National Instrument 94-102 Derivatives: Customer Clearing and Protection of Customer Collateral and Positions and Related Companion Policy

National Instrument 94-102 Derivatives: Customer Clearing and Protection of Customer Collateral and Positions and Related Companion Policy

CSA Notice of

National Instrument 94-102 Derivatives: Customer Clearing and

Protection of Customer Collateral and Positions

and

Related Companion Policy

CSA Notice of National Instrument 94-102 Derivatives: Customer Clearing and Protection of Customer Collateral and Positions and Related Companion Policy

January 19, 2017

Introduction

The Canadian Securities Administrators (the CSA or we), are adopting:

• National Instrument 94-102 Derivatives: Customer Clearing and Protection of Customer Collateral and Positions including:

January 19, 2017

Introduction

The Canadian Securities Administrators (the CSA or we), are adopting:

• National Instrument 94-102 Derivatives: Customer Clearing and Protection of Customer Collateral and Positions including:

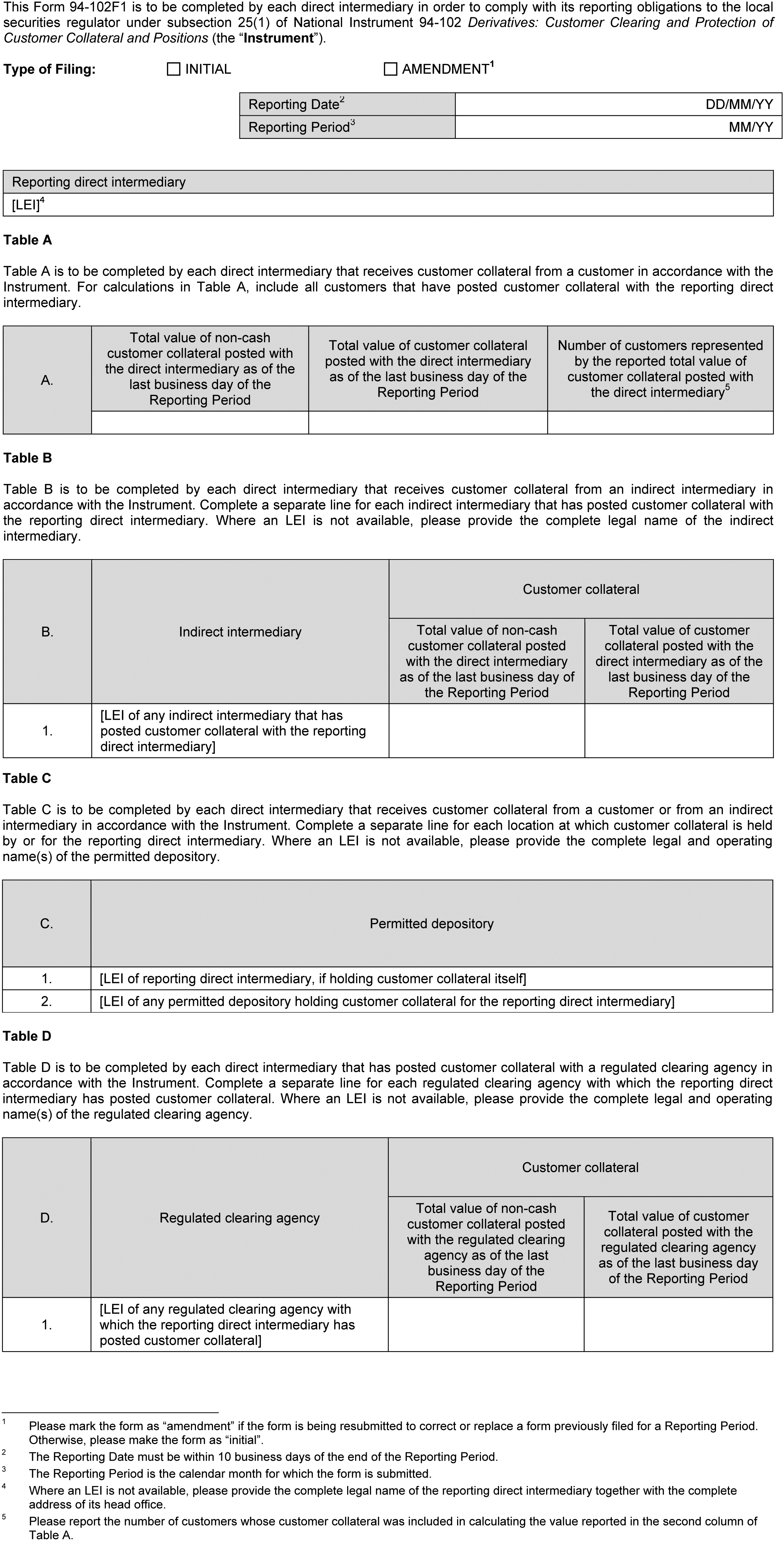

• Form 94-102F1 Customer Collateral Report: Direct Intermediary

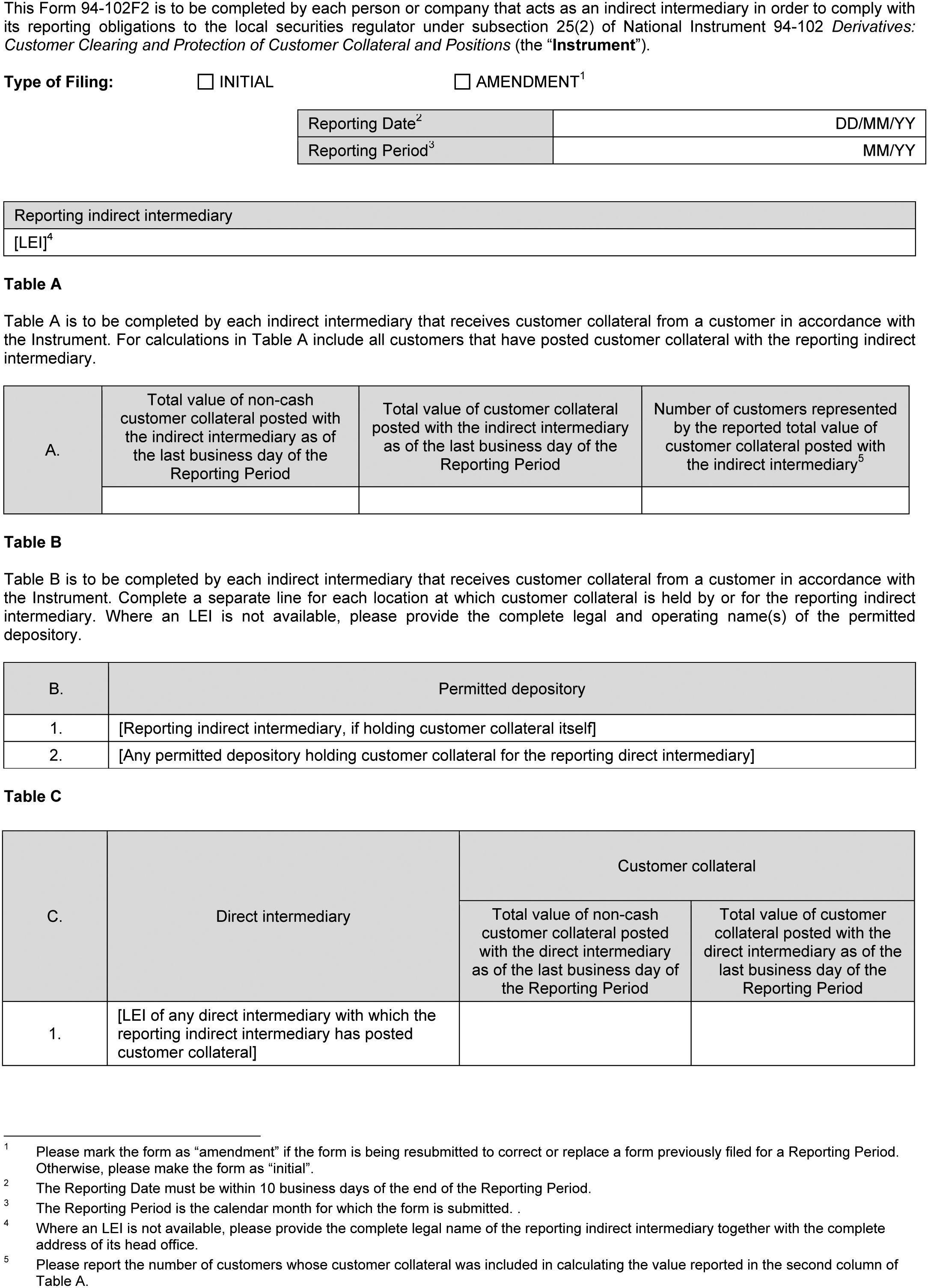

• Form 94-102F2 Customer Collateral Report: Indirect Intermediary

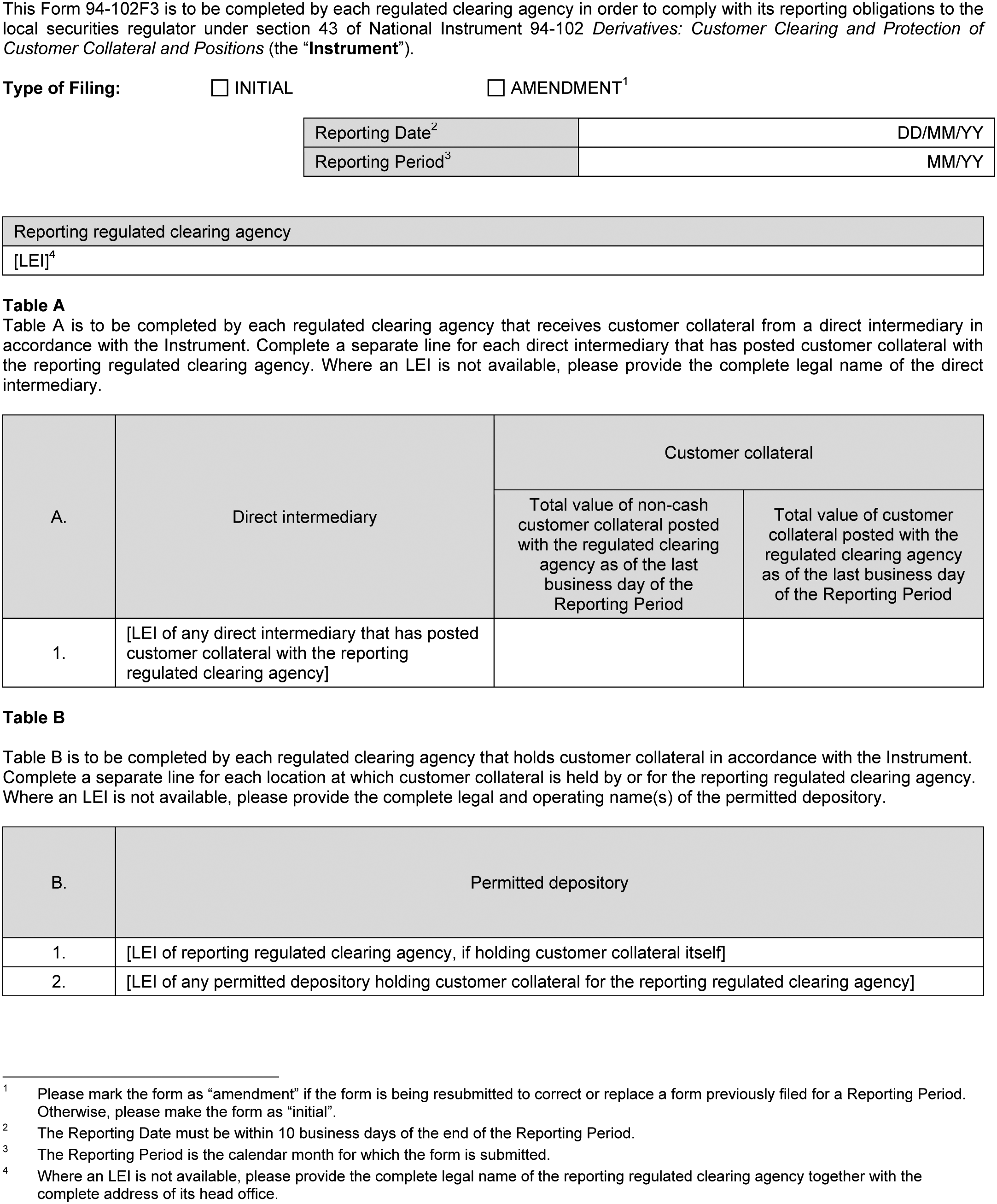

• Form 94-102F3 Customer Collateral Report: Regulated Clearing Agency

(the Instrument), and

• Companion Policy 94-102 Derivatives: Customer Clearing and Protection of Customer Collateral and Positions (the CP)

(together, the National Instrument).

In some jurisdictions, government ministerial approvals are required for the implementation of the Instrument. Provided all necessary approvals are obtained, the National Instrument will come into force on July 3, 2017.

The CSA Derivatives Committee (the Committee) has consulted and collaborated with the Bank of Canada, the Office of the Superintendent of Financial Institutions (Canada), the Department of Finance Canada and market participants on the National Instrument. The Committee also continues to contribute to and follow international regulatory developments. In particular, members of the Committee work with international regulators and bodies such as the International Organization of Securities Commissions and the OTC Derivatives Regulators' Group in the development of international standards and regulatory practices.

Although a significant market in Canada, the Canadian over-the-counter (OTC) derivatives market comprises a relatively small share of the global market, and a substantial portion of derivatives entered into by Canadian market participants involve foreign counterparties. The CSA endeavours to develop rules for the Canadian market that are aligned with international practices to ensure that Canadian market participants have access to the international market and are regulated in accordance with international principles.

We would like to draw your attention to another publication: CSA Notice of National Instrument 94-101 Mandatory Central Counterparty Clearing of Derivatives which is being published concurrently with this Notice. This publication, and the National Instrument, relate to central counterparty clearing.

Substance and Purpose

The purpose of the Instrument is to ensure that the clearing of a local customer's OTC derivatives is carried out in a manner that protects the customer's positions and collateral and improves derivatives clearing agencies' resilience to default by a clearing intermediary. For a more detailed explanation of customer clearing please see CSA Consultation Paper 91-404 Derivatives: Segregation and Portability in OTC Derivatives Clearing.{1}

