ontario exempt market in 2016 after experiencing a relative drop in 2015. In 2016, the number of small Canadian issuers that obtained exempt market financings increased by almost 30% and gross proceeds raised also jumped by approximately 40% year-over-year.

The industry breakdown of these small Canadian issuers is very similar to that of the junior Canadian exchanges particularly the TSXV exchange. This is not surprising since approximately 70% of the small Canadian issuers identified above were found to be reporting issuers. Similar to the TSXV exchange, there is a high concentration of issuers from the natural resources industry followed by issuers in the technology and life sciences industry groups.

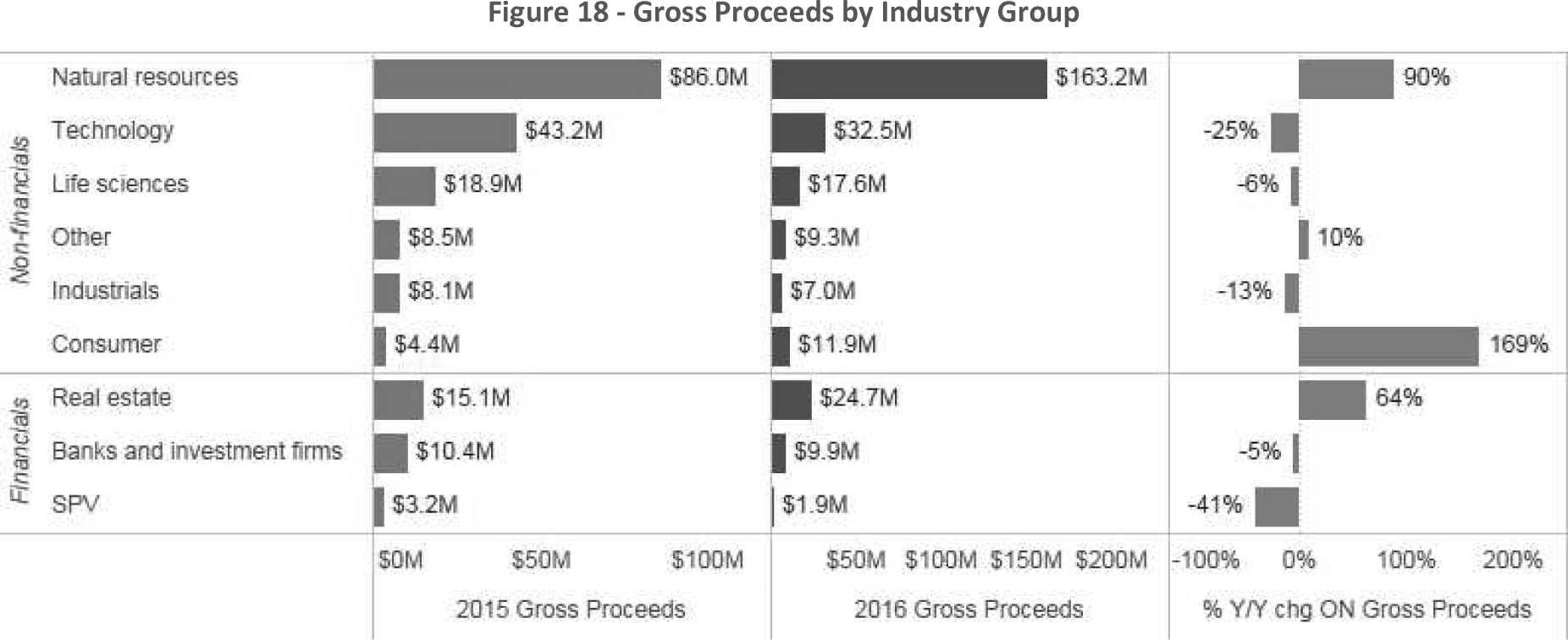

The increased level of exempt market offerings by small Canadian issuers in 2016 was mainly concentrated among issuers in the natural resources, consumer goods and services ("consumer") and real estate industries. All other industry groups either experienced a decline or a nominal change in the number of issuers and the amount of capital raised in the exempt market.

