Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

OSC Notice and Request for Comment - Proposed OSC Rule 72-503 - Distributions Outside of Canada and CP 72-503CP to OSC Rule 72-503 Distributions Outside of Canada

OSC Notice and Request for Comment - Proposed OSC Rule 72-503 - Distributions Outside of Canada and CP 72-503CP to OSC Rule 72-503 Distributions Outside of Canada

NOTICE AND REQUEST FOR COMMENT

PROPOSED OSC RULE 72-503 DISTRIBUTIONS OUTSIDE OF CANADA AND

COMPANION POLICY 72-503CP TO OSC RULE 72-503 DISTRIBUTIONS OUTSIDE OF CANADA

June 30, 2016

Introduction

The jurisdictional scope of securities legislation in respect of a distribution of securities is not expressly addressed in the Securities Act (Ontario) (the Act) or the regulations.

In 1983, the Ontario Securities Commission (the Commission) published a note entitled "Interpretation Note 1 Distributions of Securities Outside Ontario"{1} (the Interpretation Note) in which the Commission acknowledged that an overly broad interpretation of the application of Ontario prospectus requirements could

"... seriously interfere with the capital formation process for issuers effecting financings outside Ontario where it is manifest that there is no intention that the securities distributed abroad will find their way into Ontario and where no question arises of bringing the Ontario capital markets into disrepute."

The Interpretation Note provided guidance that, where an issuer and intermediaries take "reasonable precautions" to ensure that securities distributed out of Ontario "come to rest" with investors outside of Ontario, and there are no other circumstances that would call into question the integrity of Ontario capital markets, the Commission would take the view that a prospectus was not required under the Act, nor was an exemption from the prospectus requirements necessary.

Over time market participants and Commission staff have found the approach described in the Interpretation Note difficult to administer because of its uncertainty:

The Interpretation Note did not seek to establish bright line tests to determine when a distribution outside of Ontario also constitutes a distribution in Ontario but rather sought to provide guidance to assist issuers and selling securityholders in structuring transactions. The Interpretation Note is not securities legislation and does not grant exemptions from the prospectus and registration requirements. The principal drawback of the Interpretation is that both market participants and Commission staff have found it difficult to administer because of its uncertainty.{2}

In particular, staff regularly encounter the various challenges that issuers and intermediaries face in determining whether sufficient steps have been taken to reasonably conclude that securities have "come to rest" outside of Canada and will not "flow back" into Canada.

Moreover, the Interpretation Note's approach to the application of Ontario prospectus requirements is substantially narrower than the approach taken to determining the parameters of a regulator's jurisdiction in recent case law. In the context of enforcement cases, the Commission and Courts have sometimes concluded that the securities laws of a jurisdiction will apply to activities outside of the jurisdiction provided there is a "real and substantial connection" (or "sufficient connecting factors") to the jurisdiction. These cases also often involve serious misconduct that may affect the reputation of the jurisdiction's capital markets.

The Commission approach to distributions outside of the jurisdiction has evolved over time, as has case law on provincial jurisdiction over activities outside the province, such that the Interpretation Note is out of date and no longer accurately represents Commission staff practice. The purpose of the Commission's proposals and the exemptions provided is to remove uncertainty regarding the extent of the application of the prospectus and registration requirements in certain cross border transactions, irrespective of the breadth of the Commission's jurisdiction based on case law.

The Commission is proposing the withdrawal of the Interpretation Note and is publishing for comment the following as its replacement:

• Proposed Ontario Securities Commission Rule 72-503 Distributions Outside of Canada and (the Proposed Rule)

• Proposed Form 72-503F Report of Distributions Outside of Canada (the Proposed Form)

• Companion Policy 72-503CP to OSC Rule 72-503 Distributions Outside of Canada (the Proposed Companion Policy).

In developing these proposed instruments, the Commission had the benefit of feedback from members of the Commission's Securities Advisory Committee and input from numerous Ontario market participants as well as public feedback on the draft initial regulations published on August 25, 2015 by governments participating in the Cooperative Capital Markets Regulatory System initiative. These draft initial regulations included a unified approach to distributions outside of Cooperative Capital Markets Regulatory System jurisdictions under draft Regulation 71-501 International Issuers and Securities Transactions with Persons Outside the CMR Jurisdictions and draft Policy 71-601 Distribution of Securities to Persons Outside of CMR Jurisdictions. These draft instruments represented a broader approach to the application of the prospectus requirement than is Commission staff's practice today. The Commentary to the draft instruments included specific questions that were designed to solicit feedback on the impact of the proposed approach to cross-border transactions in Ontario.