The Instrument contains requirements for the treatment of customer collateral by clearing intermediaries providing clearing services to local customers and derivatives clearing agencies located in Canada or providing clearing services to local customers. The Instrument includes requirements relating to the segregation and use of customer collateral that are designed to protect customer collateral, particularly in the case of financial difficulties of a clearing intermediary. The Instrument also includes detailed recordkeeping, reporting and disclosure requirements intended to make customer collateral and positions readily identifiable. Finally, the Instrument contains requirements relating to the transfer or porting of customer collateral and positions intended to result, in the event of default or insolvency of a clearing intermediary, that customer collateral and positions can be transferred to one or more non-defaulting clearing intermediaries.

Background and Summary of Written Comments Received by the CSA

On January 16, 2014, the CSA published for comment CSA Notice 91-304 Proposed Model Provincial Rule on Derivatives: Customer Clearing and Protection of Customer Collateral and Positions (the Model Rule). The Committee modified the Model Rule in response to public comments and on January 21, 2016, Proposed National Instrument 94-102 Derivatives: Customer Clearing and Protection of Customer Collateral and Positions (the Proposed Instrument) was published by CSA Notice for a 90-day comment period.

During the last comment period, we received submissions from six commenters on the Proposed Instrument. We thank all of the commenters for their input. We have carefully reviewed the comments received and revised the Proposed Instrument. The names of the commenters and a summary of their comments, together with our responses, are contained in Annex A of this Notice. Copies of the submissions on the Proposed Instrument can be found on the websites of the Alberta Securities Commission, Ontario Securities Commission{2} and Autorité des marchés financiers.{3}

Summary of the Instrument

The Instrument is divided into 11 Parts.

Part 1 of the Instrument sets out relevant definitions and specifies that the Instrument applies only to cleared OTC derivatives where a customer, regulated clearing agency or clearing intermediary has a specified nexus to a local jurisdiction.

Part 2 to Part 4 of the Instrument set out requirements applicable to clearing intermediaries with respect to treatment of customer collateral, recordkeeping and disclosure.

Part 2 of the Instrument sets out the manner in which a customer's collateral is to be treated by clearing intermediaries, including requirements in respect of the collection, holding and maintenance of customer collateral, the identification of excess margin as well as the segregation, use and investment of customer collateral. Part 2 also sets out requirements that a clearing intermediary must meet to provide clearing services to a local customer including appropriate risk management in respect of those services.

Under Part 3 of the Instrument, clearing intermediaries are required to keep and retain certain records and supporting documentation as well as keep adequate and appropriately updated books and records that facilitate the identification and protection of a customer's positions and collateral.

Part 4 of the Instrument sets out reporting and disclosure requirements for clearing intermediaries, including reporting required to be submitted to the regulator or the securities regulatory authority.

Part 5 to Part 7 of the Instrument are parallel to Part 2 to Part 4 of the Instrument and set out similar requirements as they apply to regulated clearing agencies.

Part 5 of the Instrument sets out how a customer's collateral is to be treated by regulated clearing agencies, including requirements in respect of the collection, holding and maintenance of customer collateral, the identification of excess margin as well as the segregation, use and investment of customer collateral.

Under Part 6 of the Instrument, regulated clearing agencies are required to keep certain records and supporting documentation as well as keep adequate and appropriately updated books and records that facilitate the identification and protection of a customer's positions and collateral.