5. IMPACT OF RECENTLY INTRODUCED PROSPECTUS EXEMPTIONS

Collectively, the new prospectus exemptions have gained traction among a sizeable proportion of Canadian issuers in the short period that they have been introduced. In this section, we highlight the impact of these new exemptions.

ACTIVITY UNDER THE NEW EXEMPTIONS

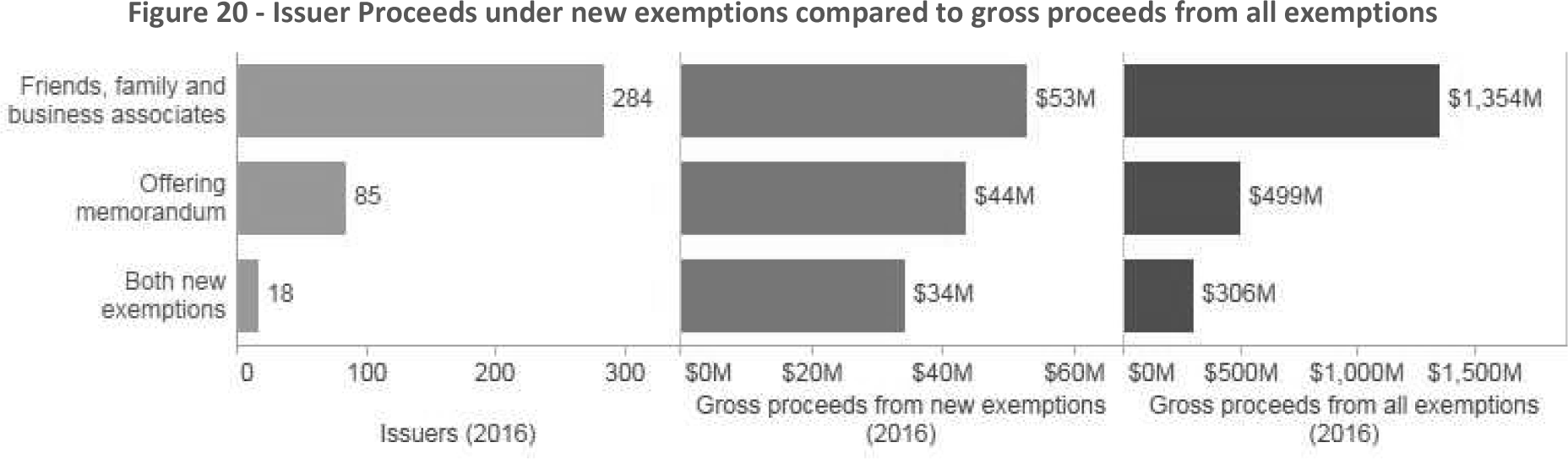

From the date they became effective to December 31, 2016, the new exemptions have been used to raise a total of $163 million. However, most of this activity occurred in 2016, when approximately $133 million was raised under the new prospectus exemptions in Ontario by 401 issuers. More specifically, the number of issuers and capital raised under the new exemptions in 2016 are as follows:{26}

• The family, friends and business associates exemption was used by 302 issuers that raised gross proceeds of approximately $63 million.

• The offering memorandum exemption was used by 103 issuers that raised gross proceeds of approximately $68 million.

• The existing security holder exemption was used by 24 issuers that raised gross proceeds of approximately $2 million.

Among the new prospectus exemptions, the family, friends and business associates exemption was relied on the most by issuers in Ontario's exempt market. In 2016, the family, friends and business associates exemption was the second most used exemption in Ontario by number of issuers after the accredited investor exemption. The existing security holder exemption, which was targeted at reporting issuers listed on specified Canadian exchanges, has seen a much lower adoption rate. Although there has been no reported use of the crowdfunding exemption as of December 2016, there has been "crowdfunding" in the broader sense given that a small number of issuers have used online funding portals to raise proceeds under the accredited investor or offering memorandum exemption. Moreover, a number of portals registered in the exempt market dealer or restricted dealer category have indicated they may facilitate issuers relying on the crowdfunding exemption in the future.