In response to this feedback and input, and based on staff's historical experience with cross-border transactions, the Commission is of the view that the proposed new distributions out regime is more reflective of Commission staff's current practice and strikes an appropriate balance between investor protections and facilitating cross-border offerings by avoiding the duplicative application of Ontario requirements where offering are subject to foreign securities laws.

Substance and Purpose

The substance and purpose of the Proposed Rule, the Proposed Form, and the Proposed Companion Policy is to provide certainty to participants in cross-border transactions by providing explicit exemptions that respond to the challenges that issuers and intermediaries face in determining whether a prospectus must be filed or an exemption from the prospectus requirement must be relied on, and the effect of related dealer registration requirements, in connection with a distribution of securities to investors outside of Canada. The provision of exemptions in the Proposed Rule is not, by itself, determinative of whether Ontario securities law would otherwise apply to a distribution outside of Canada or to activities related to the distribution.

Generally, the Proposed Rule provides exemptions from the prospectus requirement in respect of a distribution of securities to a person or company outside of Canada in the following circumstances:

• if the distribution is under a public offering document in the United States of America or a designated foreign jurisdiction

• if a concurrent distribution is qualified under a final prospectus in Ontario

• if the issuer is and has been a reporting issuer in a jurisdiction of Canada for the four months immediately preceding the distribution, and

• all other distributions, but subject to restrictions on resale to a person or company in a jurisdiction of Canada.

The Proposed Rule also provides an exemption from the dealer and underwriter registration requirement in respect of a distribution of securities to a person or company outside of Canada on the following conditions:

• the head office or principal place of business of the person or company is in the United States of America, a designated foreign jurisdiction or Canada

• in the case of a distribution to a purchaser in the United States of America, the person or company is appropriately registered with the SEC and FINRA and complies with all applicable regulatory requirements

• in the case of a distribution to a purchaser located in a designated foreign jurisdiction, the person or company is registered in a category similar to dealer in that jurisdiction and complies with all applicable regulatory requirements

• subject to a limited exception, the person or company does not carry on business as a dealer or underwriter from an office or place of business in Ontario

• other than the issuer or selling security holder, the person or company does not trade securities to, with or on behalf of anyone in Ontario, and

• the person or company relying on the exemption is not registered as a dealer in any jurisdiction of Canada.

Issuers will be required to file the Proposed Form electronically in Ontario, pursuant to OSC Rule 11-501 Electronic Delivery of Documents to the Ontario Securities Commission. Accordingly, the Proposed Form will be an e-form in Ontario, available on the Commission's Electronic Filing Portal. In developing the e-form, we will be incorporating the use of drop-down menus and other similar features wherever appropriate in order to make the e-form more "user-friendly" and easier to complete.

Authority for the Rule

The following provisions of the Act provide the Commission with authority to adopt the Proposed Rule.

Paragraph 143(1)8 authorizes the Commission to make rules prescribing any matter referred to in Part XII (Exemptions from Registration Requirements) as required by the regulations or prescribed by or in the regulations, other than the matters referred to in subsection 35.1(2).

Paragraph 143(1)20 authorizes the Commission to make rules prescribing any matter referred to in Part XVII (Exemptions from Prospectus Requirements) as required by the regulations or prescribed by or in the regulations, other than the matters referred to in subsection 73.1(3).

Paragraph 143(1)48 authorizes the Commission to specify the conditions under which any particular type of trade that would not otherwise be a distribution shall be a distribution.

Alternatives Considered

The Commission considered the options of maintaining the status quo under the Interpretation Note or updating the guidance in the Interpretation Note. In light of the feedback received on the Cooperative Capital Markets Regulatory System initiative, together with the ongoing issues faced by stakeholders in their attempts to apply the guidance in the Interpretation Note, the Commission has determined that an updated "distributions out" regime is required to improve the efficiency of Ontario participants' cross-border capital raising activities.

Unpublished Materials

In proposing the Proposed Rule and the Proposed Companion Policy, the Commission has not relied on any significant unpublished study, report, decision or other written materials.