Part 7 of the Instrument sets out reporting and disclosure requirements for regulated clearing agencies, including reporting required to be submitted to the regulator or the securities regulatory authority.

Part 8 of the Instrument sets out the requirements for a regulated clearing agency to facilitate the transfer of a customer's positions and collateral in the context of a clearing intermediary's default or at the request of a customer. Part 8 also requires a clearing intermediary that provides clearing services to an indirect intermediary to have policies and procedures for transferring the positions and collateral of a customer of the indirect intermediary.

Under Part 9 of the Instrument, clearing intermediaries and regulated clearing agencies located outside Canada may be exempt from the Instrument if they comply with the requirements of comparable legislation of a foreign jurisdiction specified in Appendix A to the Instrument. Despite the exemption from the Instrument provided for in Part 9, clearing intermediaries and regulated clearing agencies that offer clearing services to local customers will remain subject to certain provisions under the Instrument, as specified in Appendix A to the Instrument.

Part 10 of the Instrument contains provisions authorizing the regulator or the securities regulatory authority, as the case may be, to grant an exemption from any provision of the Instrument.

Part 11 of the Instrument sets out the effective date for the Instrument.

Summary of Changes to the Proposed Instrument

(a) Non-application to OTC options on securities

We received comments noting that the Instrument would extend the application of segregation and portability requirements to options on securities in a manner that is inconsistent with other regulatory regimes internationally. In response to these comments, we determined that the Instrument will not apply to OTC options on securities. Under securities legislation in Canada, options on securities are subject to regulation as securities, or in Québec as derivatives.{4} Options on securities will continue to be regulated as securities, or in Québec as derivatives, under the existing securities legislation in Canada and remain subject to the investor protections included in these regimes. This is consistent with approaches employed in the United States and the European Union.

(b) Record retention

Changes have been made to the record retention provisions for clearing intermediaries and regulated clearing agencies to avoid duplicative retention of records. These changes were made in response to several comments received that pointed out how recordkeeping efficiencies could be incorporated into the Instrument.

For clearing intermediaries, different retention requirements apply to (i) records and documentation related to individual cleared derivatives and (ii) all other records and information collected for a customer. Records related to a cleared derivative are required to be retained for at least seven years after the expiration of the cleared derivative while customer profiles, account agreements or other general information collected from a customer at any time by a clearing intermediary providing clearing services for the customer must be kept for at least seven years after the date upon which the customer's last derivative that is cleared with the clearing intermediary expires or is terminated.

Regulated clearing agencies are now required to keep records only until the expiry or termination of the cleared derivative to which the record relates. Since clearing intermediaries are required to maintain records relating to a particular cleared derivative for at least seven years after the termination of the cleared derivative, this change to the Instrument avoids duplication of the records already maintained by clearing intermediaries.

(c) Transfer of collateral and positions upon default vs. business-as-usual

We received comments discussing the challenges associated with transferring a customer's positions and collateral in both non-default, or "business-as-usual", transfer scenarios and during the default of a direct intermediary. In particular, the commenters noted that in a default scenario, it is sometimes necessary to rely on negative consent from a customer (i.e., the customer's silence), where a customer has not provided instructions or it is not possible to transfer a customer's collateral and positions in accordance with its instructions. We acknowledge there are differences between a transfer of a customer's positions and collateral upon default by a direct intermediary and a business-as-usual transfer upon request from the customer, and separate provisions for these scenarios have been included in the Instrument. The provision relating to the transfer of a customer's positions and collateral upon default by a direct intermediary provides additional flexibility to facilitate a transfer while taking into account any instructions that a customer may have provided in contemplation of a clearing intermediary's default.

(d) Substituted compliance

Currently, OTC derivatives clearing infrastructure and clearing service providers are largely concentrated outside of Canada. Therefore, it is likely that many local customers' cleared derivatives will involve foreign clearing infrastructure or clearing service providers. We received comments requesting exemptions from the Instrument where a clearing intermediary or regulated clearing agency complies with comparable laws of a foreign jurisdiction. As a result, we carefully considered the interaction of the Instrument with foreign customer clearing regimes that may also apply to a cleared derivative involving local customers. The Instrument provides for an exemption from the Instrument based on the concept of substituted compliance where a foreign clearing intermediary or regulated clearing agency in compliance with the comparable laws of the United States or the European Union is involved in clearing a local customer's cleared derivatives. However, despite a clearing intermediary or regulated clearing agency qualifying for the exemption from the Instrument by substituted compliance, certain provisions in the Instrument will still apply to foreign entities providing clearing services to local customers. These "residual provisions" include the retention of records, reporting on customer collateral to the customer and the regulator and the segregation of customer collateral from other property of the customer. The residual provisions that apply to a clearing intermediary or regulated clearing agency depend on the comparability of the applicable foreign laws, and therefore on whether the foreign entity complies with the laws of the United States or the European Union.

(e) Customer collateral reports -- regulatory

We received comments regarding the information about customer collateral required to be reported to the regulator or securities regulatory authority. Commenters asked that the information reported by clearing intermediaries and regulated clearing agencies in Form 94-102F1, Form 94-102F2 and Form 94-102F3 pursuant to section 25 and section 43 of the Instrument be more closely harmonized with similar reporting requirements under the U.S. Commodity Futures Trading Commission's rules. In response to these comments, among other changes, information on customer collateral is now required on an aggregate basis, rather than on an individual customer basis.

Commenters also requested that reporting on customer collateral to the regulator or securities regulatory authority be included in the provisions for which an exemption based on substituted compliance is available. However, the information reported on Form 94-102F1, Form 94-102F2 and Form 94-102F3 is of importance to securities regulatory authorities. Consequently, section 25 and section 43 of the Instrument are not included in the exemption based on substituted compliance.

(f) International harmonization and miscellaneous drafting clarifications

There are a number of drafting changes throughout the Instrument to respond to comments from clearing agencies and clearing intermediaries that work to harmonize the Instrument with international regulatory regimes and more accurately reflect customer collateral and position segregation, recordkeeping and reporting practices.

Local Matters

The scope of derivatives subject to the Instrument in each local jurisdiction is set out in Ontario Securities Commission Rule 91-506 Derivatives: Product Determination,{5} Manitoba Securities Commission Rule 91-506 Derivatives: Product Determination,{6} Québec Regulation 91-506 respecting Derivatives Determination{7} (Québec Regulation 91-506) and Multilateral Instrument 91-101 Derivatives: Product Determination.{8}

Concurrently with the publication of this Notice, the Autorité des marchés financiers is publishing consequential amendments in respect of the National Instrument to Regulation 91-506.

Anticipated Costs and Benefits

The Instrument is intended to facilitate development of the Canadian market for clearing customer OTC derivatives in a safe and efficient manner. It is intended to provide investor protection for local customers using clearing services that are equivalent to the protections offered in major foreign markets and provide systemic benefits to the Canadian market. There will be compliance costs for clearing service providers that may increase the cost of clearing for market participants. The benefits to the Canadian market and to local customers from implementing the Instrument significantly outweigh the compliance costs to market participants. The major benefits and costs of the Instrument are described below.

(a) Benefits

The two major benefits of the Instrument are the reduction of systemic risk and the protection of customers and their assets when they clear OTC derivatives through clearing agencies.

(i) Mitigation of Systemic Risk

The Group of Twenty has agreed that requiring standardized and sufficiently liquid OTC derivatives to be cleared through central counterparties will result in more effective management of counterparty credit risk. The clearing of OTC derivatives may also contribute to greater stability of our financial markets and to a reduction in systemic risk. Along with mandatory central counterparty clearing, minimum capital requirements and margin requirements for non-centrally cleared derivatives may create additional incentives for central counterparty clearing.

The Instrument is designed to create a framework for customer clearing that promotes stability of the OTC derivatives market by facilitating, to the greatest extent possible, the porting of customers' positions and collateral. Portability of customers' positions and collateral is a key mechanism to ensure that in the event of a clearing intermediary default or insolvency, customers' positions are not terminated and their positions and collateral can be transferred to one or more non-defaulting clearing intermediaries. Portability can mitigate difficulties associated with stressed market conditions such as a market-wide reduction in liquidity and price dislocation, allow customers to maintain continuous clearing access and generally promotes efficient financial markets.

(ii) Customer Protection

The Instrument is aimed at significantly reducing the likelihood that customers will suffer major financial losses in the event of a clearing service provider's insolvency. In general, customer clearing offers risk mitigation benefits to customers. However, if a robust customer protection regime is not in effect, there can be risks in the clearing process, particularly if a clearing intermediary becomes insolvent. The Instrument provides customer protections that should significantly reduce the likelihood of a range of negative potential consequences, that could occur in the event of a clearing intermediary's insolvency, including:

• forced liquidation of positions;

• loss or inaccessibility of collateral;

• loss of hedge positions necessitating re-entry into the market at time of stress to re-establish positions; and

• market uncertainty.

