Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

Summary Report for Investment Fund and Structured Product Issuers - 2015

Summary Report for Investment Fund and Structured Product Issuers - 2015

2015 - Summary Report for Investment Fund and Structured Product Issuers

February 17, 2016

Table of Contents

Introduction

1. Key Policy Initiatives

1.1 Mutual Fund Fees

1.2 Point of Sale Project – Pre-Sale Delivery for Mutual Funds, Summary Disclosure for ETFs and Risk Classification Methodology

1.3 Accredited Investor Exemption for Investment Funds

1.4 Modernization of Investment Fund Product Regulation

2. Emerging Issues and Trends

2.1 Update on Structured Note Offerings

2.2 Past Performance Presentation in the Fund Facts

2.3 Investment Funds that Track an Index

3. Disclosure and Compliance Reviews

3.1 Continuous Disclosure Reviews

3.2 Compliance and Registrant Regulation Branch Reviews of Investment Fund Managers

4. Outreach, Consultation and Education

4.1 Investment Funds Product Advisory Committee (IFPAC)

4.2 The Investment Funds Practitioner

4.3 International Organization of Securities Commissions - Committee 5 - Investment Management (IOSCO C5)

5. Feedback and Contact Information

Introduction

Our annual Summary Report for Investment Fund and Structured Product Issuers provides an overview of the key activities and initiatives of the Ontario Securities Commission for 2015 that impact investment fund and structured product issuers and the fund industry, including:

- key policy initiatives,

- emerging issues and trends,

- continuous disclosure and compliance reviews, and

- recent developments in staff practices.

This report provides information about the status of some of the initiatives the OSC is undertaking to promote clear and concise disclosure in order to assist investors in making more informed investment decisions, as well as our work to examine the effect of mutual fund compensation models on advisor behaviour. It also highlights recent product and market developments, and our regulatory response to them, to assist the investment management industry in understanding and complying with regulatory requirements.

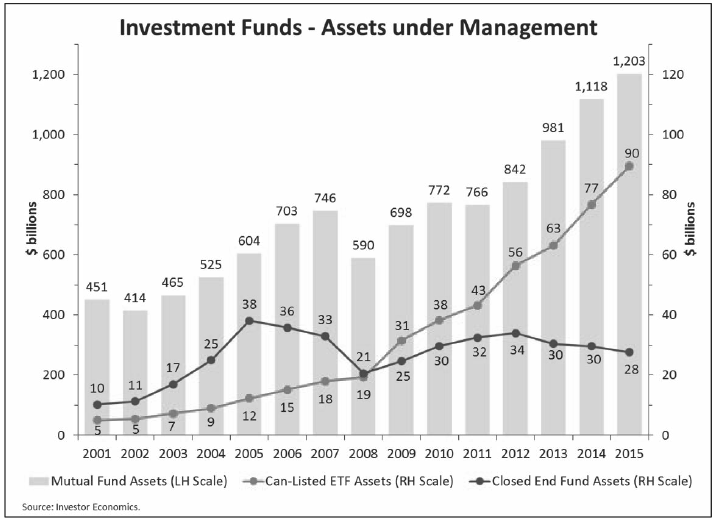

The OSC is responsible for overseeing approximately 3900 publicly-offered investment funds. Ontario-based publicly-offered investment funds hold approximately 80% of the over $1.3 trillion in publicly-offered investment fund assets in Canada.

We administer the regulatory framework for investment funds, including:

- reviewing and assessing product disclosure for all types of investment funds, including prospectuses and continuous disclosure filings,

- considering applications for discretionary relief from securities legislation and rules, and

- taking a leadership role in developing new rules and policies to adapt to changes in the investment fund industry.

We also monitor and participate in investment fund regulatory developments globally, primarily through our work with the International Organization of Securities Commissions (IOSCO). OSC staff participation on the IOSCO C5 Investment Management Committee informs our operational and policy work. In this report, we highlight some of the recent work by IOSCO C5 that we think are of interest to investment fund issuers.

The investment products we oversee include both conventional mutual funds and non-conventional investment funds, as well as structured notes. Non-conventional funds include non-redeemable investment funds such as closed-end funds, open-end mutual funds listed and posted for trading on a stock exchange (ETFs), commodity pools, scholarship plans, labour-sponsored or venture capital funds and flow-through limited partnerships. We discuss the different types of funds on our website at www.osc.ca: Types of investment funds.