Anticipated Costs and Benefits

The principal benefit of the Proposed Rule and the Proposed Companion Policy will be to provide more regulatory certainty to Ontario market participants. The Commission anticipates that this regulatory certainty will reduce overall costs for Ontario issuers seeking to raise capital outside of Ontario. The costs associated with the Proposed Rule and the Proposed Companion Policy will be

• the costs of analyzing the new exemptions and guidance provided to determine whether or not an Ontario prospectus or reliance on another prospectus exemption is required,

• the costs of complying with Ontario prospectus requirements in any circumstances that may have been previously covered by the Interpretation Note but are not covered by the Proposed Rule or Proposed Companion Policy, and

• the costs of preparing and filing the Proposed Form for outbound private placements.

In the view of the Commission, the benefits of the Proposed Rule, including the Proposed Form, and the Proposed Companion Policy outweigh the costs.

Request for Comments

The Commission welcomes your comments on the Proposed Rule (Annex A to this Notice), including the Proposed Form, and the Proposed Companion Policy (Annex B to this Notice).

How to Provide Your Comments

You must provide your comments in writing by September 28, 2016. If you are not sending your comments by email, you should also send an electronic file containing the submissions (in Windows format, Microsoft Word).

Please send your comments to the following address:

The SecretaryOntario Securities Commission20 Queen Street West22nd FloorToronto, Ontario M5H 3S8Fax: 416-593-2318Email: [email protected]

The Commission will publish written comments received unless the Commission approves a commenter's request for confidentiality or the commenter withdraws its comment before the comment's publication.

Questions

Please refer your questions to:

Victoria CarrierSenior Legal CounselGeneral Counsel's Office416-593-8329Michael TangActing ManagerCorporate Finance416-593-2330Elizabeth ToppSenior Legal CounselCompliance and Registrant Regulation416-593-2377Doug WelshSenior Legal CounselInvestment Funds and Structured Products416-593-8068Andre MonizSenior Investigation CounselEnforcement416-593-2383

{1} Interpretation Note 1 was published in connection with the Notice of Repeal of OSC Policy 1.5 Distribution of Securities Outside of Ontario, (March 25, 1983) 6 OSCB 226.

{2} See Notice and Request for Comment in respect of proposed Multilateral Instrument 72-101 Distributions Outside of the Local Jurisdiction (September 8, 2000) (2000) 23 OSCB 6260. In March 2002, the CSA published CSA Staff Notice 72-301 in relation to proposed MI 72-101 that indicated that the initiative was now being considered under the CSA Uniform Securities Legislation Project (the USL Project). In Ontario and certain other jurisdictions, the USL Project has been superseded by the Cooperative Capital Markets Regulatory System initiative.

ANNEX A PROPOSED ONTARIO SECURITIES COMMISSION RULE 72-503 DISTRIBUTIONS OUTSIDE OF CANADA

PART 1 DEFINITIONS

1.1 Definitions -- in this Rule

"1933 Act" means the Securities Act of 1933 of the United States of America, as amended from time to time;

"distribution date" has the same meaning as in National Instrument 45-102 Resale of Securities;

"designated foreign jurisdiction" has the same meaning as in National Instrument 71-102 Continuous Disclosure and Other Exemptions Relating to Foreign Issuers;

"FINRA" means the Financial Industry Regulatory Authority, a self-regulatory organization in the United States of America; and

"SEC" means the Securities and Exchange Commission of the United States of America.

PART 2 EXEMPTIONS FROM THE PROSPECTUS REQUIREMENT

2.1 Distribution Under Public Offering Document in Foreign Jurisdictions -- The prospectus requirement does not apply to a distribution of securities to a person or company outside of Canada if prior to the issuance or resale of the securities,

(a) the issuer has filed a registration statement in accordance with the 1933 Act registering the securities in connection with the distribution, and that registration statement has become effective; or

(b) the issuer has filed a document similar to a final prospectus for which a receipt or similar acknowledgement of approval has been obtained in accordance with the securities laws of a designated foreign jurisdiction registering the securities in connection with the distribution or qualifying the securities for distribution.