The Instrument mitigates many of these risks to customers by establishing robust collateral and recordkeeping requirements. It requires a customer's positions to be collateralized at the regulated clearing agency and obligates the regulated clearing agency and clearing intermediaries to keep records that identify customers and their positions in order to facilitate porting.{9}

(b) Costs

Generally, any increased costs resulting from compliance with the Instrument stem from enhanced collateral protection and recordkeeping and reporting requirements for customer collateral and positions. Any costs associated with complying with the Instrument will be borne by clearing intermediaries and regulated clearing agencies and may be passed on to customers through higher initial margin or higher fees for cleared derivatives. There is also a possibility that clearing service providers may be dissuaded from entering or remaining in the Canadian market due to the costs of complying with the Instrument, which would reduce local customers' options for clearing service providers.

(i) Establishing Systems

Clearing intermediaries and regulated clearing agencies may incur up-front costs to develop or modify their recordkeeping and account structure systems in order to comply with the Instrument. However, once the systems are established, the incremental cost of on-going compliance should be less significant.

(ii) Loss of Potential Revenue for Clearing Intermediaries and Clearing Agencies

The Instrument places restrictions on the use and investment of customer collateral held by clearing intermediaries and clearing agencies. Customer collateral may only be invested in liquid and low-risk instruments. The Instrument also requires a regulated clearing agency to collect initial margin from clearing intermediaries for each customer on a gross basis. Collecting gross margin promotes more effective porting of positions which benefits customers. However, this requirement means that less customer collateral will be held at and available for use by clearing intermediaries. These requirements limit the potential revenue that clearing intermediaries and clearing agencies may earn through the use and investment of their customers' collateral.

(iii) Market Access Issues

Currently, OTC derivatives clearing infrastructure and service providers are largely concentrated outside of Canada with the main clearing agencies and clearing intermediaries located in the United States and the European Union. Given the small size of the Canadian market, there is a risk that the costs of analyzing and complying with the Instrument may result in some market participants choosing not to offer customer clearing services in Canada which may limit local customers' access to OTC derivatives clearing services. However, as described above, the Instrument provides for an exemption for clearing intermediaries and regulated clearing agencies located in foreign jurisdictions based on substituted compliance with certain foreign laws. This exemption based on substituted compliance could significantly reduce compliance costs associated with the Instrument for providers of clearing services located in and complying with the laws of the foreign jurisdictions set out in Appendix A to the Instrument.

(c) Conclusion

Protection of customers' positions and collateral is the fundamental principle of the Instrument. It is the Committee's view that the impact of the Instrument, including anticipated compliance costs for market participants, is proportional to the benefits sought. The Instrument aims to provide a level of protection similar to that offered to customers in other jurisdictions with significant OTC derivatives markets. To achieve a balance of interests, the Instrument is designed to deliver a high level of protection to customers transacting in OTC derivatives and create a safer environment in the Canadian market for customers to clear OTC derivatives, while allowing clearing service providers a flexible and competitive market to operate in.

Contents of Annexes

The following annexes form part of this CSA Notice:

• Annex A -- Summary of comments and CSA responses and list of commenters

• Annex B -- National Instrument 94-102 Derivatives: Customer Clearing and Protection of Customer Collateral and Positions

• Annex C -- Companion Policy 94-102CP Derivatives: Customer Clearing and Protection of Customer Collateral and Positions.

Questions

Please refer your questions to any of:

{1} Available at http://www.osc.gov.on.ca/documents/en/Securities-Category9/csa_20120210_91-404_segregation-portability.pdf and http://www.lautorite.qc.ca/files//pdf/consultations/derives/2012fev10-91-404-cons-en.pdf.

{2} Available at http://www.osc.gov.on.ca/en/51109.htm.

{3} Available at http://www.lautorite.qc.ca/en/previous-consultations-derivatives-pro.html.

{4} See National Instrument 14-101 Definitions for a list of statues and other instruments comprising "securities legislation" across Canada. Available at http://www.osc.gov.on.ca/en/14882.htm and http://www.lautorite.qc.ca/files//pdf/reglementation/valeurs-mobilieres/14-101/2011-01-01/2011jan01-14-101-vadmin-en.pdf.

{5} Available at https://www.osc.gov.on.ca/en/SecuritiesLaw_91-506.htm.

{6} Available at http://docs.mbsecurities.ca/msc/irp/en/item/101711/index.doc.

{7} Available at http://www2.publicationsduquebec.gouv.qc.ca/dynamicSearch/telecharge.php?type=3&file=/I_14_01/I14_01R0_1_A.HTM.

{8} Available at http://www.albertasecurities.com, http://www.bcsc.bc.ca, http://www.nbsc-cvmnb.ca, http://nssc.novascotia.ca and http://www.fcaa.gov.sk.ca/Securities%20Division.

{9} The level of protection afforded by the Instrument is dependent on the Instrument's interaction with other foreign and domestic laws such as bankruptcy and insolvency laws and the Payment Clearing and Settlement Act (Canada) as well as provincial and territorial personal property security laws including as they apply to cash collateral.

ANNEX A

SUMMARY OF COMMENTS AND CSA RESPONSES ON PROPOSED NATIONAL INSTRUMENT 94-102 DERIVATIVES: CUSTOMER CLEARING AND PROTECTION OF CUSTOMER COLLATERAL AND POSITIONS

1. Section Reference

2. Summary of Issues/Comments

3. Response

GENERAL COMMENTS

General Comments

Overall, commenters supported creating a domestic regime for the protection of customer positions and collateral to ensure that Canada's derivatives market functions efficiently and continues to maintain the confidence of market participants.

The Instrument addresses the need for a harmonized regime across Canada for the protection of customer positions and collateral. The Instrument furthers the aims of OTC derivatives reform set out by the Group of Twenty and supports the safe, effective and efficient function of Canada's OTC derivatives market.

Support was expressed for substituted compliance in the Instrument. In particular, support was expressed for the revisions that facilitate the operation of different customer clearing models and including the laws of the United States and European Union for substituted compliance. Other commenters cautioned that without an effective substituted compliance regime, the Instrument may result in overlapping, duplicative and burdensome requirements.

Exemptions based on substituted compliance are available where market participants are subject to foreign laws that are substantially the same, on an outcomes basis, as the Instrument, based on a review of the foreign laws. The Instrument permits substituted compliance in specified circumstances and subject to certain conditions where a foreign clearing intermediary or regulated clearing agency clears a derivative and is in compliance with the foreign laws listed in Appendix A to the Instrument.

Two commenters requested that orders exempting certain actions issued by foreign regulatory agencies be included in the substituted compliance approach used in the Instrument.

No change. To include exemptions made by foreign regulatory authorities in the substituted compliance approach under the Instrument would be an impermissible sub-delegation of a securities regulatory authority's legislative powers, as a foreign regulatory authority granting exemptions would be able to bypass the effect of the Instrument without the approval of the securities regulatory authority.

One commenter requested that customer disclosure rules under the U.S. Commodity Futures Trading Commission (CFTC) regulations be deemed equivalent to the disclosure rules in the Instrument. Additionally, the commenter suggested that the Instrument be aligned with the customer disclosure rules and market practice evidenced by CFTC Rule 1.55(k) Disclosure and Default Disclosure, in particular with respect to sections 21, 22, 23, 26 and 27.

Change made. An exemption based on substituted compliance is available to clearing intermediaries that provide disclosure in accordance with CFTC and European Market Infrastructure Regulation (EMIR) disclosure requirements. Additionally, the examples of information to be included in the disclosure provided as guidance in the CP have been clarified.

Two commenters requested clarification regarding whether equity options would be within the scope of the Instrument. It was noted that equity options have a specific margining process where initial margin is collected on a gross basis and there is no netting of opposite positions or resulting margin. The commenters suggest that the level of segregation required under the Proposed Instrument would adversely limit the margin efficiency investors are looking for when using OTC options in parallel with exchange-traded options and will impose a significant burden on equity options market participants that is not imposed in other foreign jurisdictions.

Change made. OTC options on securities are excluded from the scope of application of the Instrument.

One commenter noted that requirements in the Instrument should be applied consistently across all jurisdictions of Canada and harmonized with international regulations.

No change. The Instrument will be consistently applied across Canadian jurisdictions and is largely harmonized with international regulations.

One commenter noted that implementation of the Instrument will require significant technological, operational and rule changes for regulated clearing agencies and requested that appropriate timelines for compliance be provided in the Instrument.

Change made. The Instrument includes an implementation period to provide time for market participants to comply with the Instrument.

Two commenters requested that reporting obligations in the Instrument be revised to minimize duplicative reporting requirements for foreign clearing agencies, such as by accepting the same reports provided to the CFTC or National Futures Association (with information regarding non-Canadian customers removed). One commenter requested that the reporting obligations of clearing agencies be limited to information related to collateral held by Canadian intermediaries.