In 2016, the family, friends and business associates exemption and offering memorandum exemption together were relied on by 387 issuers or almost a quarter of all Canadian issuers that raised capital in the Ontario exempt market. However, the total amount raised under these new exemptions accounted for less than 1% of gross proceeds. In some instances, issuers relied on both the offering memorandum exemption and the family, friends and business associates exemption. For most issuers, these new exemptions supplemented considerably larger amounts raised under the accredited investor exemption. Prior to the adoption of these new exemptions in Ontario, we observed that a sizeable proportion of issuers that raised capital under the accredited investor exemption in Ontario had relied on the family, friends and business associates exemption or offering memorandum exemption in other Canadian jurisdictions where it was already available.

ISSUER CHARACTERISTICS

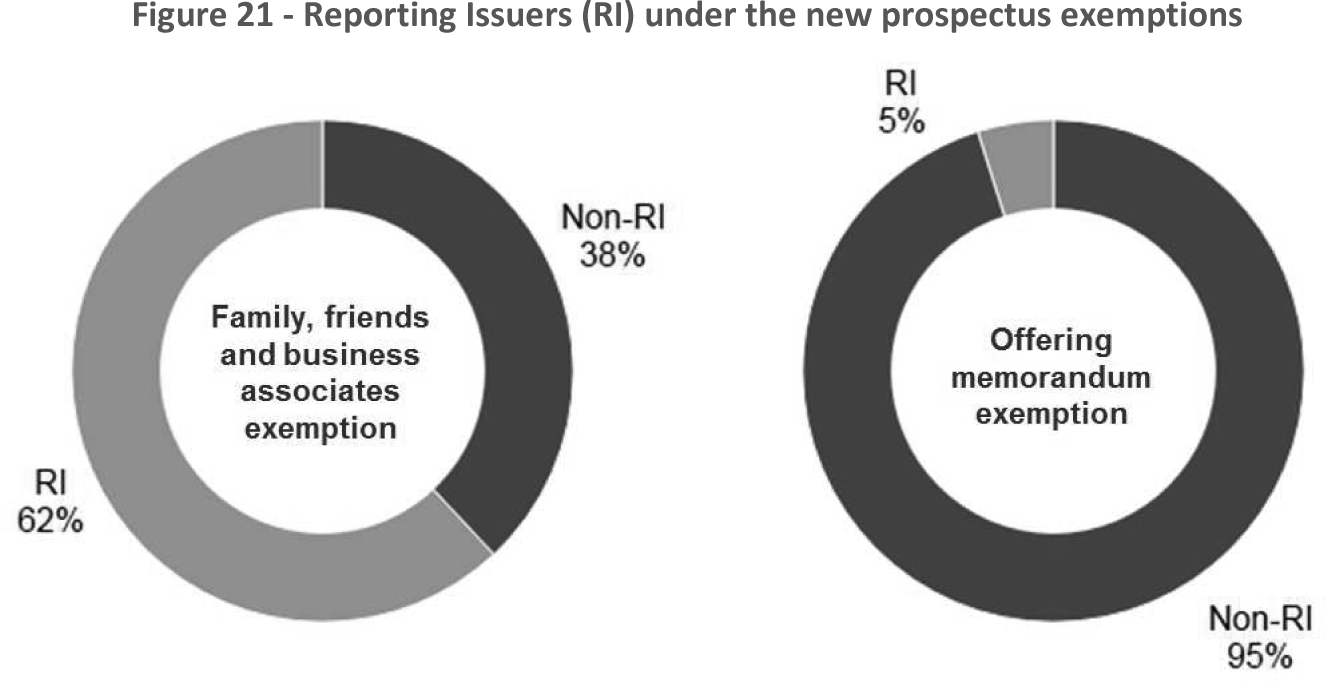

The family, friends and business associates and offering memorandum exemptions have been predominantly used by Canadian issuers (98%), although there are notable differences in the composition of the issuer groups that relied on these two exemptions. Almost two-thirds of the issuers that relied on the family, friends and business associates exemption were reporting issuers, whereas the majority (95%) of issuers that relied on the offering memorandum exemption were non-reporting issuers.