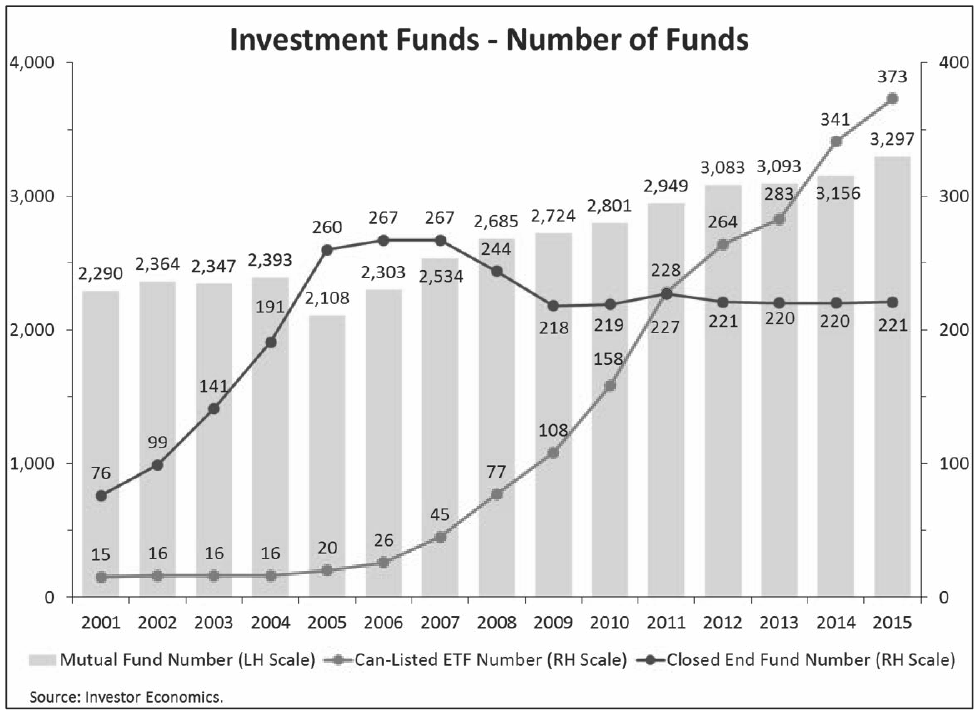

The ETF market continued to grow in 2015. As at the end of December 2015, there were 373 ETFs in Canada with assets of $90 billion. In comparison, as at December 2014, there were 341 ETFs with assets of $77 billion, representing an increase in assets of 17%. Over the same period, conventional fund assets increased by approximately $85 billion, or 8%. Total conventional mutual fund assets stood at approximately $1.2 trillion at the end of 2015. As at December 2015, closed-end fund assets totalled $27.6 billion, having declined by approximately 7% from December 2014.

As these and other investment and structured products increase in number, and as the use of ETFs by retail investors continues to grow, the OSC will continue to assess and respond to product developments and innovations with a view to promoting investor protection and improving the consistency of the regulatory treatment of different investment fund and structured products.

1. Key Policy Initiatives

The OSC has a leading role in several significant policy initiatives being undertaken with other securities regulators in Canada through the Canadian Securities Administrators (the CSA). This section reports on the status of key policy initiatives, including:

- mutual fund fees,

- pre-sale delivery for mutual funds, summary disclosure for ETFs and risk classification methodology,

- accredited investor exemption for investment funds, and

- modernization of investment fund product regulation.

1.1 Mutual Fund Fees

To advance a policy decision on mutual fund fees, and as part of a broader effort to make evidence-based policy, the CSA commissioned two pieces of independent third party research, which were completed and published in 2015. They consist of:

- a literature review entitled “Mutual Fund Fee Report” (Brondesbury Report) conducted by the Brondesbury Group and published on June 11, 2015. This report evaluates the extent to which the use of fee-based versus commission-based compensation changes the nature of advice and impacts investment outcomes over the long term, and

- an empirical study entitled “A Dissection of Mutual Fund Fees, Flows, and Performance” (Cumming Report) conducted by Professor Douglas J. Cumming and published on October 22, 2015. This report evaluates the extent to which sales and trailing commissions influence fund sales using data sourced directly from Canadian fund managers.