Change made. An exemption based on substituted compliance is available to regulated clearing agencies that act in accordance with CFTC and EMIR recordkeeping and reporting requirements.

PART 1: DEFINITIONS, INTERPRETATION AND APPLICATION

s. 1 -- Definitions and interpretation

General comments

One commenter requested that the definition of "cleared derivative" be modified to clarify the exclusion of exchange-traded derivatives from the scope of the definition of "cleared derivative" and from the scope of the Instrument as it applies to clearing agencies.

No change. Subsection 1(4) together with the application provisions in subsection 2(2) of the Instrument provide that the Instrument is limited only to the scope of derivatives set out in each local jurisdiction's derivatives product determination rule or regulation (the Product Determination Rules),{1} which exclude exchange-traded derivatives. Subsection 1(4) and Subsection 2(2) apply to the entirety of the Instrument, including the definitions of direct intermediary and indirect intermediary and the other application provisions in section 2. To provide a specific reference to the Product Determination Rules in the definition of "cleared derivative" would be redundant.

"clearing services"

One commenter suggested that the definition may be overly broad and capture activities which should not be regulated as clearing services, such as services provided by introducing brokers that do not hold customer collateral.

No change. The term "clearing services" is not defined in the Instrument. However, guidance applicable to that term is provided in the CP. With respect to intermediaries that provide clearing services, the Instrument applies only to clearing intermediaries that, according to the definitions in the Instrument, require, receive or hold customer collateral.

"customer"

One commenter noted that a clearing agency may have difficulty porting a customer's position and associated collateral where there are several intermediaries between the clearing agency and the customer that is the beneficial owner of the position. The commenter suggested that the definition of customer should be limited in scope to include only direct customers of a direct intermediary (i.e., a customer of a participant of the clearing agency).

No change. Customers that clear indirectly should benefit from the same protections as those that clear directly through a direct intermediary.

"customer collateral"

One commenter requested that the definition of customer collateral distinguish between collateral that is deposited to satisfy margin requirements (i.e., initial margin) and cash or other assets that are paid or deposited to settle the change in price of an open transaction over its settlement cycle (i.e., variation margin). The commenter requested clarification on whether customer initial margin and variation margin must be segregated from the initial margin and variation margin belonging to other customers as well as from house owned initial margin and variation margin.

No change. Initial margin and variation margin must be segregated from a clearing intermediary's house account. Customer collateral is permitted to be held in an omnibus account, provided that the customer collateral for each customer is accounted for separately.

PART 2: TREATMENT OF CUSTOMER COLLATERAL BY A CLEARING INTERMEDIARY

s. 3 -- Segregation of customer collateral -- clearing intermediary

General Comments

One commenter expressed concern regarding the risk associated with perfecting a secured interest in cash collateral posted by a customer to a clearing intermediary. While the commenter supported the changes made to the Instrument, which no longer requires customer collateral to be held in a segregated account linked to the customer's name, the commenter noted the importance of amending the personal property security legislation in Canada to permit perfection by control of a security interest in cash collateral held outside a securities account.

Amendments to the personal property securities legislation are outside the jurisdiction of the CSA. However, amendments were made to the Quebec Civil Code to address this issue and the Committee supports the amendments suggested by the commenter and harmonization of personal property securities legislation across Canada.

s. 5 -- Excess margin -- clearing intermediary

General Comments

One commenter requested that the requirement for clearing service providers to identify and record each business day the value of excess margin under section 5 and section 31 be harmonized with the CFTC's regulations which only require Futures Commission Merchants (FCMs) to calculate excess margin across all customers rather than at the individual customer level.

No change. However, an exemption based on substituted compliance with CFTC and EMIR provisions is available for sections 5 and 31 of the Instrument.

s. 7 -- Investment of customer collateral -- clearing intermediary

General Comments

One commenter noted that United States laws do not require that a repurchase or reverse repurchase agreement in respect of customer collateral invested by a clearing intermediary or regulated clearing agency be confirmed in writing to the customer, contrary to section 7 or section 33, and that such a requirement may be onerous, considering that a customer bears no risk of loss on such agreement.

Change made. To harmonize with similar CFTC requirements, delivery of a written confirmation to the clearing intermediary, rather than to the customer, of the terms of a repurchase or resale transaction involving customer collateral is required in the Instrument. Additionally, the clearing intermediary must disclose to the customer in writing that its customer collateral may be invested or used by the clearing intermediary in accordance with section 7, including disclosure that any losses on the investment or use of the customer collateral will not be allocated to the customer.

PART 3: RECORDKEEPING BY A CLEARING INTERMEDIARY

s. 12 -- Retention of records -- clearing intermediary

General Comments

Commenters requested that the record time for record retention under section 12 and section 36 be reduced to five years.

No change. A seven-year retention period is common practice in Canada and is in line with timing requirements under the Limitations Act, 2002 (Ontario).

Commenters requested that record retention be measured in relation to each individual transaction to harmonize with similar requirements under United States laws. Alternatively, the commenters suggested that recordkeeping requirements be considered for substituted compliance. Clarification of what was meant by keeping records in a readily accessible location was also requested.

Change made. Record retention has been revised to operate on an individual transaction basis. However, general account information must be maintained for at least seven years after the last date upon which a customer's last derivative that is cleared by the clearing intermediary expires or terminates.

s. 13 -- Books and records -- clearing intermediary

General Comments

Commenters suggested that the information required to be recorded about customer collateral held by clearing intermediaries and regulated clearing agencies under section 13 and section 37 is too detailed for the customer segregation regime permitted by the Instrument. A concern was raised that requiring clearing intermediaries and regulated clearing agencies to identify specific items of collateral attributable to each customer may lead customers to believe specific items of collateral are individually segregated for their benefit. Commenters requested that the guidance be revised to only require recording of collateral value.

Change made. The Instrument requires a clearing intermediary or regulated clearing agency to record the value of the customer collateral received from or attributable to a customer.

PART 4: REPORTING AND DISCLOSURE BY A CLEARING INTERMEDIARY

s. 25 -- Customer collateral report -- regulatory

General Comments

Two commenters suggested that the requirement for clearing intermediaries to report posted customer collateral on Forms 94-102F1 and 94-102F2 on an individual customer basis was more burdensome than similar requirements under the CFTC's rules, where reporting on posted customer collateral is only required on an aggregate basis.

Change made. Forms 94-102F1 and 94-102F2 have been revised. A clearing intermediary is now required to report customer collateral on an aggregate basis for all customers, rather than on an individual customer basis. Additionally, a clearing intermediary is now required to report which permitted depositories hold customer collateral on its behalf but is not required to report on the value of customer collateral held at each permitted depository location.

One commenter expressed its support for section 25 to be one of the sections listed in Appendix A for which substituted compliance is available for clearing intermediaries that are in compliance with analogous rules and regulations under the Dodd-Frank Wall Street Reform and Consumer Protection Act (United States).

The reporting required under this section is of importance to Canadian securities regulatory authorities. Consequently, this section remains a residual requirement that is applicable even when substituted compliance is available.

s. 26 -- Customer collateral report -- customer

s.26(1)(b)

Two commenters requested that paragraph 26(1)(b) and paragraph 44(b) be modified to remove references to asset type and quantity of customer collateral to address the concern raised about the level of detail required to be recorded about customer collateral held by clearing intermediaries and regulated clearing agencies under section 13 and section 37.

Change made. Consistent with the changes to sections 13 and 37, the Instrument requires a clearing intermediary or regulated clearing agency to record the value of the customer collateral received from or attributable to a customer.

PART 5: TREATMENT OF CUSTOMER COLLATERAL BY A REGULATED CLEARING AGENCY

General Comments

Commenters suggested that portfolio margining and cross-margining of OTC derivatives with other products such as futures should be permitted under the Instrument because these practices confer commercial benefits for market participants without meaningfully increasing the risk of customer shortfalls in the event of a clearing intermediary's default.

No change. The Instrument prohibits the cross-margining of a customer's OTC cleared derivatives and futures positions. However, in some jurisdictions, customer protection requirements applicable to futures are equivalent to those applicable to OTC cleared derivatives; under such regimes, cross-margining may not represent a material risk to porting a customer's OTC cleared derivatives positions. Therefore, these factors will be taken into account when considering an application for discretionary relief from the prohibition on cross-margining or when making an equivalence determination of a foreign jurisdiction's regulatory requirements for the purpose of substituted compliance.

s. 28 -- Collection of initial margin

General Comments

One commenter noted that a clearing agency's rules do not prescribe the level of margin that its participants must request from its customers. Accordingly, it will not be possible for the clearing agency to monitor whether or not direct intermediaries are offsetting initial margin positions of its customers against one another.

No change. A regulated clearing agency is responsible for ensuring it receives initial margin on a gross basis from each customer.

s. 30 -- Holding of customer collateral -- regulated clearing agency

General Comments

One commenter requested the Instrument explicitly permit commingling and the use of omnibus accounts directly in section 30.