2.2 Concurrent Distribution under Final Prospectus in Ontario -- The prospectus requirement does not apply to a distribution of securities to a person or company outside of Canada if,

(a) in connection with the distribution, the issuer of those securities or the selling securityholder has complied with the securities law requirements of the jurisdiction outside of Canada; and

(b) prior to the issuance or resale of the securities, the issuer of those securities has filed with the Commission and a receipt has been issued for a final prospectus qualifying the concurrent distribution of such securities in Ontario in accordance with Ontario securities law.

2.3 Distributions by Reporting Issuers -- The prospectus requirement does not apply to a distribution of securities to a person or company outside of Canada if,

(a) in connection with the distribution, the issuer of those securities or the selling securityholder has complied with the securities law requirements of the jurisdiction outside of Canada; and

(b) the issuer of the securities is and has been a reporting issuer in a jurisdiction of Canada for the four months immediately preceding such distribution.

2.4 Other Distributions

(1) The prospectus requirement does not apply to a distribution of securities to a person or company outside of Canada if, in connection with the distribution, the issuer of those securities or the selling securityholder has complied with the securities law requirements of the jurisdiction outside of Canada.

(2) The first trade of securities distributed under the exemption in subsection (1) is a distribution unless

(a) the trade is to a person or company outside of Canada; or

(b) both of the following are satisfied:

(i) The issuer of the securities is and has been a reporting issuer in a jurisdiction of Canada for the four months immediately preceding the trade.

(ii) At least four months have elapsed from the distribution date.

PART 3 EXEMPTION FROM THE DEALER AND UNDERWRITER REGISTRATION REQUIREMENTS

3.1 Exemption from the Dealer and Underwriter Registration Requirements -- The dealer registration requirement and the underwriter registration requirement do not apply to a person or company in connection with a distribution of securities to a person or company outside of Canada that is qualified by a prospectus filed in a jurisdiction of Canada or that is exempt from the prospectus requirement under Part 2 of this Rule if all of the following apply

(a) The head office or principal place of business of the person or company is in the United States of America, a designated foreign jurisdiction or Canada;

(b) In the case of a distribution to a purchaser located in the United States of America, the person or company is registered as a broker-dealer with the SEC, is a member in good standing of FINRA and complies with all applicable conduct and other regulatory requirements of U.S. federal and state securities law and FINRA rules in connection with the distribution;

(c) In the case of a distribution to a purchaser located in a designated foreign jurisdiction, the person or company is registered under the securities legislation of the designated foreign jurisdiction in a category of registration that permits it to carry on the activities in that jurisdiction that registration as a dealer would permit it to carry on in Ontario, and complies with all applicable dealer registration requirements and other broker-dealer regulatory requirements of the designated foreign jurisdiction in connection with the distribution;

(d) The person or company does not carry on business as a dealer or underwriter from an office or place of business in Ontario except in accordance with Ontario Securities Commission Rule 32-505 Conditional Exemption from Registration for United States Broker-Dealers and Advisers Servicing U.S. Clients from Ontario or this Rule;

(e) Other than an issuer or selling security holder involved in a distribution that is exempt from Ontario prospectus requirements under this Rule, the person or company does not trade securities to, with, or on behalf of, a person or company in Ontario, except pursuant to an exemption from registration other than the exemption provided by this section 3.1; and

(f) The person or company is not registered in any jurisdiction of Canada in the category of dealer.

PART 4 REPORT OF DISTRIBUTION OUTSIDE CANADA

4.1 Report of Distribution outside Canada -- An issuer that relies on the exemption in section 2.2, 2.3 or 2.4 must, on or before the tenth day after the distribution date, electronically file a report of trade with respect to that exempt distribution. The electronic filing must be prepared in accordance with the instructions and must include the required information set forth in Form 72-503F Report of Distributions Outside of Canada.

PART 5 EXEMPTION

5.1 Exemption -- Only the Director may grant an exemption and only an exemption from Part 4 may be granted, in whole or in part, subject to such conditions or restrictions as may be imposed in the exemption.

PART 6 EFFECTIVE DATE

6.1 Effective Date -- This Rule comes into force on •.

FORM 72-503F REPORT OF DISTRIBUTIONS OUTSIDE OF CANADA

Instructions:

1. An issuer that is required to file a report on Form 72-503F Report of Distributions Outside of Canada must file the report through the online e-form available at http://www.osc.gov.on.ca.

