Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

Proposed Amendments to NI 24-101 Institutional Trade Matching and Settlement, Changes to Companion Policy 24-101 Institutional Trade Matching and Settlement, and CSA Consultation Paper 24-402 Policy Considerations for Enhancing Settlement Discipline in a

Proposed Amendments to NI 24-101 Institutional Trade Matching and Settlement, Changes to Companion Policy 24-101 Institutional Trade Matching and Settlement, and CSA Consultation Paper 24-402 Policy Considerations for Enhancing Settlement Discipline in a

Proposed Amendments to

NI 24-101 Institutional Trade Matching and Settlement

and

Proposed Changes to

Companion Policy 24-101 Institutional Trade Matching and Settlement

and

CSA Consultation Paper 24-402 Policy Considerations for

Enhancing Settlement Discipline in a T+2 Settlement Cycle Environment

August 18, 2016

Part I. Introduction

The Canadian Securities Administrators (the CSA or we) are publishing for comment (the Proposed Revisions) proposed amendments to National Instrument 24-101 Institutional Trade Matching and Settlement (Instrument) and proposed changes to Companion Policy 24-101 Institutional Trade Matching and Settlement (Companion Policy) (collectively, the Instrument and Companion Policy are referred to as NI 24-101).

Some of the Proposed Revisions amend the Instrument and change the Companion Policy in anticipation of shortening the standard settlement cycle for equity and long-term debt market trades in Canada from three days after the date of a trade (T+3) to two days after the date of a trade (T+2). The move to a T+2 settlement cycle is expected to occur on September 5, 2017, at the same time as the markets in the United States move to a T+2 settlement cycle. The other Proposed Revisions are intended to clarify or modernize certain provisions of NI 24-101.

The text of the amending Instrument and Companion Policy follow after this Notice in Annexes A and B, respectively, and will also be available on websites of CSA jurisdictions, including:

www.lautorite.qc.cawww.albertasecurities.comwww.bcsc.bc.cawww.gov.ns.ca/nsscwww.nbsc-cvmnb.cawww.osc.gov.on.cawww.fcaa.gov.sk.cawww.msc.gov.mb.ca

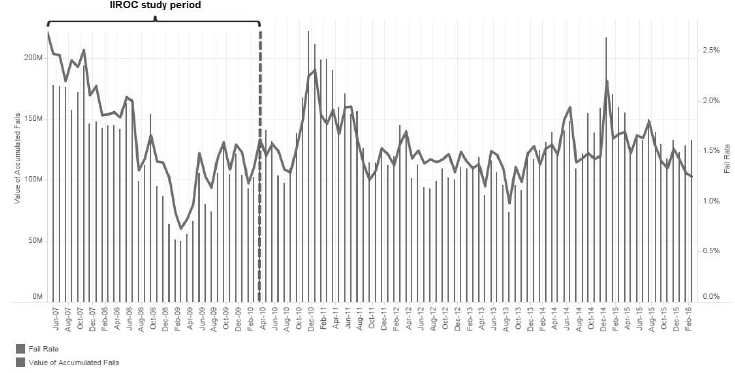

Concurrently with this Notice, we are also publishing CSA Consultation Paper 24-402 Policy Considerations for Enhancing Settlement Discipline in a T+2 Settlement Cycle Environment (Consultation Paper). The Consultation Paper provides an overview of existing settlement discipline measures in the Canadian equity and debt markets. It raises certain policy considerations for addressing the risk that the transition to a standard T+2 settlement cycle may increase settlement failures in our markets. We discuss potential measures to enhance settlement discipline, specifically in relation to NI 24-101. We are seeking stakeholder views on the Consultation Paper. Any proposal to adopt measures arising from the Consultation Paper, including a proposal to further amend NI 24-101, would require another public comment process. The Consultation Paper is set out in Annex E.

We are publishing for comment for 90 days this Notice, the Proposed Revisions and the Consultation Paper. The comment period will expire on November 16, 2016. See below under "7. Comment process" of Part IV.

This Notice includes the following Annexes:

• Annex A: the proposed amendments to the Instrument;

• Annex B: the proposed changes to the Companion Policy;

• Annex C: Blackline version of the Instrument reflecting the proposed amendments to the Instrument;

• Annex D: Blackline version of the Companion Policy reflecting the proposed changes to the Companion Policy;

• Annex E: the Consultation Paper;

• Annex F: Local Matters (where applicable).

Part II. Background to, and purpose of Proposed Revisions

1. Introduction to NI 24-101

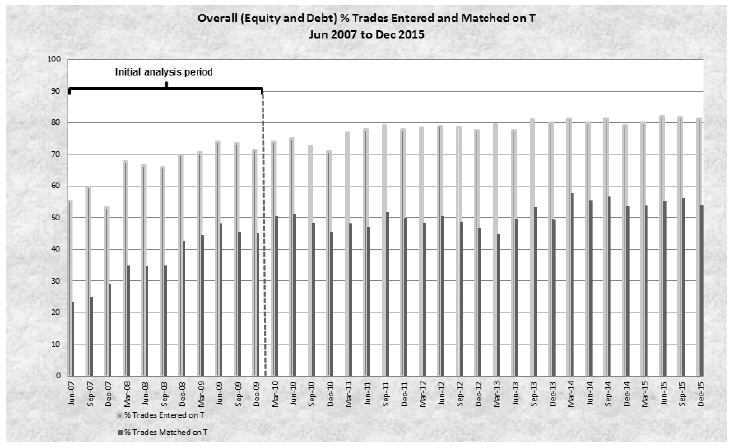

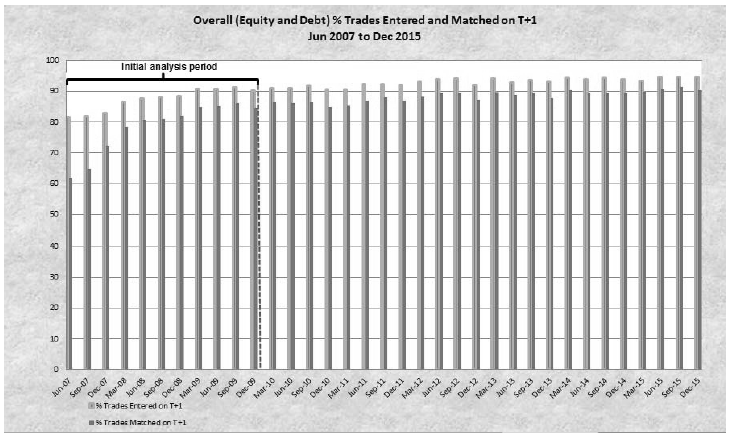

NI 24-101 came into force in 2007 and was developed largely to encourage more efficient and timely pre-settlement confirmation, affirmation, trade allocation and settlement instructions processes for institutional trades in Canada, otherwise described in this Notice as institutional trade matching (ITM).

Registered dealers and advisers trading on a DAP/RAP basis for or with an institutional investor must have ITM policies and procedures designed to match a DAP/RAP trade as soon as practical after the trade is executed, but no later than noon on T+1 (ITM deadline).{1} In addition, registered firms are required to complete and file exception reports on Form 24-101F1 if they did not meet, with respect to their institutional trades, the ITM threshold of 90 percent (ITM threshold) of trades by value and volume matched by the ITM deadline during a calendar quarter. Clearing agencies (in particular, CDS Clearing and Depository Services Inc. (CDS)) and matching service utilities (MSUs) are required to submit quarterly data on the matching of institutional equity and debt trades of their participants or users.

For more background information on NI 24-101, including its history and regulatory objective, please see the Consultation Paper being published concurrently with this Notice.

2. Migration to T+2 settlement cycle

The Canadian securities industry is preparing for the migration to a standard T+2 settlement cycle on September 5, 2017, at the same time as the industry in the United States is moving to T+2. For further information on the move to a T+2 settlement cycle, please see the Consultation Paper being published concurrently with this Notice.

For a successful migration to T+2 settlement, registered firms and other capital market stakeholders will need to review and change, as required, their current clearing and settlement procedures and internal operations and processes. In addition, self-regulatory organizations, marketplaces and clearing agencies will need to change various rules and procedures that specifically mandate a three day settlement cycle, that are keyed to the settlement date and require pre-settlement actions, or that generally facilitate the prompt clearance and settlement of trades.{2} While NI 24-101 does not expressly mandate a T+3 settlement cycle, nor would currently prevent the T+2 migration, there are a number of provisions that require revision to facilitate the move to a T+2 settlement cycle.