No change. We refer to the guidance in section 30 of the CP, which states that the customer collateral of multiple customers held by a regulated clearing agency may be commingled in an omnibus customer account if the customer collateral is segregated by each customer on a recordkeeping basis. Additionally, the recordkeeping obligations in the Instrument require the regulated clearing agency to identify the value of customer collateral held for each customer within an omnibus account.

s.30(2)

One commenter requested clarification on whether separate accounts are required for each type of customer collateral (e.g., initial margin, variation margin) as well as for any property of the customer held by the regulated clearing agency related to transactions outside of the scope of the Instrument (e.g., exchange-traded derivatives).

Change made. All types of customer collateral can be commingled in an omnibus account with the customer collateral of other customers.

Additionally, guidance has been added to the CP clarifying that a regulated clearing agency is required to hold customer collateral relating to cleared derivatives separately from any other type of property that is not customer collateral, including any other property posted by a customer as collateral relating to another investment or financial instrument that is not a cleared derivative. For example, the customer collateral of a customer may be commingled in an omnibus account with the customer collateral of other customers but may not be commingled with collateral relating to a futures contract that belongs to the customer or another customer.

s. 32 -- Use of customer collateral -- regulated clearing agency

General Comments

Commenters noted that section 32 prevents cross-margining of futures and OTC swaps and requested that cross-margining be permitted where a Canadian counterparty is interacting with a clearing agency in foreign jurisdictions where cross-margining is permitted. It was requested the Committee consider that clearing agencies would need to implement manual controls to prevent Canadian counterparties from accessing cross-margined offerings and that Canadian counterparties would be subject to significantly higher margin requirements if their futures and OTC swaps could not be commingled and cross-margined.

No change. The Instrument prohibits the cross-margining of a customer's OTC cleared derivatives and futures positions. However, in some jurisdictions, customer protection requirements applicable to futures are equivalent to those applicable to OTC cleared derivatives; under such regimes, cross-margining may not represent a material risk to porting a customer's OTC cleared derivatives positions. Therefore, these factors will be taken into account when considering an application for discretionary relief from the prohibition on cross-margining or when making an equivalence determination of a foreign jurisdiction's regulatory requirements for the purpose of substituted compliance.

s. 33 -- Investment of customer collateral -- regulated clearing agency

General Comments

One commenter requested that investment losses be borne solely by the clearing agency. The commenter noted that equivalent provisions in the CFTC regulations do not permit mutualisation of investment losses among clearing agency members and requested clarification on the risk management and policy reasons for permitting mutualisation of investment losses among clearing members.

No change. There is no requirement in section 7 or section 33 that losses be shared among clearing intermediaries.

PART 6: RECORDKEEPING BY A REGULATED CLEARING AGENCY

s. 36 -- Retention of records -- regulated clearing agency

General Comments

Clarification of the scope of records required to be retained by regulated clearing agencies was requested. The commenter suggested that the customer information collected by a clearing intermediary and shared with a regulated clearing agency under section 24 should be retained only by the clearing intermediary in accordance with section 12.

Change made. The Instrument does not require a regulated clearing agency to retain records related to a cleared derivative after the cleared derivative is terminated. Clearing intermediaries are required to maintain records related to customers and individual cleared derivatives for at least 7 years after termination; thus, it would be redundant for both clearing intermediaries and regulated clearing agencies to keep these records for an extended period after termination.

s. 37 -- Books and records -- regulated clearing agency

General Comments

A concern was raised that requiring clearing intermediaries and regulated clearing agencies to identify specific items of collateral attributable to each customer may cause customers to believe specific items of collateral are individually segregated for their benefit.

Change made. The Instrument requires a regulated clearing agency to record the value of the customer collateral received from or attributable to a customer.

s. 38 -- Separate records -- regulated clearing agency

s. 38(b)

One commenter noted that under United States laws, a derivatives clearing organization (DCO) must only record the value of customer collateral held by the DCO in satisfaction of its margin requirements and is not required to record the value of excess margin. The commenter requested that paragraph 38(b) not apply to non-Canadian clearing agencies subject to different regulatory requirements and which have built operation systems accordingly.

Change made. Section 31 of the Instrument has been revised and requires a regulated clearing agency to record the value of excess margin it holds for a clearing intermediary on behalf of its customers.

Additionally, an exemption based on substituted compliance is available to regulated clearing agencies that act in accordance with CFTC or EMIR requirements.

s. 38(b)

One commenter requested that paragraph 38(b) be revised to clarify that clearing agencies are not required to distinguish the value of customer collateral on an individually segregated basis (i.e., it can be recorded within an omnibus customer account).

No change. Customer collateral can be held within an omnibus account but the value of customer collateral attributable to each customer must be recorded.

s. 38(b) and (c)

One commenter requested that to align with the CFTC's approach to the treatment of non-US indirect intermediary's accounts, the Instrument should provide for substituted compliance for paragraphs 38(b) and (c) and clarify that paragraphs 38(b) and (c) apply only to a clearing intermediary in respect of local counterparties (not all of their customers).

Change made. An exemption based on substituted compliance is available to regulated clearing agencies that act in accordance with CFTC or EMIR requirements.

Otherwise, section 2 of the Instrument provides that the requirements under the Instrument are applicable to a regulated clearing agency that has its head office or principal place of business in a foreign jurisdiction only in respect of clearing services provided for local customers (i.e., customers located or organized in Canada). Section 2 also provides that the requirements under the Instrument applicable to clearing intermediaries apply only in respect of clearing services provided to local customers.

PART 7: REPORTING AND DISCLOSURE BY A REGULATED CLEARING AGENCY

s. 41 -- Disclosure to direct intermediaries by regulated clearing agency

General Comments

One commenter requested that for clearing agencies subject to United States laws, substituted compliance be available to permit reliance on the existing disclosures by clearing agencies under Part 39.37 of the CFTC's rules. Additionally, where a clearing agency has already made the disclosures required under the Instrument to a customer, the clearing agency should not be required to make the disclosures again after the Instrument comes into force.

Change made. Substituted compliance applies to clearing intermediaries that provide disclosure in accordance with CFTC and EMIR disclosure requirements. Additionally, the guidance in the CP providing examples of information to be included in the disclosure has been clarified.

As stated in the Notice and in the CP, where a regulated clearing agency or clearing intermediary has previously delivered disclosure to its customers that meets the requirements of the Instrument prior to the entry into force of the Instrument, new disclosure will not need to be provided to those customers.

s. 43 -- Customer collateral report -- regulatory

General Comments

One commenter suggested that the reporting requirements regarding customer collateral for regulated clearing agencies on Form 94-102F3 was more burdensome than similar requirements under the CFTC's rules.

Change made. Form 94-102F3 has been revised and a regulated clearing agency is now required to report customer collateral on an aggregate basis for all customers, rather than on an individual customer basis. Additionally, a regulated clearing agency is now required to report which permitted depositories hold customer collateral on its behalf but is not required to report on the value of customer collateral held at each permitted depository location.

The reporting required under this section is of importance to Canadian securities regulatory authorities. Consequently, this section remains a residual requirement that is applicable even when substituted compliance is available.

PART 8: TRANSFER OF POSITIONS

s. 46 -- Transfer of customer collateral and positions

General Comments

One commenter noted that the contractual obligation between a clearing agency and its direct participant to comply with the rules of the clearing agency does not extend to a customer of the direct participant. Consequently, the clearing agency is not in a position to assess if the direct participant's customer has defaulted on its obligation.

Change made. The CP has been revised at section 24 to explain that the clearing intermediary would be responsible for providing information on customer default.

s. 46(1)

Two commenters requested that subsection 46(1) be modified to include "to the extent practicable" to address explicitly the challenges associated with discharging the obligations created by this provision.

Change made. Section 46 has been revised in the Instrument to address the challenges associated with the obligations created by the provision. These changes include specifying different requirements for transfers of a customer's positions and customer collateral in a default scenario or by request of the customer in a business-as-usual scenario.

s. 46(3)(a)

Two commenters suggested that paragraph 46(3)(a) be revised to reflect the fact that customer consent to transfer collateral and positions will not always be obtained in certain default scenarios which rely on negative consent.

Change made. Regulated clearing agencies are obligated to make reasonable efforts to ensure the transfer of a customer's collateral and positions is facilitated in accordance with the customer's instructions. Guidance on this point has been added to the CP.

PART 9: SUBSTITUTED COMPLIANCE

General Comments

In making its conclusions regarding which provisions in the Instrument will benefit from substituted compliance, one commenter encouraged assessing foreign customer protection rules using an outcomes-based approach, such that foreign rules would qualify for substituted compliance where the same level of overall protection is achieved even if the foreign rules are not exactly the same as the requirements under the Instrument.

Change made. An outcomes-based approach was used to make the substituted compliance determinations included in the Instrument.