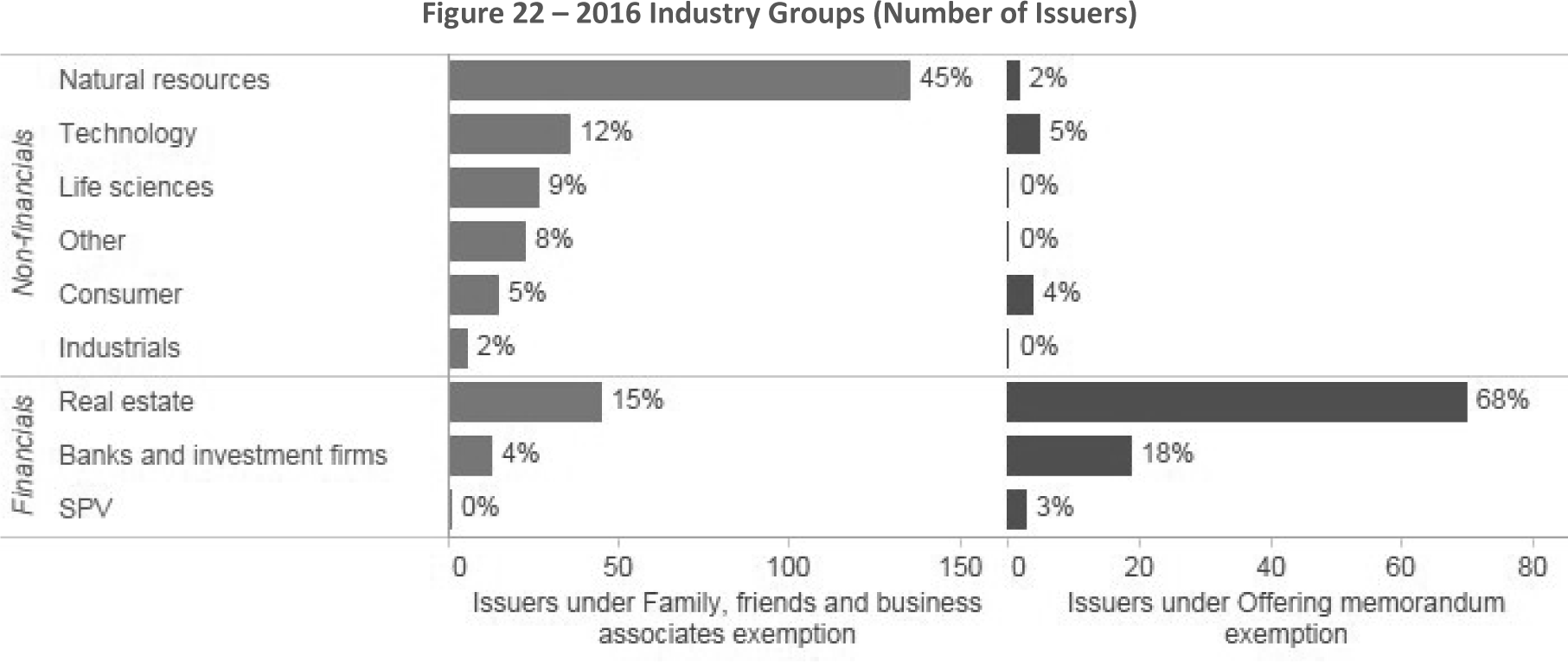

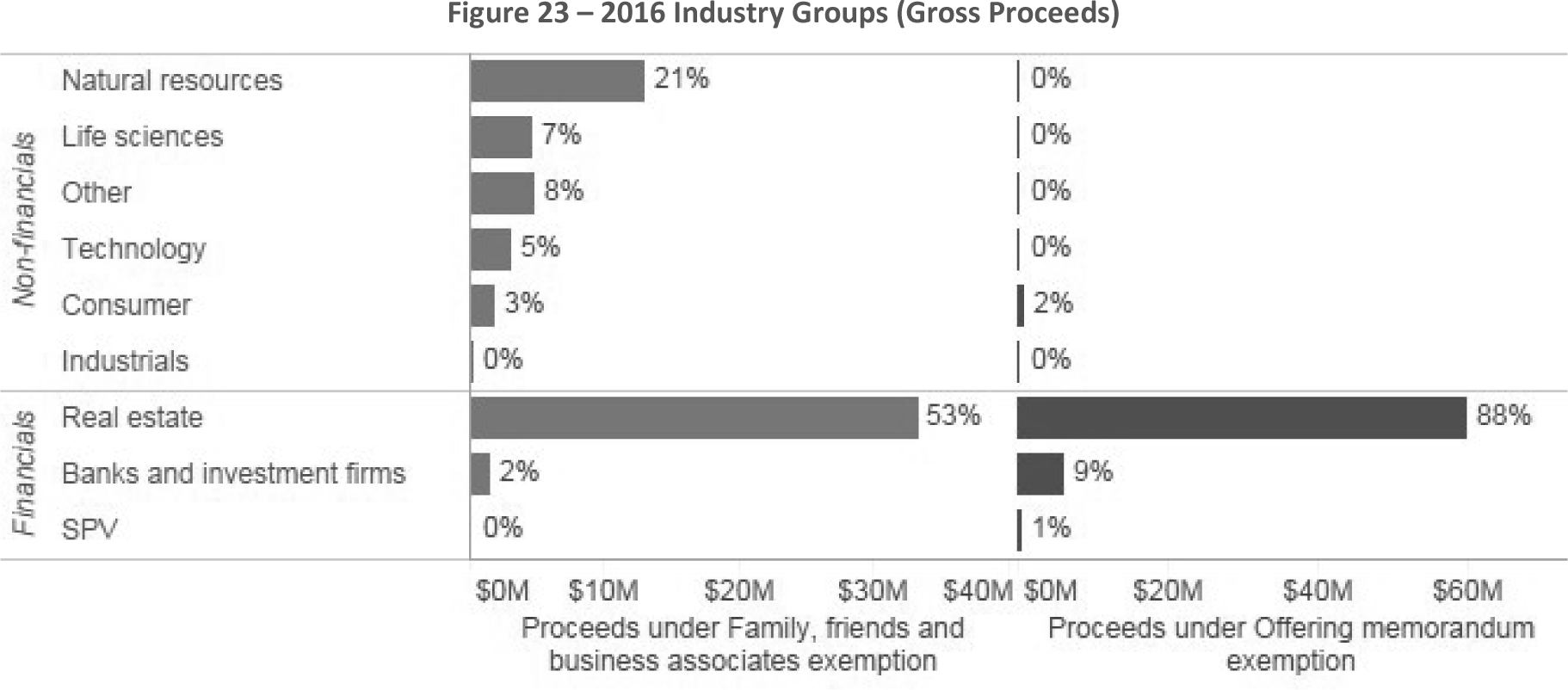

Junior mining issuers, most of which were also reporting issuers, represented approximately half of all issuers that used the family, friends and business associates exemption. Real estate issuers represented the second largest industry group that relied on the family, friends and business associates exemption and also accounted for the majority (53%) of the gross proceeds raised under that exemption. Real estate issuers have also been the predominant industry group among issuers that relied on the offering memorandum exemption in Ontario. They accounted for approximately 70% of the number of issuers and close to 90% of gross proceeds raised under the offering memorandum exemption in 2016.

In 2016, the family, friends and business associates exemption was relied on by three times as many issuers as the offering memorandum exemption, but most issuers relying on the family, friends and business associates exemption raised significantly smaller amounts of capital. Issuers relying on the offering memorandum exemption raised more capital since they incur higher transaction costs associated with preparing an offering memorandum document than is the case under the family, friends and business associates exemption.