The Brondesbury Report concludes that while commission-based compensation is sufficiently problematic to justify the development of new compensation policies, based on the literature reviewed, there is insufficient evidence to support a conclusion that investors would achieve better long-term outcomes under a fee-based model. The Brondesbury Report cautions that while fee-based compensation is likely a better alternative, it is not a behaviourally-neutral form of compensation. Other forms of inducements that influence advice, such as bonuses or the potential for promotion at the dealer firm, and affiliation between a fund manager and a dealer firm, would likely persist under a fee-based model, which may lessen the benefits of moving to such a model. The Brondesbury Report also finds that investor behavioural biases are an important factor in sub-optimal returns on investment and that these biases are unlikely to be overcome as a result of changing compensation schemes alone, although it is possible they can be moderated.

The findings of the Cumming Report are based on an analysis of detailed data on mutual fund fees, flows and performance obtained under a data request the CSA sent in November 2014 to 113 fund managers of conventional mutual funds in Canada. Of those contacted, 43 fund managers managing approximately 67% of mutual fund assets and 51.5% of fund-of-fund assets in Canada voluntarily provided the data requested. The data sample collected comprised more than one million monthly observations on fees, flows and performance. The Cumming Report finds that mutual funds that perform better attract more sales, but this effect is less strong when fund managers: (i) pay trailing commissions to dealer firms – these commissions increase new flows regardless of the fund’s past performance, and (ii) distribute their mutual funds through affiliated dealers – in this case, the fund manager’s ownership of the fund shelf appears to be the primary driver of sales. The Cumming Report also finds that higher trailing commissions and high affiliated dealer flow negatively affect future outperformance.

The findings from the Brondesbury Report and the Cumming Report, together with the comments gathered from industry stakeholders and investor advocates throughout the CSA’s consultation process on mutual fund fees, will be key inputs to CSA staff deliberations on policy recommendations. The CSA expects to communicate its policy direction on mutual fund fees in the first half of 2016.

1.2 Point of Sale Project – Pre-Sale Delivery for Mutual Funds, Summary Disclosure for ETFs and Risk Classification Methodology

(i) Pre-sale delivery of fund facts document

Stage 3 of the Point of Sale (POS) Project was completed in December 2014 with the publication of rule amendments to require the pre-sale delivery of the fund facts document (Fund Facts) for mutual funds. Currently, dealers are required to deliver the Fund Facts within two days of buying a mutual fund. Effective May 30, 2016, dealers will be required to deliver the Fund Facts to a purchaser before accepting an instruction for the purchase of a mutual fund, with the prospectus continuing to be available to investors upon request.

(ii) Summary disclosure document for ETFs

On June 18, 2015, the CSA published proposed rule amendments that will require ETFs to produce and file a summary disclosure document called “ETF Facts”, and make it available on the ETF’s or the ETF manager’s website. The proposed rules also introduce a new delivery requirement that will require dealers to deliver an ETF Facts to investors within two days of a purchase, including secondary market purchases. Delivery of the ETF’s prospectus will not be required, but the prospectus will continue to be filed with regulators and made available at no cost to investors upon request.

The proposed ETF Facts is based on the Fund Facts, however, it contemplates information specific to the attributes of an ETF, including trading and pricing information. The introduction of the ETF Facts will help investors access key information about an ETF in language they can easily understand. Furthermore, the new delivery regime for ETF Facts will ensure that all ETF investors receive the same disclosure, regardless of whether they purchased ETF securities under a distribution. It will also create a more consistent disclosure framework between conventional mutual funds and ETFs, two comparable products sold to retail investors.

We received 20 comment letters during the 90 day comment period for the proposed rules that ended on September 16, 2015. Staff are currently considering the feedback received from the comment letters.

(iii) CSA risk classification methodology

We continued work on proposed rule amendments for a CSA risk classification methodology (the Proposed Methodology) for use in the Fund Facts and the ETF Facts. The Proposed Methodology will be used to determine the risk rating of a conventional mutual fund and an ETF on the risk scale prescribed in the Fund Facts and for the proposed ETF Facts, respectively.