Commenters requested that the Instrument permit substituted compliance on a holistic basis whereby the OTC derivatives customer clearing regimes of foreign jurisdictions would be recognized in their entirety. Where certain parts of a foreign jurisdiction's customer clearing regime are insufficient, it was suggested that additional conditions be imposed such that compliance with the Instrument is required for those particular provisions.

Change made. An outcomes-based approach was used to make the substituted compliance determinations included in the Instrument. On an outcomes basis, it was determined that certain provisions in the Instrument did not have equivalent provisions in the customer clearing regimes used in the foreign jurisdictions that we have reviewed. Accordingly, such "residual" provisions must be complied with by foreign clearing intermediaries and regulated clearing agencies providing clearing services for local customers even when benefitting from the exemption based on substituted compliance.

{1} Manitoba Securities Commission Rule 91-506 Derivatives: Product Determination; Ontario Securities Commission Rule 91-506 Derivatives: Product Determination; Québec Regulation 91-506 respecting Derivatives Determination; and Multilateral Instrument 91-101 Derivatives: Product Determination.

List of Commenters:

1. BMO Nesbitt Burns Inc.2. The Canadian Advocacy Council for Canadian CFA Institute Societies3. Canadian Market Infrastructure Committee4. Chicago Mercantile Exchange Inc.5. Futures Industry Association, Inc.6. TMX Group Limited

ANNEX B

NATIONAL INSTRUMENT 94-102 DERIVATIVES: CUSTOMER CLEARING AND PROTECTION OF CUSTOMER COLLATERAL AND POSITIONS

PART 1 DEFINITIONS, INTERPRETATION AND APPLICATION

Definitions and interpretation

1.

(1) In this Instrument

"Canadian financial institution" has the meaning ascribed to it in National Instrument 45-106 Prospectus Exemptions;

"cleared derivative" means a derivative that is, directly or indirectly, submitted to and cleared by a clearing agency;

"clearing intermediary" means a direct intermediary or an indirect intermediary;

"customer" means a counterparty to a cleared derivative other than a clearing intermediary or a regulated clearing agency;

"customer collateral" means all cash, securities and other property if any of the following apply:

(a) the cash, securities or other property is received or held by a clearing intermediary or regulated clearing agency from, for or on behalf of a customer, and is intended to or does margin, guarantee, secure, settle or adjust a cleared derivative of the customer;

(b) the cash, securities or other property is posted on behalf of a customer by a clearing intermediary to satisfy the margin requirements arising from the customer's cleared derivatives;

"direct intermediary" means a person or company that

(a) with respect to a cleared derivative, is a participant of the regulated clearing agency at which the cleared derivative is cleared,

(b) directly provides clearing services for a customer in respect of a cleared derivative entered into by, for or on behalf of the customer, and

(c) requires, receives or holds collateral from, for or on behalf of the customer in providing clearing services;

"excess margin" means customer collateral in respect of a customer's cleared derivatives that

(a) is delivered to a regulated clearing agency or clearing intermediary from, for or on behalf of the customer, and

(b) has a value in excess of the amount required by the regulated clearing agency to clear and settle the cleared derivatives of the customer;

"indirect intermediary" means a person or company that

(a) indirectly provides clearing services for a customer in respect of a cleared derivative entered into by, for or on behalf of the customer, and

(b) requires, receives or holds collateral from, for or on behalf of the customer in providing clearing services;

"initial margin" means, in relation to a regulated clearing agency's margin system that manages credit exposures to its participants, collateral that is required by the regulated clearing agency to cover potential changes in the value of a customer's cleared derivatives over an appropriate close-out period in the event of a default;

"local customer" means a customer that, in respect of a local jurisdiction, is any of the following:

(a) an individual who is resident in the local jurisdiction;

(b) a person or company, other than an individual, to which any of the following apply:

(i) the person or company is organized under the laws of the local jurisdiction;

(ii) the head office of the person or company is in the local jurisdiction;

(iii) the principal place of business of the person or company is in the local jurisdiction;

"participant" means a person or company that has entered into an agreement with a regulated clearing agency to access the services of the regulated clearing agency and is bound by the regulated clearing agency's rules and procedures;

"permitted depository" means a person or company that is any of the following:

(a) a Canadian financial institution or Schedule III bank;

(b) a regulated clearing agency;

(c) the central bank of Canada or of a permitted jurisdiction;

(d) in Québec, a person recognized or exempt from recognition as a central securities depository under the Securities Act (Québec);

(e) a person or company

(i) whose head office or principal place of business is in a permitted jurisdiction,

(ii) that is a banking institution or trust company of a permitted jurisdiction, and

(iii) that has shareholders' equity, as reported in its most recent audited financial statements, of not less than the equivalent of $100 000 000;

(f) with respect to customer collateral that it receives from a customer or a clearing intermediary for which it provides clearing services, a registered investment dealer as defined in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations;

(g) with respect to customer collateral that it receives from a customer or a clearing intermediary for which it provides clearing services, a prudentially regulated entity

(i) whose head office or principal place of business is located outside of Canada, and

(ii) that is subject to and in compliance with the laws of a permitted jurisdiction relating to clearing services and the requiring, receiving and holding of customer collateral;

"permitted investment" means cash or a security or other financial instrument with minimal market and credit risk that is capable of being liquidated rapidly with minimal adverse price effect;

"permitted jurisdiction" means a foreign jurisdiction that is any of the following:

(a) a country where the head office or principal place of business of a Schedule III bank is located, and a political subdivision of that country;

(b) if a customer has provided express written consent to the clearing intermediary or the regulated clearing agency clearing a cleared derivative in a foreign currency, the country of origin of the foreign currency used to denominate the rights and obligations under the cleared derivative entered into by, for or on behalf of the customer, and a political subdivision of that country;

"position" means the economic interest of a counterparty in an outstanding cleared derivative at a point in time;

"prudentially regulated entity" means a person or company that is subject to and in compliance with the laws of a foreign jurisdiction that is a permitted jurisdiction under paragraph (a) of the definition of "permitted jurisdiction", relating to minimum capital requirements, financial soundness and risk management;

"qualifying central counterparty" means a person or company to which all of the following apply:

(a) it is recognized, exempt from recognition or otherwise registered or authorized to operate as a central counterparty in a jurisdiction of Canada or a foreign jurisdiction by a government or regulatory authority;

(b) it is subject to regulation that is consistent with the Principles for market infrastructures published by the Bank for International Settlements' Committee on Payments and Market Infrastructures and the International Organization of Securities Commissions in April 2012, as amended from time to time;

"regulated clearing agency" means

(a) in British Columbia, Manitoba and Ontario, a person or company recognized or exempt from recognition as a clearing agency in the local jurisdiction, and

(b) in Alberta, Newfoundland and Labrador, New Brunswick, the Northwest Territories, Nova Scotia, Nunavut, Prince Edward Island, Québec, Saskatchewan and Yukon, a person or company recognized or exempt from recognition as a clearing agency or clearing house pursuant to the securities legislation of any jurisdiction of Canada;

"Schedule III bank" means an authorized foreign bank named in Schedule III of the Bank Act (Canada);

"segregate" means to separately hold or separately account for a customer's positions or customer collateral.

(2) In this Instrument, a person or company is an affiliated entity of another person or company if one of them controls the other or each of them is controlled by the same person or company.

(3) In this Instrument, a person or company (the first party) is considered to control another person or company (the second party) if any of the following apply:

(a) the first party beneficially owns or directly or indirectly exercises control or direction over securities of the second party carrying votes which, if exercised, would entitle the first party to elect a majority of the directors of the second party, unless the first party holds the voting securities only to secure an obligation;

(b) the second party is a partnership, other than a limited partnership, and the first party holds more than 50% of the interests of the partnership;

(c) the second party is a limited partnership and the general partner of the limited partnership is the first party;

(d) the second party is a trust and the trustee of the trust is the first party.

(4) In this Instrument, in Alberta, British Columbia, New Brunswick, Newfoundland and Labrador, the Northwest Territories, Nova Scotia, Nunavut, Prince Edward Island, Saskatchewan and Yukon, "derivative" means a "specified derivative" as defined in Multilateral Instrument 91-101 Derivatives: Product Determination.

Application

2.

(1) This Instrument does not apply to any of the following:

(a) a regulated clearing agency whose head office or principal place of business is in a foreign jurisdiction except with respect to a cleared derivative entered into by, for or on behalf of a local customer;

(b) a clearing intermediary that provides clearing services except with respect to a cleared derivative entered into by, for or on behalf of a local customer.