3. General reform of NI 24-101

We are proposing to update the Instrument to reflect certain developments since it came into force in 2007, as well as clarify certain existing provisions. One major development in the Canadian markets since 2007 is the significant rise in the trading of exchange-traded mutual funds (ETFs). We also propose to revise the existing requirements applicable to a MSU's systems and business continuity planning.

Part III. Summary of the Proposed Revisions

Section 1 of this Part explains our Proposed Revisions in anticipation of the transition to a T+2 settlement cycle. While we are not proposing any amendments to the ITM deadline or ITM threshold at this time, in the Consultation Paper we discuss potential substantive changes to NI 24-101 and other measures that we might consider to increase the likelihood of timely settlement, and we ask specific questions on such potential changes.

Section 2 of this Part describes modernizing and clarifying amendments to the Instrument (including the Forms) and Companion Policy. Minor amendments to modernize and clarify the Instrument, Forms and Companion Policy are not discussed.

We welcome comments from stakeholders on all aspects of such amendments.

1. Proposed Revisions as a result of T+2 migration

a) References to "T+3"

While the primary focus of the Instrument is on having ITM policies and procedures to match trades no later than noon on T+1, NI 24-101 contains a number of references to T+3. They can be found in the definitions section of the Instrument (section 1.1), the Forms 24-101F2 and F5, and Part 5 of the Companion Policy. We propose to remove these references or replace them with "T+2".

b) Non-North American trades

The Instrument permits matching to occur no later than noon on T+2 if the DAP/RAP trade results from an order to buy or sell securities received from an institutional investor whose investment decisions or settlement instructions are usually made in and communicated from a geographical region outside of the North American region (non-North American trades).{3}

We are proposing to repeal the provisions that extend the ITM deadline to noon on T+2 for non-North American trades. In our view, these provisions are no longer appropriate in a standard T+2 settlement environment. The extended deadline of noon on T+2 for non-North American trades leaves insufficient time to solve problems and avoid failed trades; instead, parties need to match earlier on T+1 regardless of the cross-border nature of the trade, so that they have time to address issues and avoid failed trades. This might require improving processes in order to match on T+1, but the move to a T+2 settlement cycle will align the securities settlement cycle in Canada with the settlement cycles of most of the major foreign markets, including the U.S. and Europe. While several of the complexities with foreign investment or cross-border transactions will continue to exist,{4} market participants will need to review their internal operations and adapt their ITM policies and procedures accordingly to meet the current ITM deadline of noon on T+1. This is consistent with the need for market participants to align their policies and procedures to meet the standard settlement in the U.S., Europe and other T+2 jurisdictions.

2. Proposed Revisions to clarify or modernize NI 24-101

a) Application to ETFs

The Instrument does not currently apply to a trade in a security of a mutual fund to which National Instrument 81-102 Investment Funds (NI 81-102) applies.{5} Mutual fund trades were originally carved out of the Instrument because traditional purchase and redemption transactions in mutual fund securities were not cleared and settled through the facilities of a clearing agency such as CDS. However, because ETFs are mutual funds and therefore subject to NI 81-102, ETF securities that are bought and sold generally just like any other stock on the secondary markets and settled on a DAP/RAP basis through the facilities of CDS, are not subject to NI 24-101.

From a policy perspective, we are of the view that a secondary-market trade in an ETF security that settles on a DAP/RAP basis through the facilities of CDS should be subject to the Instrument, particularly the trade matching requirements of the Instrument (Parts 3 and 4). Such trades bring the same risks to our markets and the clearing and settlement infrastructure that serves such markets as any other trade in equity or fixed-income securities. In addition, non-redeemable investment funds that trade on a marketplace and settle on a DAP/RAP basis through CDS are currently subject to the Instrument. We are of the view that all investment funds that are traded on a marketplace should be treated in the same way under the Instrument. Currently, CDS includes ETF trades in the calculation of the aggregate number and value of equity DAP/RAP trades entered and matched at CDS, as part of its reporting of ITM data under NI 24-101. Consequently, we believe that registered firms' ITM policies and procedures should not be materially impacted by the inclusion of ETF trades into the ITM requirements.

We are proposing to amend paragraph (f) of section 2.1 of the Instrument by clarifying that the Instrument does not apply to a trade to which Part 9 or 10 of NI 81-102 applies. Part 9 governs purchases of securities of a mutual fund from the mutual fund, and Part 10 governs redemptions of investment fund securities. Moreover, the Companion Policy and forms are being amended to clarify that DAP/RAP trades in ETFs are to be included in the exception reports under Form 24-101F1 by registered firms as "equity" DAP/RAP trades, and not as "debt" DAP/RAP trades.

b) Clearing agency

In the Instrument, "clearing agency" is defined as a recognized clearing agency in certain CSA jurisdictions, which, in 2007, seemed appropriate as CDS was the only recognized clearing agency at the time. Since 2007, CSA jurisdictions have recognized a number of additional clearing agencies operating in Canada that perform a wide variety of clearing and settlement services, which differ from, and may be broader than, the securities settlement services performed by CDS.{6} We propose to update the definition of the term to fit the context of the Instrument.

c) MSU systems and business continuity planning requirements

To mitigate the probability and effects of systems failures, Part 6 of the Instrument sets out requirements for an MSU governing its systems and business continuity planning. These requirements, adopted in 2007, were based on similar regulatory requirements applicable at the time to marketplaces, information processors and clearing agencies. Such similar provisions have since been modernized and updated so that they continue to be effective in helping ensure that systems are reliable, robust and have adequate controls. Because MSUs play an important infrastructure role in the clearing and settlement of securities transactions,{7} we propose requiring MSUs to follow existing IT practices for technology service providers.

Consequently, we are proposing to update the provisions of section 6.5 of the Instrument to mirror the provisions found in other rules applicable to marketplaces, information processors, clearing agencies and trade repositories, such as those found in National Instrument 21-101 Marketplace Operation and National Instrument 24-102 Clearing Agency Requirements. See new sections 6.6 to 6.8 of the Instrument, revised Form 24-101F3 Matching Service Utility -- Notice of Operations, and sections 4.5 to 4.8 of the Companion Policy. These include new requirements to ensure that, from a systems perspective, the launching of a new MSU or material changes made to an MSU's technology requirements are conducted according to prudent business practices and are implemented so that MSU users and service vendors have a reasonable opportunity to adapt to these changes. An MSU beginning operations or making a material change to its systems can negatively impact many other parties if these actions are not carried out in a careful manner.

d) Amendments to Form 24-101F1 Registered Firm Exception Report of DAP/RAP Trade Reporting and Matching

To avoid the quarterly exception reporting requirement in Part 4 of the Instrument, a registered firm must have matched during a calendar quarter at least 90 percent of its DAP/RAP trades by volume or value by noon on T+1. Form 24-101F1 (Form F1) should only be submitted for DAP/RAP trades for the type of security (equity or debt) that did not meet the 90 percent threshold by the relevant timeline. If a registered firm does not meet the threshold for both equity and debt DAP/RAP trades, then it should submit Form F1 for both equity and debt DAP/RAP trades (i.e., by completing both tables in Exhibit A of Form F1). If the firm does not meet the threshold only for one type of security (i.e., for equity but not debt, or for debt but not equity), it should only submit Form F1 for the one type of security, by completing only one of the tables in Exhibit A of Form F1. As noted above, a DAP/RAP trade in an ETF security should be reported as an equity DAP/RAP trade, and not as a debt DAP/RAP trade. We are proposing amendments to Form F1 and Companion Policy to clarify this approach to completing Form F1.

Part IV. Other Matters

1. Authority for Instrument

In those jurisdictions in which amendments to the Instrument will be adopted, securities legislation provides the securities regulatory authority with authority in respect of the subject matter of the Instrument. See Annex F, where applicable.

2. Alternatives considered to the Proposed Revisions

The alternative to the Proposed Revisions would be not to proceed with making amendments to the Instrument or changes to the Companion Policy to facilitate the move to T+2 settlement or to clarify and update provisions in the Instrument that are unclear or outdated. Not proceeding with the T+2 related Proposed Revisions would generally be inconsistent with the desire to facilitate the move to T+2. In addition, without the proposed amendments to clarify and update the Instrument, there would be less certainty and clarity with respect to the application and interpretation of NI 24-101. Moreover, not updating the MSU systems and business continuity planning requirements could have adverse consequences to our markets. See discussion below under "4. Anticipated costs and benefits".