Currently, fund managers determine the risk rating of a conventional mutual fund using a risk classification methodology selected at their discretion. The Proposed Methodology responds to stakeholder comments we received throughout the POS Project that a standardized risk classification methodology is necessary to ensure greater consistency and improved comparability in the risk ratings of mutual funds. The Proposed Methodology was informed by stakeholder feedback received in an earlier consultation published in CSA Notice 81-324 and Request for Comments Proposed CSA Mutual Fund Risk Classification Methodology for Use in Fund Facts on December 12, 2013. As part of the consultation, we asked stakeholders whether the Proposed Methodology should be used for other types of publicly-offered investment funds, such as ETFs, in documents similar to the Fund Facts. Based on the feedback received, staff determined that the Proposed Methodology should also be used to determine the risk ratings of ETFs in the proposed ETF Facts. A summary of the key themes of the comments received from the consultation was published in CSA Staff Notice 81-325 Status Report on Consultation under CSA Notice 81-324 and Request for Comment on Proposed CSA Mutual Fund Risk Classification Methodology for Use in Fund Facts on January 29, 2015.

On December 10, 2015, staff published proposed rule amendments relating to the Proposed Methodology for first comment. The 90 day comment period ends March 9, 2016.

1.3 Accredited Investor Exemption for Investment

As part of the OSC and CSA's exempt market initiative, we amended the accredited investor exemption to permit fully managed accounts, where the advisor has a fiduciary relationship with the investor, to purchase any securities on an exempt basis, including investment fund securities. Previously, in Ontario, investment funds were carved out of the managed account category of the accredited investor exemption. Removing the carve-out harmonized the managed account category of the accredited investor exemption in all Canadian jurisdictions. This amendment came into effect on May 5, 2015.

1.4 Modernization of Investment Fund Product Regulation

During the year, work continued on the final stage of the CSA’s project to modernize investment fund product regulation (the Modernization Project). This final stage focuses on creating a comprehensive framework for funds that use alternative strategies, which we refer to as “alternative funds”. We are also considering whether congruent amendments to the current rules applicable to investment fund strategies are needed.

On February 12, 2015, the CSA published CSA Staff Notice 81-326 Update on an Alternative Funds Framework for Investment Funds to provide an update on the status of the project and to outline the proposed next steps in the project. The Notice also summarizes key themes from public comments provided in response to a request for feedback on a proposal for an alternative funds framework published in the prior stage of the Modernization Project.

Throughout 2015, the CSA engaged in consultations with various stakeholders regarding the key themes from commenters. Based on the feedback received, we have begun to draft proposed amendments to the applicable National Instruments for an alternative funds regime, with a view to publishing the amendments for public comment in mid-2016.

2. Emerging Issues and Trends

2.1 Update on Structured Note Offerings

We review and monitor structured note pricing supplements filed under National Instrument 44-102 Shelf Distributions. As part of our monitoring of the structured products market, we are in the process of collecting market data about structured notes from their issuers. The data will provide us with aggregate market size information, aggregate fund flows, and the key features of each structured note issued. The data will be updated quarterly, giving us timely market information to improve our ability to detect market trends at an early stage.

In January 2015, the CSA published CSA Staff Notice 44-305 Structured Notes Distributed under the Shelf Prospectus System (SN 44-305). SN 44-305 covered topics including:

- disclosure of the issuer’s estimate of the note’s fair value, with a view to improving transparency regarding the estimated profit embedded in the note,

- on-going disclosure that issuers should consider providing to investors,

- our views regarding the use of investment funds and managed portfolios as reference assets, and

- the process for filing structured note pricing supplements.

During 2015, we received numerous questions regarding the topics covered in SN 44-305.

In the upcoming year, we intend to publish OSC staff responses to frequently occurring questions to provide guidance to the industry.

We will continue to consider whether gaps may exist under our current regulatory approach to structured notes and whether more formal regulatory requirements may be necessary to ensure we are regulating similar products in a consistent way to achieve investor protection and promote fair and efficient capital markets.

2.2 Past Performance Presentation in the Fund Facts

Mutual funds are required to provide disclosure of past performance in the Fund Facts under the “How has this fund performed?” section. The Fund Facts requires the presentation of a year-by year return chart, a best and worst 3-month return chart, and the average annual return for a mutual fund. In the course of our prospectus reviews, we have noticed certain scenarios that are not contemplated by the Fund Facts form requirements, which could lead to inconsistent or unclear disclosure.

The Fund Facts is required to be prepared for each class or series of a mutual fund. We have encountered situations where certain classes or series of a fund had periods during which no securities were outstanding. In such circumstances, it may not be possible to show performance for a complete calendar year or to calculate an average annual return, since there are periods during which the class or series did not have any assets (asset gaps).