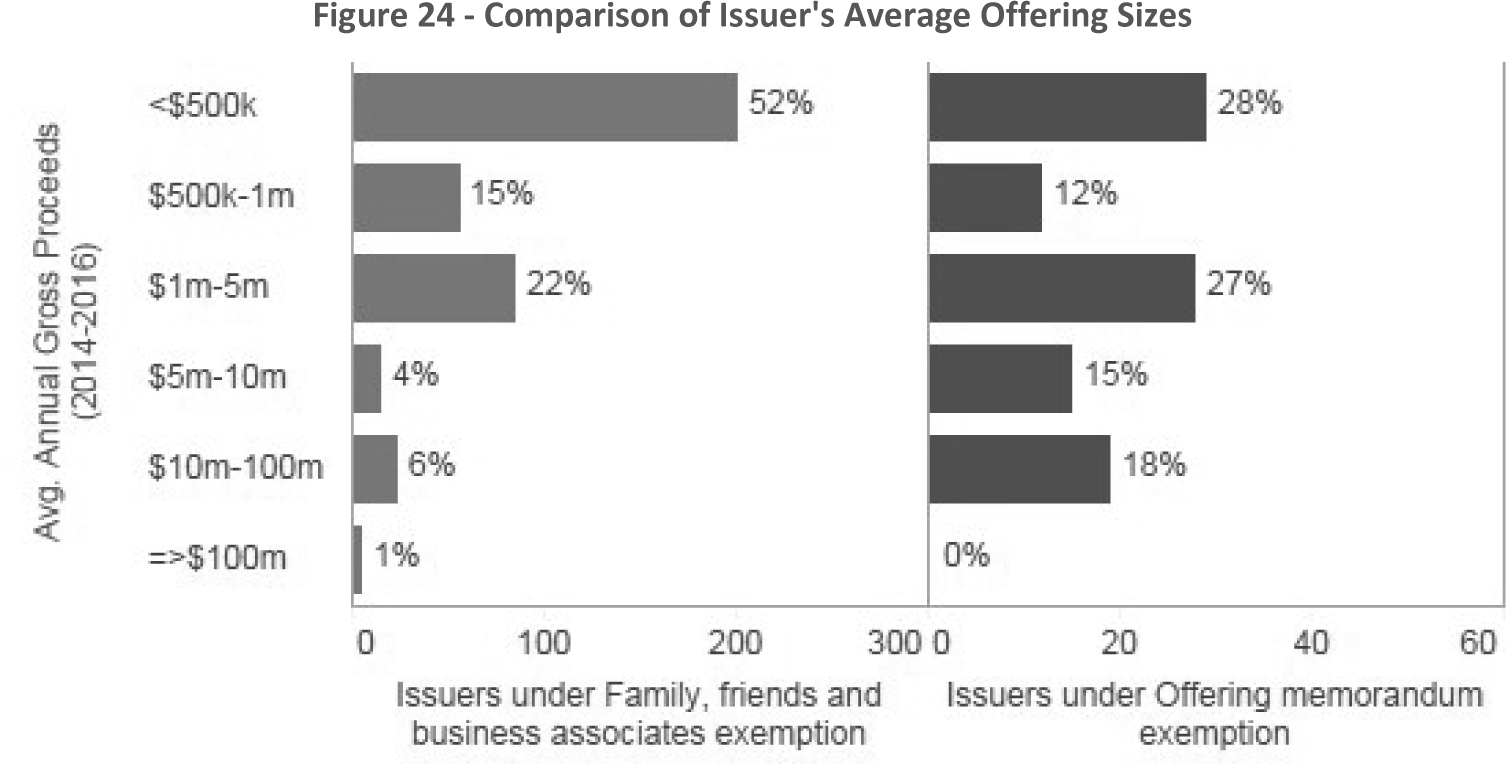

Since most issuers relying on the family, friends and business associates exemption or offering memorandum exemption also raised capital under other prospectus exemptions, particularly the accredited investor exemption, it is necessary to examine the issuers' total offering sizes across all exemptions when assessing the impact of these new exemptions on small issuers. Approximately 60% of issuers that relied on the offering memorandum exemption raised average gross proceeds of $1 million or higher annually. In contrast, close to 70% of issuers that relied on the family, friends and business associates exemption raised average gross proceeds of under $1 million annually. The family, friends and business associates exemption has mainly been used by smaller issuers, whereas the offering memorandum exemption has primarily been used by larger issuers to raise capital.