3. Unpublished materials

In proposing revisions to the Instrument and Companion Policy, we have not relied on any significant unpublished study, report, or other material.

4. Anticipated costs and benefits

As noted above, not proceeding with the T+2 related Proposed Revisions would generally be inconsistent with the desire to facilitate the move to T+2. See the Consultation Paper, which discusses the importance of ensuring that the transition in Canada to a standard T+2 settlement cycle occurs simultaneously with the move to T+2 by the securities industry in the United States. Also, the Proposed Revisions to clarify and update the Instrument would bring more certainty and clarity with respect to the application and interpretation of NI 24-101. In addition, updating the MSU systems and business continuity planning requirements will promote more reliable and robust MSU controls and is consistent with requirements imposed on other market infrastructures that pose similar risks to the integrity of Canadian capital markets. The failure of an MSU's systems could have wide-reaching and unintended consequences.

5. CSA Staff Notice 24-305

If the Proposed Revisions are made following the comment process, CSA Staff intend to update and republish CSA Staff Notice 24-305 Frequently Asked Questions About NI 24-101 -- Institutional Trade Matching and Settlement and Related Companion Policy.

6. Effective date for Proposed Revisions

If the Proposed Revisions are made following the comment process, all of the Proposed Revisions will be brought into force or, in respect of the Companion Policy, be adopted as of September 5, 2017.

7. Comment process

Please submit your comments in writing on or before November 16, 2016. If you are not sending your comments by email, please include a CD containing the submissions. Address your submission to the following CSA member commissions:

British Columbia Securities CommissionAlberta Securities CommissionFinancial and Consumer Affairs Authority of SaskatchewanManitoba Securities CommissionOntario Securities CommissionAutorité des marchés financiersNova Scotia Securities CommissionFinancial and Consumer Services Commission (New Brunswick)Office of the Attorney General, Prince Edward IslandSecurities Commission of Newfoundland and LabradorSuperintendent of Securities, YukonSuperintendent of Securities, Northwest TerritoriesSuperintendent of Securities, Nunavut

Please deliver your comments only to the addresses that follow. Your comments will be forwarded to the remaining CSA member jurisdictions.

The Secretary

Ontario Securities Commission

20 Queen Street West, 22nd Floor

Toronto, Ontario M5H 3S8

Fax: 416-593-2318

E-mail: [email protected]

Me Anne-Marie Beaudoin

Corporate Secretary

Autorité des marchés financiers

800, rue du Square-Victoria, 22e étage

C.P. 246, tour de la Bourse

Montréal (Québec) H4Z 1G3

Fax: 514-864-6381

E-mail: [email protected]

Please note that comments received will be made publicly available and posted on the Websites of certain CSA jurisdictions. We cannot keep submissions confidential because securities legislation requires that a summary of the written comments received during the comment period be published. In this context, you should be aware that some information which is personal to you, such as your e-mail and address, may appear in the websites. It is important that you state on whose behalf you are making the submission.

Questions with respect to this Notice, the Proposed Revisions, and the Consultation Paper may be referred to:

Antoinette LeungManager, Market RegulationOntario Securities CommissionTel: 416-595-8901Email: [email protected]Maxime ParéSenior Legal Counsel, Market RegulationOntario Securities CommissionTel: 416-593-3650Email: [email protected]Meg TassieSenior AdvisorBritish Columbia Securities CommissionTel: 604-899-6819Email: [email protected]Bonnie KuhnManager, Legal, Market OversightAlberta Securities CommissionTel: 403-355-3890Email: [email protected]Paula WhiteDeputy Director, Compliance and OversightManitoba Securities CommissionTel: 204-945-5195Email: [email protected]Claude GatienDirector, Clearing housesAutorité des marchés financiersTel: 514-395-0337, ext. 4341Toll free: 1-877-525-0337Email: [email protected]Martin PicardSenior Policy Advisor, Clearing housesAutorité des marchés financiersTel: 514-395-0337, ext. 4347Toll free: 1-877-525-0337Email: [email protected]Serge BoisvertSenior Policy AdvisorDirection des bourses et des OARAutorité des marchés financiersTel: 514-395-0337, ext. 4358Toll free: 1-877-525-0337Email: [email protected]Liz KutarnaDeputy Director, Capital Markets, Securities DivisionFinancial and Consumer Affairs Authority of SaskatchewanTel: 306-787-5871Email: [email protected]Jason AlcornSenior Legal CounselFinancial and Consumer Services Commission (New Brunswick)Tel: 506-643-7857Email: [email protected]

{1} See subsections 3.1(1) and 3.3(1) of the Instrument. A DAP/RAP trade is a trade in a security executed for a client account that permits settlement on a delivery against payment or receipt against payment basis through the facilities of a clearing agency, and for which settlement is completed on behalf of the client by a custodian other than the dealer that executed the trade. See the definition "DAP/RAP trade" in section 1.1 of the Instrument.

{2} On July 28, 2016, the Investment Industry Regulatory Organization of Canada (IIROC) published for comment proposed amendments to IIROC's Universal Market Integrity Rules, Dealer Member Rules, and Form 1 to facilitate the investment industry's move to T+2 settlement. See IIROC Notice 16-0177 Amendments to facilitate the investment industry's move to T+2, at: http://www.osc.gov.on.ca/documents/en/Marketplaces/iiroc_20160728_iiroc-notice-16-0177.pdf.

{3} See subsections 3.1(2) and 3.3(2). "North American region" means Canada, the United States, Mexico, Bermuda and the countries of Central America and the Caribbean. See section 1.1.

{4} Such complexities include communication lags, structural challenges, currency differences, mismatches in global settlement cycles, and time zone issues.

{5} See paragraph (f) of section 2.1.

{6} See, for example, in Ontario: http://www.osc.gov.on.ca/en/Marketplaces_clearing-agencies_index.htm

{7} See ss. 4.1(2) of the Companion Policy.

ANNEX A

PROPOSED AMENDMENTS TO NATIONAL INSTRUMENT 24-101 INSTITUTIONAL TRADE MATCHING AND SETTLEMENT

1. National Instrument 24-101 Institutional Trade Matching and Settlement is amended by this Instrument.

2. Section 1.1 is amended by

a. replacing the definition "clearing agency" with the following:

"clearing agency" means a recognized clearing agency that operates as a securities settlement system within the meaning of National Instrument 24-102 Clearing Agency Requirements;

b. in the definition "DAP/RAP trade",

i. adding the words "in a security" immediately after "means a trade", and

ii. replacing the word "made" with "completed" in paragraph (b),

c. repealing the definitions "North American region" and "T+3", and

d. replacing the semicolon at the end of the definition "T+2" with a period.

3. Section 1.2 is amended by

a. replacing in the heading of the section "Eastern Time" with "clearing agency",

b. replacing subsection (2) with the following:

For the purposes of this Instrument, in Québec, a clearing agency includes a clearing house and a settlement system within the meaning of the Québec Securities Act.

4. Paragraph 2.1(f) is replaced by the following:

(f) a trade to which Part 9 or 10 of National Instrument 81-102 Investment Funds applies,

5. Parts 3 to 8 are amended by replacing the word "shall" wherever it is found by the word "must".

6. Subsection 3.1(1) is amended by adding "Eastern Time" immediately after "12p.m. (noon)".

7. Subsection 3.1(2) is repealed.

8. Subsection 3.3(1) is amended by adding "Eastern Time" immediately after "12p.m. (noon)".

9. Subsection 3.3(2) is repealed.

10. Section 5.1 is amended by deleting the words "through which trades governed by this Instrument are cleared and settled".

11. Section 6.5 is replaced by the following:

6.5 System requirements

For each system operated by a matching service utility that supports the matching service utility's trade matching function, a matching service utility must

(a) develop and maintain

(i) an adequate system of internal controls over that system, and

(ii) adequate information technology general controls, including, without limitation, controls relating to information systems operations, information security, change management, problem management, network support and system software support,

(b) in accordance with prudent business practice, on a reasonably frequent basis, and, in any event, at least annually,

(i) make reasonable current and future capacity estimates, and

(ii) conduct capacity stress tests to determine the ability of that system to process transactions in an accurate, timely and efficient manner, and

(c) promptly notify the regulator or, in Québec, the securities regulatory authority of any material systems failure, malfunction, delay or security breach, and provide timely updates on the status of the failure, malfunction, delay or security breach, the resumption of service, and the results of the matching service utility's internal review of the failure, malfunction, delay or security breach.