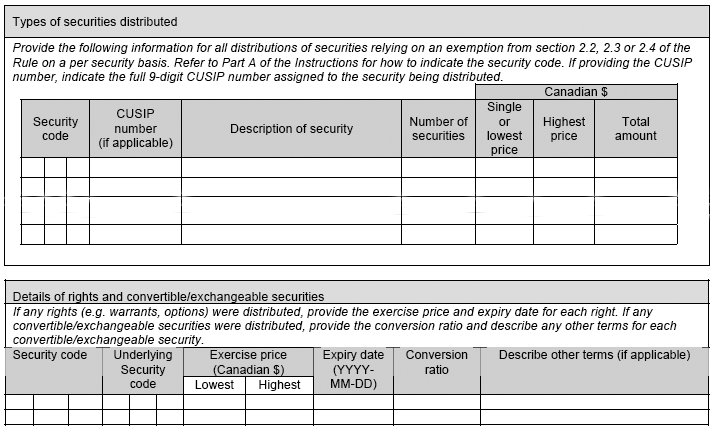

2. Security codes: Wherever this form requires disclosure of the type of security, use the following security codes:

Security code

Security type

BND

Bonds

CER

Certificates (including pass-through certificates, trust certificates)

CMS

Common shares

CVD

Convertible debentures

CVN

Convertible notes

CVP

Convertible preferred shares

DEB

Debentures

FTS

Flow-through shares

FTU

Flow-through units

LPU

Limited partnership units

NOT

Notes (include all types of notes except convertible notes)

OPT

Options

PRS

Preferred shares

RTS

Rights

UBS

Units of bundled securities (such as a unit consisting of a common share and a warrant)

UNT

Units (exclude units of bundled securities, include trust units and mutual fund units)

WNT

Warrants

OTH

Other securities not included above (if selected, provide details of security type in Item 2

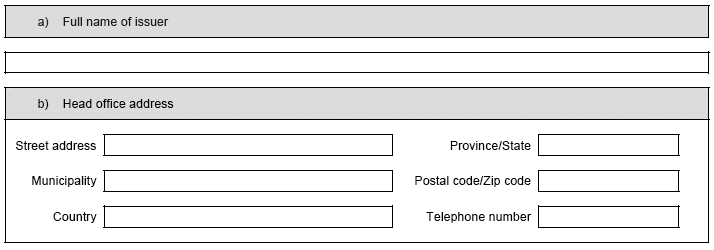

1. Full name, address and telephone number of the Issuer.

2. Type of security, the aggregate number or amount distributed and the aggregate purchase price.

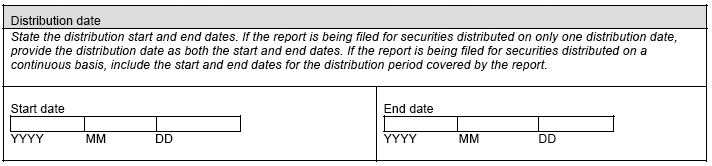

3. Date of distribution(s).

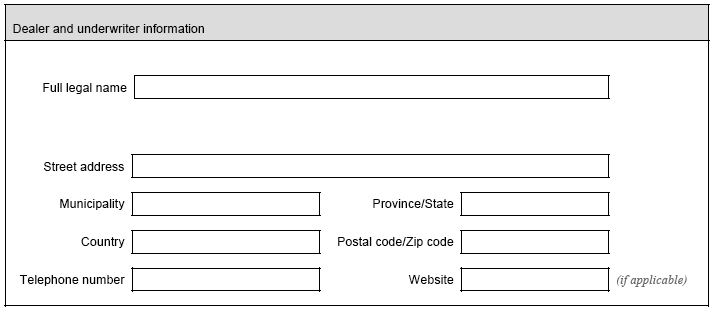

4. State the name and address of any person acting as dealer or underwriter (including an underwriter that is acting as agent) in connection with the distribution(s) of the securities.

5. Certification

Provide the following certification and business contact information of an officer or director of the issuer. If the issuer is not a company, an individual who performs functions similar to that of a director or officer may certify the report. For example, if the issuer is a trust, the report may be certified by the issuer's trustee. If the issuer is an investment fund, a director or officer of the investment fund manager (or, if the investment fund manager is not a company, an individual who performs similar functions) may certify the report if the director or officer has been authorized to do so by the investment fund.