(2) This Instrument applies to

(a) in Manitoba,

(i) a derivative other than a contract or instrument that, for any purpose, is prescribed by any of sections 2, 4 and 5 of Manitoba Securities Commission Rule 91-506 Derivatives: Product Determination not to be a derivative, and

(ii) a derivative that is otherwise a security and that, for any purpose, is prescribed by section 3 of Manitoba Securities Commission Rule 91-506 Derivatives: Product Determination not to be a security,

(b) in Ontario,

(i) a derivative other than a contract or instrument that, for any purpose, is prescribed by any of sections 2, 4 and 5 of Ontario Securities Commission Rule 91-506 Derivatives: Product Determination not to be a derivative, and

(ii) a derivative that is otherwise a security and that, for any purpose, is prescribed by section 3 of Ontario Securities Commission Rule 91-506 Derivatives: Product Determination not to be a security, and

(c) in Québec, a derivative specified in section 1.2 of Regulation 91-506 respecting derivatives determination, other than a contract or instrument specified in section 2 of that regulation.

- - - - - - - - - - - - - - - - - - - -

In each other local jurisdiction, this Instrument applies to a derivative as defined in subsection 1(4) of this Instrument. This text box does not form part of this Instrument and has no official status.

- - - - - - - - - - - - - - - - - - - -

(3) Despite subsection (2), this Instrument does not apply to an option on a security.

(4) In British Columbia, Newfoundland and Labrador, the Northwest Territories, Nunavut, Prince Edward Island and Yukon, subsection (3) does not apply to a security that is a derivative as defined in subsection 1(4).

PART 2 TREATMENT OF CUSTOMER COLLATERAL BY A CLEARING INTERMEDIARY

Segregation of customer collateral -- clearing intermediary

3.

(1) A clearing intermediary must segregate a customer's positions and customer collateral from the positions and property of other persons or companies including the positions and property of the clearing intermediary.

(2) A clearing intermediary must segregate the positions and customer collateral of a customer of an indirect intermediary from the positions and property of the indirect intermediary.

Holding of customer collateral -- clearing intermediary

4. A clearing intermediary must hold all customer collateral

(a) in one or more accounts at a permitted depository that are clearly identified as holding customer collateral, and

(b) in separate accounts from the property of all persons who are not customers.

Excess margin -- clearing intermediary

5. A clearing intermediary must at least once each business day identify and record the value of excess margin it holds that is attributable to each customer for which the clearing intermediary provides clearing services.

Use of customer collateral -- clearing intermediary

6.

(1) A clearing intermediary must not use or permit the use of customer collateral except in accordance with this section and sections 7 and 8.

(2) A clearing intermediary must not use or permit the use of customer collateral of a customer except to do any of the following:

(a) margin, guarantee, secure, settle or adjust a cleared derivative of the customer;

(b) with respect to excess margin, guarantee, secure or extend the credit of the customer.

(3) Other than with respect to excess margin used in accordance with paragraph (2)(b), a clearing intermediary must not create or permit to exist any lien or other encumbrance on a cleared derivative of a customer or customer collateral in respect of the cleared derivative unless the lien or other encumbrance secures an obligation resulting from the cleared derivative in favour of any of the following:

(a) the customer;

(b) the regulated clearing agency or clearing intermediary responsible for clearing the cleared derivative.

Investment of customer collateral -- clearing intermediary

7.

(1) A clearing intermediary must not invest customer collateral or enter into an agreement for resale or repurchase of customer collateral except in accordance with subsections (2) and (3).

(2) A clearing intermediary may

(a) invest customer collateral in a permitted investment, and

(b) enter into an agreement for resale or repurchase of customer collateral if all of the following apply:

(i) the agreement is for the resale or repurchase of a permitted investment;

(ii) the agreement is in writing;

(iii) the term of the agreement is no more than one business day, or reversal of the transaction is possible on demand;

(iv) written confirmation specifying the terms of the agreement is delivered by the counterparty to the agreement to te clearing intermediary immediately on entering into the agreement;

(v) the agreement is not entered into with an affiliated entity of the clearing intermediary.

(3) A loss resulting from an investment or use of a customer's customer collateral in accordance with subsection (1) or subsection (2) by the clearing intermediary must be borne by the clearing intermediary making the investment and not by the customer.

Use of customer collateral -- indirect intermediary default

8.

(1) A clearing intermediary must not use customer collateral of a customer of an indirect intermediary for which the clearing intermediary provides clearing services to satisfy an obligation of the indirect intermediary.

(2) Despite subsection (1), a clearing intermediary may use the customer collateral of a customer to fully or partially satisfy an obligation of an indirect intermediary that arises or is accelerated as a consequence of the indirect intermediary's default only if the obligation is attributable to a cleared derivative of the customer.

Acting as a clearing intermediary

9.

(1) A person or company must not act as a clearing intermediary for a customer unless the person or company is any of the following:

(a) a person or company that is subject to and is in compliance with the laws of a jurisdiction of Canada relating to minimum capital requirements, financial soundness and risk management;

(b) a person or company that is registered as a dealer under securities legislation in a local jurisdiction;

(c) a person or company that is

(i) a prudentially regulated entity, and

(ii) subject to and in compliance with the laws of a permitted jurisdiction relating to clearing services and the requiring, receiving and holding of customer collateral.

(2) A clearing intermediary must not provide clearing services for a customer unless the clearing services are provided in respect of derivatives that are cleared by a regulated clearing agency.

Risk management -- clearing intermediary

10. A clearing intermediary that provides or proposes to provide clearing services for an indirect intermediary must adopt and implement rules, policies or procedures reasonably designed to

(a) identify, monitor and reasonably mitigate material risks arising from the provision of clearing services, and

(b) manage a default of the indirect intermediary.

Risk management -- indirect intermediary

11.

(1) An indirect intermediary must establish and implement rules, policies or procedures reasonably designed to identify, monitor and reasonably mitigate the material risks to the clearing intermediary or its customers arising from the provision of indirect clearing services for a customer.

(2) An indirect intermediary that receives clearing services from a clearing intermediary must provide the clearing intermediary with all information reasonably required to identify, monitor and reasonably mitigate any material risks arising from the provision of indirect clearing services for customers.

PART 3 RECORDKEEPING BY A CLEARING INTERMEDIARY

Retention of records -- clearing intermediary

12.

(1) A clearing intermediary must keep a record required under this Part and Part 4, and all supporting documentation,

(a) in a readily accessible and safe location and in a durable form,

(b) in the case of a record or supporting documentation that relates to a cleared derivative, for a period of 7 years following the date on which the cleared derivative expires or is terminated, and

(c) in any other case, for a period of 7 years following the date on which a customer's last cleared derivative that is cleared for or on behalf of the customer through the clearing intermediary expires or is terminated.

(2) Despite subsection (1), in Manitoba with respect to a customer or clearing intermediary located in Manitoba, the time period applicable to records and supporting documentation kept pursuant to subsection (1) is 8 years.

Daily records -- clearing intermediary

13.

(1) A clearing intermediary that receives customer collateral must calculate and record all of the following at least once each business day in its records:

(a) for each customer, the amount of customer collateral it requires from, for or on behalf of the customer;

(b) the total amount of customer collateral it requires from, for or on behalf of all customers.

(2) For each indirect intermediary that a clearing intermediary provides clearing services for, the clearing intermediary must calculate and record all of the following at least once each business day in its records:

(a) the amount of customer collateral it requires from, for or on behalf of each customer of each indirect intermediary;

(b) the total amount of customer collateral it requires from, for or on behalf of all customers of each indirect intermediary.

(3) For each customer, a clearing intermediary must record all of the following in its records:

(a) each permitted depository at which it holds customer collateral of the customer;

(b) calculated at least once each business day, the current value of any customer collateral received from, for or on behalf of the customer, including all of the following:

(i) any accruals on the customer collateral creditable to the customer;

(ii) any gains or losses in respect of the customer collateral;

(iii) any charges accruing to the customer;

(iv) any distributions or transfers of the customer collateral.

Daily records -- direct intermediary

14. For each customer, a direct intermediary must record all of the following at least once each business day in its records:

(a) the total amount of customer collateral required for the cleared derivatives of the customer by each regulated clearing agency;

(b) the total amount of the customer's excess margin held by the direct intermediary.

Daily records -- indirect intermediary

15. For each customer, an indirect intermediary must record all of the following at least once each business day in its records:

(a) the total amount of collateral required for the cleared derivatives of the customer by each clearing intermediary through which the indirect intermediary clears;

(b) the sum of the amounts for the customer referred to in paragraph (a);

(c) the total amount of the customer's excess margin held by the indirec intermediary.

Identifying records -- direct intermediary

16. A direct intermediary must keep records that, at any time, enable it to identify all of the following in its own accounts and in the accounts held with each regulated clearing agency through which it provides clearing services:

(a) the positions and property of the direct intermediary;

(b) the positions and value of customer collateral held for or on behalf of each of the direct intermediary's customers.

Identifying records -- indirect intermediary

17. An indirect intermediary must keep records that, at any time, enable it to identify all of the following in its own accounts and in the accounts held with each clearing intermediary through which it provides clearing services:

(a) the positions and property of the indirect intermediary;

(b) the positions and value of customer collateral held for or on behalf of each of the indirect intermediary's customers.

Identifying records -- multiple clearing intermediaries