12. The Instrument is further amended by adding the following sections:

6.6 Systems reviews

(1) A matching service utility must annually engage a qualified party to conduct an independent systems review and vulnerability assessment and prepare a report in accordance with established audit standards and best industry practices to ensure that the matching service utility is in compliance with paragraph 6.5(a) and paragraph 6.8(a).

(2) The matching service utility must provide the report resulting from the review conducted under subsection (1) to

(a) its board of directors, or audit committee, promptly upon the report's completion, and

(b) the regulator or, in Québec, the securities regulatory authority, by the earlier of the 30th day after providing the report to its board of directors or the audit committee or the 60th day after the calendar year end.

6.7 Matching service utility technology requirements and testing facilities

(1) A matching service utility must make available to its users, in their final form, all technology requirements regarding interfacing with or accessing the matching service utility

(a) if operations have not begun, sufficiently in advance of operations to allow a reasonable period for testing and system modification by users, and

(b) if operations have begun, sufficiently in advance of implementing a material change to technology requirements to allow a reasonable period for testing and system modification by users.

(2) After complying with subsection (1), the matching service utility must make available testing facilities for interfacing with or accessing the matching service utility

(a) if operations have not begun, sufficiently in advance of operations to allow a reasonable period for testing and system modification by users, and

(b) if operations have begun, sufficiently in advance of implementing a material change to technology requirements to allow a reasonable period for testing and system modification by users.

(3) The matching service utility must not begin operations before

(a) it has complied with paragraphs (1)(a) and (2)(a), and

(b) the chief information officer of the matching service utility, or an individual performing a similar function, has certified in writing to the regulator or, in Québec, the securities regulatory authority, that all information technology systems used by the matching service utility have been tested according to prudent business practices and are operating as designed.

(4) The matching service utility must not implement a material change to the systems referred to in section 6.5 before

(a) it has complied with paragraphs (1)(b) and (2)(b), and

(b) the chief information officer of the matching service utility, or an individual performing a similar function, has certified in writing to the regulator or, in Québec, the securities regulatory authority, that the change has been tested according to prudent business practices and is operating as designed.

(5) Subsection (4) does not apply to the matching service utility if the change must be made immediately to address a failure, malfunction or material delay of its systems or equipment and if

(a) the matching service utility immediately notifies the regulator or, in Québec, the securities regulatory authority, of its intention to make the change, and

(b) the matching service utility discloses to its users the changed technology requirements as soon as practicable.

6.8 Testing of business continuity plans

A matching service utility must

(a) develop and maintain reasonable business continuity plans, including disaster recovery plans, and

(b) test its business continuity plans, including its disaster recovery plans, according to prudent business practices and on a reasonably frequent basis and, in any event, at least annually.

13. Form 24-101F1 is amended by adding the following at the end of the text under the heading "INSTRUCTIONS:" and immediately before the heading "EXHIBITS:":

Include DAP/RAP trades in an exchange-traded fund (ETF) security in the equity DAP/RAP trades statistics. Exhibit A(1) applies only to trades in equity and ETF securities. Exhibit A(2) applies only to trades in debt and other fixed-income securities.

14. Form 24-101F1 is further amended by replacing the portion of the Form under the heading "Exhibit A -- DAP/RAP trade statistics for the quarter" and immediately before the heading "Exhibit B -- Reasons for not meeting exception reporting thresholds" with the following:

Where applicable, complete Table 1 or 2, or both, below for each calendar quarter. Deadline means noon Eastern time on T+1.

(1) Equity DAP/RAP trades (includes ETF trades)

Entered into the clearing agency by deadline (to be completed by dealers only)

Matched (to be completed by dealers and advisers)

# of trades

%

$ value of trades

%

# of trades matched

%

$ value of trades matched

%

# of trades matched by deadline

%

$ value of trades matched by deadline

%

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

(2) Debt DAP/RAP trades

Entered into the clearing agency by deadline (to be completed by dealers only)

Matched (to be completed by dealers and advisers)

# of trades

%

$ value of trades

%

# of trades matched

%

$ value of trades matched

%

# of trades matched by deadline

%

$ value of trades matched by deadline

%

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

_____

- - - - - - - - - - - - - - - - - - - -

Legend

"# of Trades" is the total number of transactions in the calendar quarter;

"$ Value of Trades" is the total value of the transactions (purchases and sales) in the calendar quarter.

- - - - - - - - - - - - - - - - - - - -

15. Form 24-101F1 is further amended by replacing references to "Companion Policy 24-101CP" under the headings "Exhibit B -- Reasons for not meeting exception reporting thresholds" and "Exhibit C -- Steps to address delays" with "Companion Policy 24-101"

16. Form 24-101F2 is amended under the heading "INSTRUCTIONS:" by

a. inserting the following paragraph immediately after the first paragraph:

Include client trades in an exchange-traded fund (ETF) security in the equity trades statistics.

b. replacing "shall" with "must" in the last sentence.

17. Form 24-101F2 is further amended in each of Table 1 (Equity trades) and Table 2 (Debt trades) under the heading and subheadings "EXHIBITS: -- 1. DATA REPORTING -- Exhibit A -- Aggregate matched trade statistics" by removing the entire row titled "T+3" and changing the title of the row titled ">T+3" with ">T+2".

18. Form 24-101F3 is amended under the heading "INSTRUCTIONS:" by

a. deleting "or 10.2(4)" in the first sentence,

b. replacing "shall" with "must" in the second paragraph,

c. deleting the last sentence of the last paragraph.

19. Form 24-101F3 is further amended under the heading "6. SYSTEMS COMPLIANCE" by

a. replacing the text of Exhibit K -- Security with the following:

Exhibit K -- General and security

Provide a high level description of the systems used to perform your services of a matching service utility, including the processes and procedures implemented by you to provide for the security of the systems.

b. replacing the text under the subheading "Exhibit M -- Business continuity" with the following:

Exhibit M -- Business continuity

Provide a brief description of your business continuity and disaster recovery plans that includes, but is not limited to, information regarding the following:

1. Where the primary processing site is located.

2. What the approximate percentage of hardware, software and network redundancy is at the primary site.

3. Any uninterruptible power source (UPS) at the primary site.

4. How frequently market data is stored off-site.

5. Any secondary processing site, the location of any such secondary processing site, and whether all of the matching service utility's critical business data is accessible through the secondary processing site.

6. The creation, management, and oversight of the plans, including a description of responsibility for the development of the plans and their ongoing review and updating.

7. Escalation procedures, including event identification, impact analysis, and activation of the plans in the event of a disaster or disruption.

8. Procedures for internal and external communications, including the distribution of information internally, to the securities regulatory authority, and, if appropriate, to the public, together with the roles and responsibilities of the matching service utility's staff for internal and external communications.

9. The scenarios that would trigger the activation of the plans.

10. How frequently the business continuity and disaster recovery plans are tested.

11. Procedures for record keeping in relation to the review and updating of the plans, including the logging of tests and deficiencies.

12. The targeted time to resume operations of critical information technology systems following the declaration of a disaster by the matching service utility and the service level to which such systems are to be restored.

13. Any single points of failure faced by the matching service utility.

c. replacing the text of "Exhibit O -- Independent systems audit" with the following:

Exhibit O -- Independent systems audit

1. Provide high level information on the qualified party engaged to provide an annual independent systems review and vulnerability assessment.

2. If applicable, provide a copy of the last systems operations audit report.

20. Form 24-101F4 is amended under the heading "INSTRUCTIONS:" by replacing "shall" with "must" in the second paragraph.

21. Form 24-101F5 is amended under the heading "INSTRUCTIONS:" by

a. adding the following paragraph after the first paragraph:

Include DAP/RAP trades in an exchange-traded fund (ETF) security in the equity DAP/RAP trades statistics.

b. replacing "shall" with "must" in the second and third sentences.