Lastly, we analyzed past exempt market activity by issuers that relied on the family, friends and business associates exemption or offering memorandum exemption to estimate whether these new exemptions have attracted new issuers to Ontario's exempt market. Our preliminary estimates indicate that roughly half of the issuers that relied on the new exemptions had not previously raised capital in Ontario since 2014. In particular, 40% of issuers that relied on the family, friends and business associates exemption and 58% of issuers that relied on the offering memorandum exemption accessed Ontario's exempt market for the first time since 2014.

6. QUESTIONS

Please refer your questions to any of the following OSC staff:

Kevin YangSenior Research Analyst, Strategy and Operations BranchOntario Securities Commission416-204-8983kyang@osc.gov.on.caJo-Anne MatearManager, Corporate Finance BranchOntario Securities Commission416-593-2323jmatear@osc.gov.on.caYan Kiu ChanLegal Counsel, Corporate Finance BranchOntario Securities Commission416-204-8971ychan@osc.gov.on.ca

{1} For more information about the exempt market, see OSC's "The exempt market" webpage at http://www.osc.gov.on.ca/en/exempt-market.htm or the OSC Investor Office's "The exempt market explained" webpage at <http://www.getsmarteraboutmoney.ca/>.

{2} For more information on the new prospectus exemptions and the OSC's exempt market reform initiative, see "Summary of Key Capital Raising Prospectus Exemptions in Ontario," January 28, 2016 at <:http://www.osc.gov.on.ca/documents/en/Securities-Category4/ni_20160128_45-106_key-capital-prospectus-exemptions.pdf>:.

{3} See OSC Notice 11-775 Notice of Statement of Priorities for Financial Year to End March 31, 2017 at <http://www.osc.gov.on.ca/en/SecuritiesLaw_sn_20160609_11-775_sop-end-2017.htm> and OSC Notice 11-777 Statement of Priorities -- Request for Comments Regarding Statement of Priorities for Financial Year to End March 31, 2018 at <http://www.osc.gov.on.ca/en/53722.htm>.

{4} The OSC's Compliance and Registrant Regulation Branch has recently completed an initial sweep of compliance reviews of exempt market dealers that have facilitated the distribution of securities in reliance on the new offering memorandum and family, friends and business associates exemptions. Please refer to OSC Staff Notice 33-748 2017 OSC Annual Summary Report for Dealers, Advisers and Investment Fund Managers (forthcoming) for more information about this sweep.

{5} Companies that rely on prospectus exemptions to distribute securities commonly rely on registered dealers to distribute the securities to investors. A company that seeks to distribute securities to investors without registered dealer involvement may itself be required to register as a dealer. For additional guidance on when companies and intermediaries need to be registered, see Companion Policy to National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations.

{6} However, in some cases, written offering materials may be considered an "offering memorandum" and subject to a requirement to deliver the written offering materials to the OSC. See Part 5 of OSC Rule 45-501.

{7} For more information on the Prior Report and current Report, see CSA Notice of Amendments to National Instrument 45-106 Prospectus Exemptions relating to Reports of Exempt Distribution, April 7, 2016 at <http://www.osc.gov.on.ca/en/SecuritiesLaw_csa_20160407_45-106_amd_prospectus-exemptions.htm>.

{8} See for example, Fleming, Sam. "Strengthening US economy bolsters case for rate rise." Financial Times. July 26, 2015. Web. May 2017; See also, "Better than it looks." The Economist. June 13, 2015. Web. May 2017.

{9} See for example, Platt, Eric and Joe Rennison. "Dash for debt ahead of US rate rise." Financial Times. November 8, 2015. Web. May 2017; See also Alloway, Tracy. "Last Year Was a Big One for the Corporate Bond Market." Bloomberg Markets. 8 January, 2016. Web. May 2017.