To maximize the utility of the Fund Facts for investors, staff have been requesting that fund managers consider alternative approaches to the presentation of past performance in situations where a class or series of a mutual fund experienced asset gaps. In response, some fund managers have used the performance record of another class or series of the mutual fund as a proxy for the missing performance information. When selecting the proxy class or series, staff have indicated that the fund manager should ensure that the fees are not lower than those of the class or series with the asset gap. In addition, the proxy class or series should not have any special features that would result in a material difference in performance, such as currency hedging. As well, staff expect that the Fund Facts include a notation indicating that the performance of a proxy class or series has been presented. We will continue to provide guidance on performance presentation in the Fund Facts as necessary.

2.3 Investment Funds that Track an Index

During 2015, we saw an increasing trend in offerings of investment funds whose investment objectives are to replicate the performance of an index, and whose name includes the word "index" (Index Tracking Funds). Issuers used the term “index” to refer to various types of strategies, including tracking proprietary portfolios that are actively managed by an investment advisor.

On July 9, 2015, we published OSC Staff Notice 81-728 Use of “Index” in Investment Fund Names and Objectives to provide guidance on our views of the characteristics that an “index” should possess. Staff’s view is that a fund that seeks to replicate the performance of an identified index is generally considered to be pursuing a passive investment strategy. In staff's view, the index whose performance an Index Tracking Fund is aiming to replicate (i) should not involve material discretion in the administration of the index, and (ii) should be transparent to assist investors in understanding the investment exposure provided by the index. Staff also indicated that if the index is not transparent or if the selection of the index constituents involved material discretion, we would require that the term “index” be removed from the fund name and its objectives. We will continue to monitor the use of the term “index” as we see more offerings of Index Tracking Funds, and provide additional guidance if necessary.

3. Disclosure and Compliance Reviews

The OSC reviews the prospectus and continuous disclosure filings of Ontario-based investment funds. We select investment funds for reviews of their disclosure documents using risk-based criteria. Staff may also choose to conduct targeted reviews of a particular industry segment or on a particular topic. For prospectus reviews, staff continue to focus on three areas: disclosure relating to different classes or series offered by investment funds; fees and expenses; and investment objectives and strategies. Further details on this can be found in the July 2015 issue of the Investment Funds Practitioner.

In addition to prospectus and continuous disclosure reviews, the Investment Funds and Structured Products Branch works closely with the Compliance and Registrant Regulation (CRR) Branch on issues related to investment fund manager compliance and identifying possible emerging issues. Joint reviews by the two Branches are conducted as necessary.

3.1 Continuous Disclosure Reviews

This section discusses some of our reviews and findings in connection with:

• mutual fund portfolio liquidity,

• active management of mutual funds,

• fund-of-funds fees disclosure,

• ETF portfolio transparency,

• reliance on proxy advisory firms, and

• IFRS.

3.1.1 Mutual Fund Portfolio Liquidity

In 2015, staff completed a series of targeted reviews focused on mutual fund practices relating to (i) liquidity assessments of fund holdings, (ii) liquidity stress testing, and (iii) liquidity valuation considerations. We focused on funds that invest in asset classes that were considered to be more susceptible to liquidity concerns, including high yield debt funds, emerging market funds and small capitalization equity funds. On June 25, 2015, we published OSC Staff Notice 81-727 Report on Staff’s Continuous Disclosure Review of Mutual Fund Practices Relating to Portfolio Liquidity to summarize our findings and provide related guidance to fund managers.

Staff’s recommendations to fund managers included:

- having robust policies and procedures on liquidity assessments at the time of purchase of an investment and on an on-going basis, with assessments that are based on objective and relevant metrics,

- having written stress testing policies and procedures in place at the time of purchase of an investment and on an on-going basis, including using scenario analysis that incorporate redemption rates that exceed past redemption experience, and

- using valuation procedures that take into account the market conditions for the portfolio asset.

We continue to monitor developments in this area, including the proposed liquidity management rules for mutual funds and ETFs that were published for comment by the U.S. Securities and Exchange Commission in September 2015. We will publish additional guidance as needed.

3.1.2 Active Management of Mutual Funds

We commenced a targeted review of conventional mutual funds that disclose in their prospectus and marketing materials that they pursue active management strategies. Our review examined whether the funds are actively managed or whether they exhibit a close tracking of their benchmark index (often referred to as “closet indexation”).