22. Form 24-101F5 is further amended under the heading "EXHIBITS" by

a. adding the text and punctuation ",malfunction, delay or security breach" immediately after "systems failures" in the sentence under the subheadings "1. SYSTEMS REPORTING -- Exhibit B -- Material systems failures reporting"

b. by removing the entire row titled "T+3" and changing the title of the row titled ">T+3" with ">T+2" in each of Table 1 (Equity trades) and Table 2 (Debt trades) under the subheadings "2. DATA REPORTING -- Exhibit C -- Aggregate matched trade statistics".

23. This Instrument comes into force on September 5, 2017.

ANNEX B

PROPOSED CHANGES TO COMPANION POLICY 24-101 INSTITUTIONAL TRADE MATCHING AND SETTLEMENT

1. Companion Policy 24-101 Institutional Trade Matching and Settlement is changed by this Document.

2. The title of the Companion Policy is simplified to read as follows:

COMPANION POLICY 24-101 INSTITUTIONAL TRADE MATCHING AND SETTLEMENT

3. Subsection 1.2(2) is changed by replacing, in the last sentence of footnote 3, the words "within one hour of the execution of the trade" with "by no later than 6 pm on the day of the trade".

4. Paragraph 1.2(3)(c) is changed by replacing footnote 5 by the following:

5 See, for example, section 14.12 of NI 31-103 and IIROC Member Rule 200.1(h).

5. Subsection 1.3(1) (including footnotes) is replaced by the following (including a footnote):

(1) Clearing agency -- While the terms "clearing agency" and "recognized clearing agency" are generally defined in securities legislation,6 we have defined clearing agency for the purposes of the Instrument to narrow its scope to a recognized clearing agency that operates as a securities settlement system. The term securities settlement system is defined in National Instrument 24-102 Clearing Agency Requirements as a system that enables securities to be transferred and settled by book entry according to a set of predetermined multilateral rules. Today, the definition of clearing agency in the Instrument applies to CDS Clearing and Depository Services Inc. (CDS). For the purposes of the Instrument, a clearing agency includes, in Quebec, a clearing house and settlement system within the meaning of the Québec Securities Act. See subsection 1.2(2). [Footnote 6: See, for example, s. 1(1) of the Securities Act (Ontario).]

6. Subsection 1.3(4) is changed by replacing, in the second sentence, the words "the Joint Financial Questionnaire and Report of the Canadian SROs" with "IIROC Form 1, Part II".

7. Section 2.2 is changed by

a. adding in the first sentence "Eastern Time" immediately after "12p.m. (noon)"

b. deleting the second and third sentences,

c. adding immediately after the first sentence the following new sentence (including a footnote):

The policies and procedures requirement of Part 3 of the Instrument is consistent with the overarching obligation of a registered firm to manage the risks associated with its business in accordance with prudent business practices.7 [Footnote 7: See s. 11.1 of NI 31-103, which requires registered firms to establish, maintain and apply policies and procedures that establish a system of controls and supervision sufficient to manage the risks associated with their business in accordance with prudent business practices.]

8. Section 3.1 is changed by

a. replacing, in the second sentence of paragraph (a), the words "a percentage target of the DAP/RAP trades" with "90 percent of the DAP/RAP trades (by volume and value)"

b. deleting the first word ("They ...") in the second sentence of paragraph (b) and inserting in its place the following text:

DAP/RAP trades in exchange-traded funds are reportable in the equities category of DAP/RAP trades.

Form 24-101F1 should only be submitted for DAP/RAP trades for the type of security (equity or debt) that did not meet the 90 percent threshold by the relevant timeline. If a registered firm does not meet the threshold for both equity and debt DAP/RAP trades, then it should submit the Form for both equity and debt DAP/RAP trades (i.e., by completing both tables in Exhibit A of Form 24-101F1). If the firm does not meet the threshold only for one type of security (i.e., for equity but not debt, or for debt but not equity), it should only submit the Form for the one type of security, by completing only one of the tables in Exhibit A of Form 24-101F1. A registered firm ...

9. Paragraph 3.2(b) is changed by

a. replacing the first sentence with the following:

The Canadian securities regulatory authorities may consider the consistent inability to meet the matching percentage target as evidence that either the policies and procedures of one or more of the trade matching parties have not been properly designed or, if properly designed, have been inadequately complied with.

b. Replacing, in the second sentence, the word "will" with "may".

10. Section 3.3 is changed by replacing the words "participants or users/subscribers" with "participants, users or subscribers".

11. Section 3.4 is changed by replacing the word "may" with "should".

12. Subsection 4.1(1) is changed by

a. deleting the first word ("The ...") in the second sentence and inserting in its place "For the purposes of the Instrument, the..."

b. adding the following text (including a footnote) immediately after the last sentence:

In Québec, a person or company that seeks to provide centralized facilities for matching must, in addition to the requirements of the Instrument, apply for recognition as a matching service utility or for an exemption from the requirement to be recognized as a matching service utility pursuant to the Securities Act (Québec, chapter V-1.1) or Derivatives Act (Québec, chapter I-14.01). In certain other jurisdictions, in addition to the requirements of the Instrument, such person or company may be required to apply either for recognition as a clearing agency or for an exemption from the requirement to be recognized as a clearing agency.10 [Footnote 10: See, for example, the scope of the definition of "clearing agency" in s. 1(1) of the Securities Act (Ontario), which includes providing centralized facilities "for comparing data respecting the terms of settlement of a trade or transaction".]

13. Section 4.2 is changed by replacing the beginning portion of the first sentence "Sections s 6.1(1) and 10.2(4) of the Instrument require ..." with "Subsection 6.1(1) of the Instrument requires".

14. Section 4.5 is replaced with the following new section 4.5, together with added new sections 4.6 to 4.8:

4.5 System requirements

(1) The intent of these provisions is to ensure that controls are implemented to support information technology planning, acquisition, development and maintenance, computer operations, information systems support, and security. Recognized guides as to what constitutes adequate information technology controls include 'Information Technology Control Guidelines' from the Canadian Institute of Chartered Accountants (CICA) and 'COBIT' from the IT Governance Institute.

(2) Capacity management requires that the matching service utility monitor, review, and test (including stress test) the actual capacity and performance of the system on an ongoing basis. Accordingly, under paragraph 6.5(b), the matching service utility is required to meet certain standards for its estimates and for testing. These standards are consistent with prudent business practice. The activities and tests required in that paragraph are to be carried out at least once a year. In practice, continuing changes in technology, risk management requirements and competitive pressures will often result in these activities being carried out or tested more frequently.

(3) A failure, malfunction or delay or other incident is considered to be "material" if the matching service utility would, in the normal course of operations, escalate the matter to or inform its senior management ultimately accountable for technology. It is also expected that, as part of this notification, the matching service utility will provide updates on the status of the failure and the resumption of service. Further, the matching service utility should have comprehensive and well-documented procedures in place to record, report, analyze, and resolve all operational incidents. In this regard, the matching service utility should undertake a "post-incident" review to identify the causes and any required improvement to the normal operations or business continuity arrangements. Such reviews should, where relevant, include the matching service utility's participants. The results of such internal reviews are required to be communicated to the securities regulatory authority as soon as practicable. Paragraph 6.5(c) also refers to a material security breach. A material security breach or systems intrusion is considered to be any unauthorized entry into any of the systems that support the functions of the matching service utility or any system that shares resources with one or more of these systems. Virtually any security breach would be considered material and thus reportable to the securities regulatory authority. The onus would be on the matching service utility to document the reasons for any security breach it did not consider material.

4.6 Systems reviews

(1) A qualified party is a person or a group of persons with relevant experience in both information technology and in the evaluation of related internal systems or controls in a complex information technology environment. Qualified persons may include external auditors or third party information system consultants, as well as employees of the matching service utility or an affiliated entity of the matching service utility, but may not be persons responsible for the development or operation of the systems or capabilities being tested. Before engaging a qualified party, a matching service utility should discuss its choice with the regulator or, in Québec, the securities regulatory authority.

4.7 Matching service utility technology requirements and testing facilities

(1) The technology requirements required to be disclosed under subsection 6.7(1) do not include detailed proprietary information.

(2) We expect the amended technology requirements to be disclosed as soon as practicable, either while the changes are being made or immediately after.

4.8 Testing of business continuity plans

(1) Paragraph 6.8 (a) of the Instrument requires that matching service utility develop and maintain reasonable business continuity plans, including disaster recovery plans. Business continuity planning should encompass all policies and procedures to ensure uninterrupted provision of key services regardless of the cause of potential disruption. In fulfilling the requirement to develop and maintain reasonable business continuity plans, the Canadian securities regulatory authorities expect that matching service utilities are to remain current with best practices for business continuity planning and to adopt them to the extent that they address their critical business needs.