The certification may not be delegated to an agent or other individual preparing the report on behalf of the issuer.

The signature on the report must be in typed form rather than handwritten form. The report may include an electronic signature provided the name of the signatory is also in typed form.

Certificate of Issuer

The undersigned hereby certifies that the statements made in this report are true.

DATED: _________________, 20__

______________________________

[Title]

ANNEX B PROPOSED COMPANION POLICY 72-503CP TO OSC RULE 72-503 DISTRIBUTIONS OUTSIDE OF CANADA

PART 1 APPLICATION AND PURPOSE

This Policy sets out how the Ontario Securities Commission (the Commission or the OSC) interprets and applies section 53 of the Securities Act (Ontario) (the Act), the provisions of OSC Rule 72-503 Distributions of Securities Outside of Canada (the Rule) and section 25 of the Act in limited circumstances.

Statement of Principle

A distribution of securities by an issuer to an investor outside of Ontario may be subject to the Act depending on the connecting factors with Ontario. The Commission takes the view that an investor outside of Canada will ordinarily expect to rely on the prospectus, registration statement or similar protections of the securities laws of the foreign jurisdiction in which the investor is located. The Commission recognizes that compliance with the prospectus requirement or conditions of a prospectus exemption under Ontario securities law may be unnecessarily duplicative of these protections and will generally not be necessary to fulfill the purposes of the Act.

Accordingly, the Commission does not interpret the prospectus requirement as applying to a distribution of securities outside of Canada that is made in compliance with the securities laws of the foreign jurisdiction in which the investor is located, provided that the issuer, underwriters and other participants in the offering take reasonable steps to ensure that the securities come to rest outside of Canada and are not redistributed back into Canada. The issuer, underwriters and other participants in the offering would be expected to implement reasonable precautions and restrictions designed to ensure that the entire distribution process results in the securities being held by or for the benefit of foreign investors, as opposed to intermediaries in the distribution chain holding securities for resale to investors in Canada.

The Commission acknowledges that the connecting factors test at common law for determining the Commission's jurisdiction and the coming to rest notion for determining whether an Ontario prospectus is required may not provide sufficient certainty to market participants. The purpose of the Rule is to provide certainty to cross-border transactions by providing explicit exemptions that respond to the challenges that issuers and intermediaries face in determining whether a prospectus must be filed or an exemption from the prospectus requirement must be relied on in connection with a distribution of securities to investors outside of Canada. Therefore, the provision of exemptions in the Rule is not, by itself, determinative of whether Ontario securities law would otherwise apply to a distribution outside of Canada or to activities related to the distribution.

The Integrity of the Ontario Capital Markets and the Jurisdiction of the Commission

Neither the Rule nor this Policy impacts the jurisdiction of the Commission. Where the Commission becomes aware of conduct that may bring the reputation of Ontario's capital markets into disrepute or otherwise impair its mandate, the Commission may assert its jurisdiction and exercise its powers to take appropriate action against issuers, underwriters and other persons, including in connection with distributions of securities to an investor outside of Canada. Regardless of whether there is a distribution in Ontario in breach of section 53 of the Act, the Commission may exercise its discretionary authority to cease trade securities, make orders to prevent conduct contrary to the public interest, and make regulations to foster fair and efficient capital markets and confidence in capital markets.

PART 2 EXEMPTIONS FROM THE PROSPECTUS REQUIREMENT

Generally

The prospectus exemptions under Part 2 of the Rule are intended to facilitate cross-border offerings by removing the potentially duplicative application of Ontario prospectus requirements where offerings to an investor outside of Canada are made in compliance with the securities laws of the foreign jurisdiction.

Concurrent Distribution under Final Prospectus in Ontario

An issuer or selling securityholder distributing securities to an investor outside of Canada may concurrently distribute securities to purchasers in Ontario provided that the distribution of securities to an investor in Ontario is qualified by a prospectus filed under the Act, or is conducted in reliance on an exemption from the prospectus requirement. The condition under paragraph 2.2(b) of the Rule therefore requires the filing of a prospectus in Ontario in connection with a concurrent distribution in Ontario. The prospectus exemption under section 2.2 of the Rule may be relied on for purposes of the distribution to an investor outside of Canada only.