Among other data, we considered the funds’ active share (a measure of the percentage of a fund’s portfolio holdings that differs from the composition of its benchmark index) to assess the extent of active management. We have written to selected managers of Canadian equity funds to obtain a better understanding of their investment strategies and the reasons why the strategies resulted in investment portfolios that overlap significantly with the composition of their benchmark index. We have received responses and are in the process of reviewing and requesting additional information, including whether the securities selection process for the funds is affected by the managers’ evaluation of their funds’ performance relative to their benchmark index.

3.1.3 Fund-of-Funds Fees Disclosure

During the year, we conducted a review that focused on the disclosure of fees and expenses in fund-of-funds structures. The objectives of the review are to ensure that the layering of fees in fund-of funds structures is fully transparent and that the calculation of the management expense ratio (MER) and trading expense ratio (TER) includes the expenses of underlying funds in compliance with National Instrument 81-106 Investment Fund Continuous Disclosure (NI 81-106). Our review included both public and private funds.

In our review, we:

- asked how the funds comply with the MER and TER calculation requirements mandated in NI 81-106 for fund-of-funds structures,

- sought information about the fund manager’s policies and procedures to verify that there is no duplication of fees by investing in underlying funds, and

- reviewed offering documents and continuous disclosure documents to ensure that the disclosure about the fees and expenses associated with an investment in the underlying funds is clear.

Based on the preliminary responses received, staff have identified errors in the calculation of the MER and TER by a few fund managers of publicly-offered funds; in particular, the MERs and TERs did not include the expenses of the underlying funds, resulting in a refiling of the management reports of fund performance to correct these ratios. We have expanded the review to encompass more fund managers, and will consider publishing guidance when our review is completed.

3.1.4 ETF Portfolio Transparency

Staff commenced a review of the practices of ETF managers with respect to the disclosure of their ETFs’ portfolio holdings and other information that is provided daily for the purpose of subscribing for and redeeming securities of their ETFs. We understand that ETF managers have varying practices for providing this information and we would like to understand the reasons for the differences. We have written to each Ontario-based ETF manager to gather information, and are reviewing their responses.

3.1.5 Reliance on Proxy Advisory Firms

On April 30, 2015, the CSA published National Policy 25-201 Guidance for Proxy Advisory Firms. Related to this, staff are reviewing the reliance of fund managers on proxy advisory firms in voting the portfolio securities of the investment funds that they manage. We have written to a sample of fund managers that manage conventional mutual funds and ETFs to request information regarding their use of proxy advisory firms, including:

- information regarding the fund manager’s use of proxy advisory firms and the due diligence conducted before subscribing for the firms’ reports (Advisory Reports),

- information regarding the process for identifying any conflicts of interest that a proxy advisory firm may have in respect of a particular matter to be voted upon, and the fund manager’s process when such conflicts are identified,

- a copy of the proxy voting guidelines that the funds follow when voting shares of investee companies, and

- information regarding steps taken when the fund manager learns that an Advisory Report to which it subscribes contains factual errors or inaccuracies, or has been updated to reflect new publicly available information.

Staff are currently reviewing the responses received and will consider whether guidance in this area is necessary.

3.1.6 IFRS

Investment funds that are subject to NI 81-106 were required to adopt International Financial Reporting Standards (IFRS) for financial years beginning on or after January 1, 2014. In 2014, we conducted an issue-oriented review of interim financial reports for the period ended June 30, 2014, being the first IFRS financial statements that were required to be filed. Our review focused on the transition requirements set out in IFRS and in NI 81-106. In 2014–15, we issued four IFRS Releases to provide feedback to the industry on the outcome of the reviews and to provide guidance to investment funds that had not yet filed their first IFRS financial statements.

In 2015, we expanded our review by examining a sample of the IFRS audited annual financial statements for investment funds with a financial year ended March 31, 2015. The results of our 2015 review are summarized in the December 2015 edition of the Investment Funds Practitioner.

As we did not identify any widespread issues in the IFRS audited financial statements and related management reports of fund performance, we will not extend our review of compliance with the transition to IFRS.