(2) A matching service utility's business continuity plan and its associated arrangements should be subject to frequent review and testing. At a minimum, under paragraph 6.8(b), such tests must be conducted annually. Tests should address various scenarios that simulate wide-scale disasters and inter-site switchovers. The matching service utility's employees should be thoroughly trained to execute the business continuity plan and participants, critical service providers, and linked clearing agencies should be regularly involved in the testing and be provided with a general summary of the testing results. The CSA expects that the matching service utility will also facilitate and participate in industry-wide testing of the business continuity plan. The matching service utility should make appropriate adjustments to its business continuity plan and associated arrangements based on the results of the testing exercises.

15. Section 5.1 is changed by

a. replacing, in the second sentence, "T+3" with "T+2"

b. renumbering footnote 10 to 11.

16. This Document becomes effective as of September 5, 2017.

ANNEX C

BLACKLINE VERSION OF NI 24-101 REFLECTING PROPOSED AMENDMENTS

CANADIAN SECURITIES ADMINISTRATORS

NATIONAL INSTRUMENT 24-101 INSTITUTIONAL TRADE MATCHING AND SETTLEMENT

TABLE OF CONTENTS

|

<<PART>> |

<<TITLE>> |

|

|

|

|

PART 1 |

DEFINITIONS AND INTERPRETATION |

|

|

|

|

PART 2 |

APPLICATION |

|

|

|

|

PART 3 |

TRADE MATCHING REQUIREMENTS |

|

|

|

|

PART 4 |

REPORTING BY REGISTERED FIRMS |

|

|

|

|

PART 5 |

REPORTING REQUIREMENTS FOR CLEARING AGENCIES |

|

|

|

|

PART 6 |

REQUIREMENTS FOR MATCHING SERVICE UTILITIES |

|

|

|

|

PART 7 |

TRADE SETTLEMENT |

|

|

|

|

PART 8 |

REQUIREMENTS OF SELF-REGULATORY ORGANIZATIONS AND OTHERS |

|

|

|

|

PART 9 |

EXEMPTION |

|

|

|

|

PART 10 |

EFFECTIVE DATES AND TRANSITION |

|

|

|

|

<<FORMS>> |

<<TITLE>> |

|

|

|

|

24-101F1 |

REGISTERED FIRM EXCEPTION REPORT OF DAP/RAP TRADE REPORTING AND MATCHING |

|

|

|

|

24-101F2 |

CLEARING AGENCY -- QUARTERLY OPERATIONS REPORT OF INSTITUTIONAL TRADE REPORTING AND MATCHING |

|

|

|

|

24-101F3 |

MATCHING SERVICE UTILITY -- NOTICE OF OPERATIONS |

|

|

|

|

24-101F4 |

MATCHING SERVICE UTILITY -- NOTICE OF CESSATION OF OPERATIONS |

|

|

|

|

24-101F5 |

MATCHING SERVICE UTILITY -- QUARTERLY OPERATIONS REPORT OF INSTITUTIONAL TRADE REPORTING AND MATCHING |

NATIONAL INSTRUMENT 24-101 INSTITUTIONAL TRADE MATCHING AND SETTLEMENT

PART 1 DEFINITIONS AND INTERPRETATION

1.1 Definitions --

In this Instrument,

"clearing agency" means

,a recognized clearing agency that operates as a securities settlement system within the meaning of National Instrument 24-102 Clearing Agency Requirements;

(a) in Ontario, a clearing agency recognized by the securities regulatory authority under section 21.2 of the Securities Act (Ontario),

(b) in Québec, a clearing house for securities recognized by the securities regulatory authority, and

(c) in every other jurisdiction, an entity that is carrying on business as a clearing agency in the jurisdiction;"custodian" means a person or company that holds securities for the benefit of another under a custodial agreement or other custodial arrangement;

"DAP/RAP trade" means a trade in a security

(a) executed for a client trading account that permits settlement on a delivery against payment or receipt against payment basis through the facilities of a clearing agency, and

(b) for which settlement is

madecompleted on behalf of the client by a custodian other than the dealer that executed the trade;"institutional investor" means a client of a dealer that has been granted DAP/RAP trading privileges by the dealer;

"marketplace" has the same meaning as in National Instrument 21-101 Marketplace Operation;

"matching service utility" means a person or company that provides centralized facilities for matching, but does not include a clearing agency;

"North American region" means Canada, the United States, Mexico, Bermuda and the countries of Central America and the Caribbean;"registered firm" means a person or company registered under securities legislation as a dealer or adviser;

"trade-matching agreement" means, for trades executed with or on behalf of an institutional investor, a written agreement entered into among trade-matching parties setting out the roles and responsibilities of the trade-matching parties in matching those trades and including, without limitation, a term by which the trade-matching parties agree to establish, maintain and enforce policies and procedures designed to achieve matching as soon as practical after a trade is executed;

"trade-matching party" means, for a trade executed with or on behalf of an institutional investor,

(a) a registered adviser acting for the institutional investor in processing the trade,

(b) if a registered adviser is not acting for the institutional investor in processing the trade, the institutional investor unless the institutional investor is

(i) an individual, or

(ii) a person or company with total securities under administration or management not exceeding $10 million,

(c) a registered dealer executing or clearing the trade, or

(d) a custodian of the institutional investor settling the trade;

"trade-matching statement" means, for trades executed with or on behalf of an institutional investor, a signed written statement of a trade-matching party confirming that it has established, maintains and enforces policies and procedures designed to achieve matching as soon as practical after a trade is executed;

"T" means the day on which a trade is executed;

"T+1" means the next business day following T;

"T+2" means the second business day following T

;"T+3" means the third business day following T.

1.2 Interpretation -- trade matching and Eastern Time -- clearing agency

(1) In this Instrument, matching is the process by which

(a) the details and settlement instructions of an executed DAP/RAP trade are reported, verified, confirmed and affirmed or otherwise agreed to among the trade-matching parties, and

(b) unless the process is effected through the facilities of a clearing agency, the matched details and settlement instructions are reported to a clearing agency.

(2) Unless the context otherwise requires, a reference in this Instrument toFor the purposes of this Instrument, in Québec, a clearing agency includes a clearing house and a settlement system within the meaning of the Québec Securities Act.

(a) a time is to Eastern Time, and

(b) a day is to a twenty-four hour day from midnight to midnight Eastern Time.

PART 2 APPLICATION

2.1 This Instrument does not apply to

(a) a trade in a security of an issuer that has not been previously issued or for which a prospectus is required to be sent or delivered to the purchaser under securities legislation,

(b) a trade in a security to the issuer of the security,

(c) a trade made in connection with a take-over bid, issuer bid, amalgamation, merger, reorganization, arrangement or similar transaction,

(d) a trade made in accordance with the terms of conversion, exchange or exercise of a security previously issued by an issuer,

(e) a trade that is a securities lending, repurchase, reverse repurchase or similar financing transaction,

(f) a trade

in a security of a mutual fundto which Part 9 or 10 of National Instrument 81-102--MutualInvestment Funds applies,(g) a trade to be settled outside Canada,

(h) a trade in an option, futures contract or similar derivative, or

(i) a trade in a negotiable promissory note, commercial paper or similar short-term debt obligation that, in the normal course, would settle in Canada on T.

PART 3 TRADE MATCHING REQUIREMENTS

3.1 Matching deadlines for registered dealer --

(1) A registered dealer shallmust not execute a DAP/RAP trade with or on behalf of an institutional investor unless the dealer has established, maintains and enforces policies and procedures designed to achieve matching as soon as practical after such a trade is executed and in any event no later than 12 p.m. (noon) Eastern time on T+1.

(2) Despite subsection (1), the dealer may adapt its policies and procedures to permit matching to occur no later than 12 p.m. (noon) on T+2 for a DAP/RAP trade that results from an order to buy or sell securities received from an institutional investor whose investment decisions or settlement instructions are usually made in and communicated from a geographical region outside of the North American region.[REPEALED]

3.2 Pre-DAP/RAP trade execution documentation requirement for dealers --

A registered dealer shallmust not open an account to execute a DAP/RAP trade for an institutional investor or accept an order to execute a DAP/RAP trade for the account of an institutional investor unless its policies and procedures are designed to encourage each trade-matching party to

(a) enter into a trade-matching agreement with the dealer, or

(b) provide a trade-matching statement to the dealer.