{10} Private equity funds raise large pools of capital to ultimately acquire or invest directly in operating businesses or real estate assets. Distribution data from private equity funds and similar issuers may lead to double counting of gross proceeds since the corporate beneficiary of the proceeds may have to file similar reports for any securities distributed under a prospectus exemption.

{11} See definition of "accredited investor" under Part 1 of NI 45-106.

{12} See for example, Platt, Eric. "Corporates lead surge to record $6.6tn debt issuance." Financial Times. 27 December 2016. Web. May 2017.

{13} See Myers, Steward C. "The capital structure puzzle," Journal of Finance, vol. 39, pp. 575-592, July 1984; See also Myers, Steward and Nicholas Majluf. "Corporate financing and investment decisions when firms have information markets do not have." Journal of Financial Economics, vol. 13, no. 2, July 1984.

{14} Issuers with credit ratings have easier access to debt capital markets and most issuers with credit ratings tend to be larger firms. See for example, Lemmon, Michael L. and Jaime F. Zender. "Debt Capacity and Tests of Capital Structure Theories." The Journal of Financial and Quantitative Analysis Vol. 45, No. 5, October 2010, pp. 1161-1187. See also, Frank, Murray Z. and Vidhan K. Goyal. "Trade-Off and Pecking Order Theories of Debt." December 8, 2007. Available at SSRN: https://ssrn.com/abstract=670543 .

{15} See for example, Nassr, Iota K and Gert Wehinger. "Non-bank debt financing for SMEs: The role of securitisation, private placements and bonds." OECD Journal Financial Market Trends, Vol 1, 2014; See also, Berger, Allen N. and Gregory F. Udell. "The Economics of Small Business Finance: The Roles of Private Equity and Debt Markets in the Financial Growth Cycle." Journal of Banking Finance, Vol. 22, 1998.

{17} See for example, "Annual Survey of Large Pension Funds and Public Pension Reserve Funds -- Report on pension funds' long -- term investments." OECD, 2015 at < http://www.oecd.org/daf/fin/private-pensions/2015-Large-Pension-Funds-Survey.pdf>. May 2017.

{18} OSC estimate based on data from Bank of Canada and obtained from Statistics Canada, CANSIM Table 176-0034 at <http://www5.statcan.gc.ca/cansim/a26>. Accessed on May 29, 2017. CANSIM Table 176-0034 covers all public issues as well as most private placements of Canadian corporations with an original term to maturity of more than one year. For more information see CANSIM Table 176-0034 footnotes.

{19} See Part 6 of NI 45-106 for more information on which capital raising prospectus exemptions trigger a filing requirement.

{20} See sections 73 and 73.1 of the Act for a similar exemption to the specified debt exemption at section 2.34 of NI 45-106.

{21} The majority (82%) of capital raised by Canadian issuers originates from the debt market which is heavily concentrated in bank and non-bank financial issuers. See also, "The Canadian Fixed Income Market -- 2014." OSC, 2015 at <http://www.osc.gov.on.ca/documents/en/Securities-Category2/20150423-fixed-income-report-2014.pdf>.

{22} For example, issuers with less than 50 investors (excluding current and former employees) can rely on the private issuer exemption under subsection 73.4(2) of the Act in Ontario, which does not require reporting to the OSC. Additionally, many small businesses may rely on other funding sources such as loans, grants and donations.

{23} See Industry Canada, Canadian Industry Statistics Glossary: Employment size category at <https://www.ic.gc.ca/eic/site/cis-sic.nsf/eng/h_00005.html#employment_size_category>. Accessed May 2017.

{24} Effective June 30, 2016, all Reports require issuers to provide number of employees and approximate size of assets which will be used to update these estimates in the future.

{25} More specifically, small issuers were identified as those that raised average gross proceeds of under $1 million annually from 2014 to 2016.

{26} The count of issuers by prospectus exemptions is not mutually exclusive since some issuers may have relied on more than one of the new prospectus exemptions to raise capital over the same period.