3.2 Compliance and Registrant Regulation Branch Reviews of Investment Fund Managers

In September 2015, staff of the CRR Branch published OSC Staff Notice 33-746 Annual Summary Report for Dealers, Advisers and Investment Fund Managers. This Notice summarizes new and proposed rules and initiatives impacting registrants, current trends in deficiencies from compliance reviews of registrants (as well as suggested practices to address the deficiencies and inappropriate practices to prevent them), and current trends in registration matters.

Section 4.4 of the Notice contains information specifically for fund managers derived from the reviews carried out by the CRR Branch. Topics covered in this section include:

- repeat common deficiencies, including inappropriate expenses charged to funds, inadequate oversight of outsourced functions and service providers, and non-delivery of net asset value adjustments,

- non-compliance by fund managers of private investment funds of the prohibition on commingling fund assets with assets of the fund manager,

- non-compliance of the inter-fund trading prohibition for private investment funds, and

- new and proposed rules and initiatives impacting fund managers.

We encourage fund managers to consider the issues and guidance in the Notice.

4. Outreach, Consultation and Education

We continue our efforts to be transparent regarding practices and procedures that impact investment fund issuers in as timely a manner as possible. Our intent in doing so is to better enable fund managers and their advisors to address potential regulatory issues when they are at the planning stage for a new fund or transaction. As indicated in this report, we publish guidance and updates for the investment fund industry periodically.

We engage in periodic discussions with other regulators such as the Mutual Fund Dealers Association of Canada and the Investment Industry Regulatory Organization of Canada. Additionally, on an on-going basis, we seek input from the OSC’s Investment Funds Product Advisory Committee (see below) and Investor Advisory Panel, as well as other industry and investor organizations and stakeholders.

As in past years, we met with staff from the Investment Management and Derivatives divisions of the U.S. Securities and Exchange Commission to discuss investment fund trends, novel products and emerging issues that are common to our respective jurisdictions. These meetings help ensure that our regulatory approaches to product development are consistent and that opportunities for regulatory arbitrage between our markets are minimized.

To facilitate effective national oversight of the investment fund industry, the CSA’s Investment Funds Committee holds monthly conference calls. The Committee consists of representatives from other securities regulators in Canada. It provides a forum for discussing novel applications and products, policy interpretation and initiatives, and operational matters in a timely fashion. The discussions help promote the consistent, fair and effective application of regulatory requirements under the Passport system. Darren McKall of the OSC is currently Chair of the Committee.

The OSC website provides tools and resources for investors to learn about investments and investing. We worked with the Office of Investor Policy, Education and Outreach (OIPEO) to publish "Investing 101: Structured Notes" on February 23, 2015. This investor news piece highlights key features that investors should consider before making an investment in structured notes. As well, we worked with the OIPEO to publish "Investing 101: Indices and Index Funds" on July 27, 2015. This investor news piece explains what an index is and how index funds work, including key features investors should be aware of before purchasing an index fund.

4.1 Investment Funds Product Advisory Committee (IFPAC)

The OSC's IFPAC was established in August 2011. The IFPAC, which currently comprises 12 external members, advises staff on emerging product developments and innovations occurring in the investment fund industry. The IFPAC also acts as a source of feedback to staff on the development of policy to promote investor protection, fairness and market efficiency across all types of investment fund products. The IFPAC typically meets quarterly and members serve a two year term. When the current two year term expired in spring 2015, six members returned and six new members joined. A list of current IFPAC members can be found on the OSC website.

Topics of discussion with the IFPAC in 2015 included: the ETF market and trends; retail risk rating perspectives; OSC Staff Consultation Paper 15-401 Proposed Framework for an OSC Whistleblower Program; indexing methodologies; and the Brondesbury Report (referred to under “Key Policy Initiatives – Mutual Fund Fees” in this Report). At the first meeting of the reconstituted committee, the IFPAC also discussed an overview of our current branch policy initiatives, including the project to modernize investment fund product regulation, the mutual fund fees initiative and the POS Project.

4.2 The Investment Funds Practitioner

The Investment Funds Practitioner is an overview of topical issues arising from applications for discretionary relief, prospectuses and continuous disclosure documents that are reviewed by the Investment Funds and Structured Products Branch. This publication is intended to assist fund managers and their advisors who prepare public disclosure documents and applications for discretionary relief on behalf of investment funds. The Practitioner is also intended to make fund managers more broadly aware of some of the issues we have raised in connection with our reviews and how we have resolved them. We encourage fund managers and their advisors to review the Practitioner and welcome suggestions for future topics.