3.3 Matching deadlines for registered adviser --

(1) A registered adviser shallmust not give an order to a dealer to execute a DAP/RAP trade on behalf of an institutional investor unless the adviser has established, maintains and enforces policies and procedures designed to achieve matching as soon as practical after such a trade is executed and in any event no later than 12 p.m. (noon) Eastern time on T+1.

(2) Despite subsection (1), the adviser may adapt its policies and procedures to permit matching to occur no later than 12 p.m. (noon) on T+2 for a DAP/RAP trade that results from an order to buy or sell securities received from an institutional investor whose investment decisions or settlement instructions are usually made in and communicated from a geographical region outside of the North American region. [REPEALED]

3.4 Pre-DAP/RAP trade execution documentation requirement for advisers --

A registered adviser shallmust not open an account to execute a DAP/RAP trade for an institutional investor or give an order to a dealer to execute a DAP/RAP trade for the account of an institutional investor unless its policies and procedures are designed to encourage each trade-matching party to

(a) enter into a trade-matching agreement with the adviser, or

(b) provide a trade-matching statement to the adviser.

PART 4 REPORTING BY REGISTERED FIRMS

4.1 Exception reporting requirement

A registered firm shallmust deliver Form 24-101F1 to the securities regulatory authority no later than 45 days after the end of a calendar quarter if

(a) less than 90 per cent of the DAP/RAP trades executed by or for the registered firm during the quarter matched within the time required in Part 3, or

(b) the DAP/RAP trades executed by or for the registered firm during the quarter that matched within the time required in Part 3 represent less than 90 per cent of the aggregate value of the securities purchased and sold in those trades.

PART 5 REPORTING REQUIREMENTS FOR CLEARING AGENCIES

5.1 A clearing agency through which trades governed by this Instrument are cleared and settled shallmust deliver Form 24-101F2 to the securities regulatory authority no later than 30 days after the end of a calendar quarter.

PART 6 REQUIREMENTS FOR MATCHING SERVICE UTILITIES

6.1 Initial information reporting --

(1) A person or company shallmust not carry on business as a matching service utility unless

(a) the person or company has delivered Form 24-101F3 to the securities regulatory authority, and

(b) at least 90 days have passed since the person or company delivered Form 24-101F3.

(2) During the 90 day period referred to in subsection (1), if there is a significant change to the information in the delivered Form 24-101F3, the person or company shallmust inform the securities regulatory authority in writing immediately of that significant change by delivering an amendment to Form 24-101F3 in the manner set out in Form 24-101F3.

6.2 Anticipated change to operations --

At least 45 days before implementing a significant change to any item set out in Form 24-101F3, a matching service utility shallmust deliver an amendment to the information in the manner set out in Form 24-101F3.

6.3 Ceasing to carry on business as a matching service utility --

(1) If a matching service utility intends to cease carrying on business as a matching service utility, it shallmust deliver a report on Form 24-101F4 to the securities regulatory authority at least 30 days before ceasing to carry on that business.

(2) If a matching service utility involuntarily ceases to carry on business as a matching service utility, it shallmust deliver a report on Form 24-101F4 as soon as practical after it ceases to carry on that business.

6.4 Ongoing information reporting and record keeping --

(1) A matching service utility shallmust deliver Form 24-101F5 to the securities regulatory authority no later than 30 days after the end of a calendar quarter.

(2) A matching service utility shallmust keep such books, records and other documents as are reasonably necessary to properly record its business.

6.5 System requirements --

For all of its core systems supportingeach system operated by a matching service utility that supports the matching service utility's trade matching function, a matching service utility shallmust

(a) develop and maintain

(i) an adequate system of internal controls over that system, and

(

a) consistentii) adequate information technology general controls, including, without limitation, controls relating to information systems operations, information security, change management, problem management, network support and system software support,(b) in accordance with prudent business practice, on a reasonably frequent basis, and, in any event, at least annually,

(i) make reasonable current and future capacity estimates, and

(ii) conduct capacity stress tests

of those systemsto determine the ability ofthe systemsthat system to process transactions in an accurate, timely and efficient manner, and(

iii) implement reasonable procedures to review and keep current the testing methodology of those systems,c) promptly notify the regulator or, in Québec, the securities regulatory authority of any material systems failure, malfunction, delay or security breach, and provide timely updates on the status of the failure, malfunction, delay or security breach, the resumption of service, and the results of the matching service utility's internal review of the failure, malfunction, delay or security breach.

(iv) review the vulnerability of those systems and data centre computer operations to internal and external threats, including breaches of security, physical hazards and natural disasters, and

6.6 Systems reviews

(v) maintain adequate contingency and business continuity plans;(b) annually cause to be performed 1) A matching service utility must annually engage a qualified party to conduct an independent systems review and writtenvulnerability assessment and prepare a report, in accordance with generally accepted auditing standards, of the stated internal control objectives of those systems; andestablished audit standards and best industry practices to ensure that the matching service utility is in compliance with paragraph 6.5(a) and paragraph 6.8(a).

(2) The matching service utility must provide the report resulting from the review conducted under subsection (1) to

(a) its board of directors, or audit committee, promptly upon the report's completion, and

(b) the regulator or, in Québec, the securities regulatory authority, by the earlier of the 30th day after providing the report to its board of directors or the audit committee or the 60th day after the calendar year end.

6.7 Matching service utility technology requirements and testing facilities

(1) A matching service utility must make available to its users, in their final form, all technology requirements regarding interfacing with or accessing the matching service utility

(a) if operations have not begun, sufficiently in advance of operations to allow a reasonable period for testing and system modification by users, and

(b) if operations have begun, sufficiently in advance of implementing a material change to technology requirements to allow a reasonable period for testing and system modification by users.

(2) After complying with subsection (1), the matching service utility must make available testing facilities for interfacing with or accessing the matching service utility

(a) if operations have not begun, sufficiently in advance of operations to allow a reasonable period for testing and system modification by users, and

(b) if operations have begun, sufficiently in advance of implementing a material change to technology requirements to allow a reasonable period for testing and system modification by users.

(3) The matching service utility must not begin operations before

(a) it has complied with paragraphs (1)(a) and (2)(a), and

(b) the chief information officer of the matching service utility, or an individual performing a similar function, has certified in writing to the regulator or, in Québec, the securities regulatory authority, that all information technology systems used by the matching service utility have been tested according to prudent business practices and are operating as designed.

(4) The matching service utility must not implement a material change to the systems referred to in section 6.5 before

(a) it has complied with paragraphs (1)(b) and (2)(b), and

(b) the chief information officer of the matching service utility, or an individual performing a similar function, has certified in writing to the regulator or, in Québec, the securities regulatory authority, that the change has been tested according to prudent business practices and is operating as designed.

(5) Subsection (4) does not apply to the matching service utility if the change must be made immediately to address a failure, malfunction or material delay of its systems or equipment and if

(a) the matching service utility immediately notifies the regulator or, in Québec, the securities regulatory authority, of its intention to make the change, and

(b) the matching service utility discloses to its users the changed technology requirements as soon as practicable.

6.8 Testing of business continuity plans

A matching service utility must

(a) develop and maintain reasonable business continuity plans, including disaster recovery plans, and

(

c) promptly notify the securities regulatory authority of a material failure of those systems.b) test its business continuity plans, including its disaster recovery plans, according to prudent business practices and on a reasonably frequent basis and, in any event, at least annually.

PART 7 TRADE SETTLEMENT

7.1 Trade settlement by registered dealer --

(1) A registered dealer shallmust not execute a trade unless the dealer has established, maintains and enforces policies and procedures designed to facilitate settlement of the trade on a date that is no later than the standard settlement date for the type of security traded prescribed by an SRO or the marketplace on which the trade would be executed.

(2) Subsection (1) does not apply to a trade for which terms of settlement have been expressly agreed to by the counterparties to the trade at or before the trade was executed.

PART 8 REQUIREMENTS OF SELF-REGULATORY ORGANIZATIONS AND OTHERS

8.1 A clearing agency or matching service utility shallmust have rules or other instruments or procedures that are consistent with the requirements of Parts 3 and 7.