If an issuer or selling securityholder files a prospectus to qualify a concurrent distribution to a person or company in Ontario, the issuer may choose to file a prospectus in Ontario to qualify the distribution of securities to an investor outside of Canada. Any prospectus filed in such circumstances should therefore clearly state whether or not it also qualifies the distribution of securities to an investor outside of Canada, recognizing that purchasers of Ontario prospectus-qualified securities may be entitled to certain rights and investor protections under the Act even if the investor is outside of Canada.

If there is no concurrent distribution in Ontario but the issuer files an Ontario prospectus in connection with the distribution of securities to an investor outside of Canada, the securities being distributed outside of Canada will be qualified by the Ontario prospectus. In this case, the issuer or selling securityholder would not be relying on the exemption from the prospectus requirement in section 2.2 of the Rule because a prospectus in Ontario is qualifying the distribution.

Resale

Nothing in the Rule prohibits or restricts the resale of the securities distributed under an exemption from the prospectus requirement in section 2.1, 2.2, or 2.3 of the Rule. Nevertheless, the Commission expects the issuer, underwriters and other participants in the offering will have taken reasonable steps to ensure that the securities come to rest outside of Canada and are not redistributed back into Canada in a manner that constitutes an indirect distribution in Ontario.

Securities distributed under an exemption from the prospectus requirement in section 2.4 of the Rule may be subject to resale restrictions.

The Multijurisdictional Disclosure System

Nothing in the Rule is intended to affect the guidance in section 4.3 of Companion Policy 71-101CP To National Instrument 71-101 The Multijurisdictional Disclosure System. An issuer relying on an exemption from the prospectus requirement in paragraph 2.1(a) of the Rule may file a Form F-10 in connection with a distribution solely in the United States of America under the multijurisdictional disclosure system adopted by the SEC, select the Ontario as review jurisdiction, file the registration statement filed with the SEC with the Commission contemporaneously with the filing of the registration statement with the SEC, obtain notification of clearance from the Commission and advise the SEC of the issuance of the notification of clearance.

PART 3 EXEMPTIONS FROM THE REGISTRATION REQUIREMENT

Section 25 of the Act and National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103) set out the general requirements for registration as well as certain exemptions from these requirements. The Companion Policy to NI 31-103 provides guidance to issuers and intermediaries on how to apply the triggers for registration as well as interpret the exemptions from these requirements.

Part 3 of the Rule provides an exemption from the dealer and underwriter registration requirements in Ontario securities law for certain foreign dealers (including dealers acting as underwriters) with respect to distributions to investors outside of Canada that are made under a prospectus filed in Ontario or made in reliance on the exemptions in Part 2 of the Rule. The exemption may also be relied on by an entity that has its head office in Canada, is not registered as a dealer in Canada but is registered as a dealer in the United States of America or a designated foreign jurisdiction. The exemption includes entities that have their head office in Canada to address the situation of certain foreign broker-dealer affiliates of Canadian firms that have no foreign offices and share space and personnel with the affiliated Canadian dealer.

The Commission reminds market participants that registration in Ontario is generally required (unless an exemption is otherwise available) where registerable activities are provided to investors in Ontario or where registerable activities are otherwise conducted within Ontario, regardless of the location of the investors.

The Commission recognizes that, in the case of a distribution of securities by an Ontario issuer to purchasers outside of Ontario, there may be a question as to whether foreign dealers or underwriters that participate in the distribution are subject to the dealer and underwriter registration requirements of Ontario securities law. The Commission has introduced the exemption in Part 3 of the Rule to provide greater certainty to market participants and to help address the challenges that foreign dealers and underwriters may face in determining whether the dealer and underwriter registration requirement applies to their activities. The provision of these exemptions is not determinative of whether Ontario securities law would otherwise apply to the activities of the foreign dealer or underwriter related to the distribution. Foreign dealers and advisers may also wish to consider the registration exemptions in OSC Rule 32-505 Conditional Exemption from Registration for United States Broker-Dealers and Advisers Servicing U.S. Clients from Ontario.

PART 4 THE FORM

Issuers are required to file the information set forth in Form 72-503F Report of Distributions Outside of Canada (the Form) electronically through the Commission's Electronic Filing Portal. The electronic filing requirement applies to all issuers that are subject to the Form's disclosure requirements. Please see OSC Rule 11-501 Electronic Delivery of Documents to the Ontario Securities Commission for further information.