We published three editions of the Investment Funds Practitioner in 2015, in April, July and December. These editions, and prior editions, can be found on our website www.osc.ca at Information for Investment Funds. A Table of Contents for all of the editions of the Practitioner is available on the OSC website. The Table of Contents is organized by topic and can be used as a quick reference guide for locating topics discussed in the Practitioners published.

4.3 International Organization of Securities Commissions - Committee 5 - Investment Management (IOSCO C5)

We continued to participate in IOSCO C5 during 2015. This committee is focused on investment management issues and comprises representatives from 31 regulators. The international developments and priorities discussed at C5 inform our policy and operational work, which is also guided by the principles and best practices published by IOSCO.

During the year, IOSCO C5 published its final report on good practices on reducing reliance on credit rating agencies in asset management, which provides a set of recommended practices for reducing over-reliance on external credit ratings in the asset management industry. IOSCO C5 also published its final report on standards for the custody of collective investment schemes’ assets to clarify, modernize and develop international guidance in this area.

Current IOSCO C5 initiatives include conducting consultations on fees and expenses of investment funds to update prior IOSCO work in this area, and consultations on best practices for the voluntary termination of an investment fund, including fund mergers and reorganizations. In 2015, we also participated in IOSCO C5’s survey on the tools available to collective investment schemes to manage liquidity risks. The committee published its report based on responses from 26 member jurisdictions in December 2015.

In March 2015, IOSCO, together with the Financial Stability Board, published for a second consultation proposed methodologies for the identification of systemically-important asset management entities. However, in June 2015, the IOSCO Board determined that a full review of asset management activities and products in the broader global financial context should be the immediate focus of international efforts to identify potential systemic risks and vulnerabilities. The Board was of the view that this review should be completed prior to undertaking any further work on methodologies for the identification of such entities. Since that time, IOSCO C5 has been engaged in this review.

5. Feedback and Contact Information

If you have any feedback or questions regarding our annual summary report, please send them to <[email protected]>.

You can find additional information regarding investment funds and the Investment Funds and Structured Products Branch on the OSC website.

We have also attached a list of Investment Funds and Structured Products Branch staff at the end of this report.

Investment Funds and Structured Products Branch Contact Information

| NAME | |

| Nunes, Vera – Director (Acting) | [email protected] |

| Chan, Raymond – Manager | [email protected] |

| McKall, Darren – Manager | [email protected] |

| Paglia, Stephen – Manager (Acting) | [email protected] |

| Alamsjah, Rosni – Administrative Assistant | [email protected] |

| Asadi, Mostafa – Senior Legal Counsel | [email protected] |

| Bahuguna, Shaill – Administrative Support Clerk | [email protected] |

| Barker, Stacey – Senior Accountant | [email protected] |

| Bent, Christopher – Legal Counsel | [email protected] |

| Buenaflor, Eric – Financial Examiner | [email protected] |

| De Leon, Joan – Review Officer | [email protected] |

| Gerra, Frederick – Legal Counsel | [email protected] |

| Huang, Pei-Ching – Senior Legal Counsel | [email protected] |

| Jaisaree, Parbatee – Administrative Assistant | [email protected] |

| Joshi, Meenu – Accountant | [email protected] |

| Kalra, Ritu – Senior Accountant | [email protected] |

| Lee, Bryana – Legal Counsel | [email protected] |

| Lee, Irene – Senior Legal Counsel | [email protected] |

| Mainville, Chantal – Senior Legal Counsel | [email protected] |

| Marcovici, Harald – Legal Counsel | [email protected] |

| Nania, Viraf – Senior Accountant | [email protected] |

| Papini, Andrew – Legal Counsel | [email protected] |

| Persaud, Violet – Review Officer | [email protected] |

| Rana, Marilyn – Administrative Assistant | [email protected] |

| Russo, Nicole – Review Officer | [email protected] |

| Schofield, Melissa – Senior Legal Counsel | [email protected] |

| Thomas, Susan – Senior Legal Counsel | [email protected] |

| Tong, Louisa – Administrative Assistant | [email protected] |

| Welsh, Doug – Senior Legal Counsel | [email protected] |

| Yu, Sovener – Senior Accountant | [email protected] |

| Zaman, Abid – Accountant | [email protected] |

If you have questions or comments about this report, please contact:

|

Vera Nunes |

Pei-Ching Huang |