8.2 A requirement of this Instrument does not apply to a member of an SRO if the member complies with a rule or other instrument of the SRO that deals with the same subject matter as the requirement and that has been approved, non-disapproved, or non-objected to by the securities regulatory authority and published by the SRO.

PART 9 EXEMPTION

9.1 Exemption --

(1) The regulator or the securities regulatory authority may grant an exemption from this Instrument, in whole or in part, subject to such conditions or restrictions as may be imposed in the exemption.

(2) Despite subsection (1), in Ontario, only the regulator may grant such an exemption.

(3) Except in Ontario, an exemption referred to in subsection (1) is granted under the statute referred to in Appendix B of National Instrument 14-101 Definitions opposite the name of the local jurisdiction.

PART 10 EFFECTIVE DATES AND TRANSITION

10.1 Effective dates

[LAPSED]

10.2 Transition

[LAPSED]

FORM 24-101F1

REGISTERED FIRM EXCEPTION REPORT OF DAP/RAP TRADE REPORTING AND MATCHING

CALENDAR QUARTER PERIOD COVERED:

From: ____________________ to: ____________________

REGISTERED FIRM IDENTIFICATION AND CONTACT INFORMATION:

1. Full name of registered firm (if sole proprietor, last, first and middle name):

2. Name(s) under which business is conducted, if different from item 1:

3a. Address of registered firm's principal place of business:

3b. Indicate below the jurisdiction of your principal regulator within the meaning of NI 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations:

[ ] Alberta

[ ] British Columbia

[ ] Manitoba

[ ] New Brunswick

[ ] Newfoundland & Labrador

[ ] Northwest Territories

[ ] Nova Scotia

[ ] Nunavut

[ ] Ontario

[ ] Prince Edward Island

[ ] Québec

[ ] Saskatchewan

[ ] Yukon

3c. Indicate below all jurisdictions in which you are registered:

[ ] Alberta

[ ] British Columbia

[ ] Manitoba

[ ] New Brunswick

[ ] Newfoundland & Labrador

[ ] Northwest Territories

[ ] Nova Scotia

[ ] Nunavut

[ ] Ontario

[ ] Prince Edward Island

[ ] Québec

[ ] Saskatchewan

[ ] Yukon

4. Mailing address, if different from business address:

5. Type of business: • Dealer • Adviser

6. Category of registration:

7.

(a) Registered Firm NRD number:

(b) If the registered firm is a participant of a clearing agency, the registered firm's CUID number:

8. Contact employee name:

Telephone number:

E-mail address:

INSTRUCTIONS:

Deliver this form for both equity and debt DAP/RAP trades together with Exhibits A, B and C pursuant to section 4.1 of the Instrument, covering the calendar quarter indicated above, within 45 days of the end of the calendar quarter if

(a) less than 90 per cent of the equity and/or debt DAP/RAP trades executed by or for you during the quarter matched within the time required in Part 3 of the Instrument, or

(b) the equity and/or debt DAP/RAP trades executed by or for you during the quarter that matched within the time required in Part 3 of the Instrument represent less than 90 per cent of the aggregate value of the securities purchased and sold in those trades.

Include DAP/RAP trades in an exchange-traded fund (ETF) security in the equity DAP/RAP trades statistics. Exhibit A(1) applies only to trades in equity and ETF securities. Exhibit A(2) applies only to trades in debt and other fixed-income securities.

EXHIBITS:

Exhibit A -- DAP/RAP trade statistics for the quarter

Complete Tables 1 and 2Where applicable, complete Table 1 or 2, or both, below for each calendar quarter. Deadline means noon Eastern time on T+1.

(1) Equity DAP/RAP trades (includes ETF trades)

|

Entered into |

Matched <<(to be completed>> by |

||||||||||

|

|

|||||||||||

|

# of |

% |

$ |

% |

# of |

% |

$ |

% |

<<# of trades matched by deadline>> |

<<%>> |

<<$ value of trades matched by deadline>> |

<<%>> |

|

|

|||||||||||

|

__________ |

_____ |

__________ |

_____ |

__________ |

_____ |

__________ |

_____ |

__________ |

_____ |

__________ |

_____ |

(2) Debt DAP/RAP trades

|

Entered into |

Matched <<(to be completed>> by |

||||||||||

|

|

|||||||||||

|

# of |

% |

$ |

% |

# of |

% |

$ |

% |

<<# of trades matched by deadline>> |

<<%>> |

<<$ value of trades matched by deadline>> |

<<%>> |

|

|

|||||||||||

|

__________ |

_____ |

__________ |

_____ |

__________ |

_____ |

__________ |

_____ |

__________ |

_____ |

__________ |

_____ |

- - - - - - - - - - - - - - - - - - - -

Legend

"# of Trades" is the total number of transactions in the calendar quarter;

"$ Value of Trades" is the total value of the transactions (purchases and sales) in the calendar quarter.

- - - - - - - - - - - - - - - - - - - -

Exhibit B -- Reasons for not meeting exception reporting thresholds

Describe the circumstances or underlying causes that resulted in or contributed to the failure to achieve the percentage target for matched equity and/or debt DAP/RAP trades within the maximum time prescribed by Part 3 of the Instrument. Reasons given could be one or more matters within your control or due to another trade-matching party or service provider. If you have insufficient information to determine the percentages, the reason for this should be provided. See also Companion Policy 24-101CP to the Instrument.

Exhibit C -- Steps to address delays

Describe what specific steps you are taking to resolve delays in the equity and/or debt DAP/RAP trade reporting and matching process in the future. Indicate when each of these steps is expected to be implemented. The steps being taken could be internally focused, such as implementing a new system or procedure, or externally focused, such as meeting with a trade-matching party to determine what action should be taken by that party. If you have insufficient information to determine the percentages, the steps being taken to obtain this information should be provided. See also Companion Policy 24-101CP to the Instrument.

CERTIFICATE OF REGISTERED FIRM

The undersigned certifies that the information given in this report on behalf of the registered firm is true and correct.

DATED at _______________ this _____ day of __________ 20_____

______________________________

(Name of registered firm -- type or print)

______________________________

(Name of director, officer or partner -- type or print)

______________________________

(Signature of director, officer or partner)

______________________________

(Official capacity -- type or print)

FORM 24-101F2

CLEARING AGENCY QUARTERLY OPERATIONS REPORT OF INSTITUTIONAL TRADE REPORTING AND MATCHING

CALENDAR QUARTER PERIOD COVERED:

From: _____________________ to: ___________________

IDENTIFICATION AND CONTACT INFORMATION:

1. Full name of clearing agency:

2. Name(s) under which business is conducted, if different from item 1:

3. Address of clearing agency's principal place of business:

4. Mailing address, if different from business address:

5. Contact employee name:

Telephone number:

E-mail address:

INSTRUCTIONS:

Deliver this form together with all exhibits pursuant to section 5.1 of the Instrument, covering the calendar quarter indicated above, within 30 days of the end of the calendar quarter.

Include client trades in an exchange-traded fund (ETF) security in the equity trades statistics.

Exhibits shallmust be provided in an electronic file, in the following file format: "CSV" (Comma Separated Variable) (e.g., the format produced by Microsoft Excel).

EXHIBITS:

1. DATA REPORTING

Exhibit A -- Aggregate matched trade statistics

For client trades, provide the information to complete Tables 1 and 2 below for each month in the quarter. These two tables can be integrated into one report. Provide separate aggregate information for trades that have been reported or entered into your facilities as matched trades by a matching service utility.

Month/Year: _____ (MMM/YYYY)

Table 1 -- Equity trades:

Entered into clearing agency by dealers

Matched in clearing agency by custodians

# of Trades

% Industry

$ Value of Trades

% Industry

# of Trades

% Industry

$ Value of Trades

% Industry

T

__________

__________

__________

__________

__________

__________

__________

__________

T+1 -- noon

__________

__________

__________

__________

__________

__________

__________

__________

T+1

__________

__________

__________

__________

__________

__________

__________

__________

T+2

__________

__________

__________

__________

__________

__________

__________

__________

T+3__________

__________

__________

__________

__________

__________

__________

__________

>T+

3<<2>>__________

__________

__________

__________

__________

__________

__________

__________

Total

__________

__________

__________

__________

__________

__________

__________

__________

Table 2 -- Debt trades:

Entered into clearing agency by dealers

Matched in clearing agency by custodians

# of Trades

% Industry