Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

CSA Staff Notice: 51-334 - Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2011

CSA Staff Notice: 51-334 - Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2011

CSA Staff Notice 51-334 - Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2011

July 15, 2011

PURPOSE OF THIS NOTICE

Reliable and accurate information by reporting issuers is critical to strengthen investor confidence and promote efficient capital markets. CSA's continuous disclosure (CD) review program is designed to identify material disclosure deficiencies that affect the reliability and accuracy of a reporting issuer's disclosure record, and has two fundamental objectives: education and compliance. This notice:

• helps issuers understand and comply with their obligations,

• summarizes the results of the CD review program for the fiscal year ended March 31, 2011 (fiscal 2011), and

• provides examples of areas of common deficiencies.

In any given year, issuers are affected by new accounting standards and regulatory changes and these are areas that we generally emphasize in our CD review program. See CSA Staff Notice 51-312 -- (Revised) Harmonized Continuous Disclosure Review Program for further details on the program.

YEAR IN REVIEW - FISCAL 2011

There are approximately 4,100 issuers in Canada, excluding investment funds and issuers that have been cease-traded. Staff of the jurisdictions of the CSA (we) use a risk based approach combined with a high level screening system to select issuers for review and to determine the type of review to conduct (full or issue-oriented). This approach allows us to address areas of particular concern. We apply both qualitative and quantitative criteria in determining the level of review required. The criteria are updated as market conditions change. We focus on accounting issues and disclosure areas where either non-compliance is probable or we foresee a need for increased compliance.

Reviews Completed

The above chart illustrates the composition of the type of reviews we conducted in fiscal 2011 compared to fiscal 2010. The number of full reviews conducted in fiscal 2011 decreased by 17% from the previous year. The number of issue-oriented reviews increased by 11%. The majority of the increase in issue-oriented reviews is a result of International Financial Reporting Standards (IFRS) transition disclosure reviews, material contract filing requirement reviews, and oil and gas technical disclosure reviews under National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities (NI 51-101).

OUTCOMES FOR FISCAL 2011

Given our risk based approach combined with a high level screening system to the selection of issuers, we generally select issuers at higher risk of non-compliance. In 2011, 70% of issuers reviewed were required to take action to improve disclosure, compared to 72% in 2010.

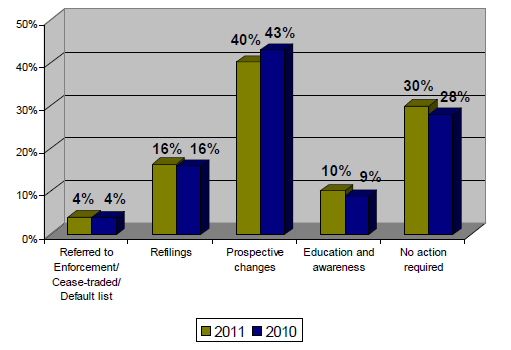

Review Outcomes 2011

We classify the outcomes of the full and issue-oriented reviews into the five categories identified below. A CD review could have more than one category of outcome. For example, an issuer could be required to refile certain documents as well as make certain changes on a prospective basis.

Enforcement referral/ Default list/ Cease trade order

If the issuer has critical CD deficiencies, we may add the issuer to our default lists, issue a cease trade order and/or refer the issuer to Enforcement.

Refiling

The issuer must amend and refile certain CD documents.

Prospective Changes

The issuer is informed that certain changes or enhancements are required in its next filing as a result of deficiencies identified.

Education and Awareness

The issuer receives a proactive letter alerting it to certain disclosure enhancements that should be considered in its next filing.

No action required

The issuer does not need to make any changes or additional filings.

FULL REVIEWS

A full review is broad in scope and covers many types of disclosure. A full review covers the issuer's most recent annual and interim financial statements, Management Discussion and Analysis (MD&A), and other disclosure documents such as:

• technical disclosure, including technical reports for oil and gas, and mining issuers;

• annual information forms (AIF);

• annual reports;

• information circulars;

• press releases, material change reports and business acquisition reports (BARs);

• website;

• CFO and CEO certifications; and

• material contracts.

ISSUE-ORIENTED REVIEWS

An issue-oriented review is an in-depth review focusing on a specific accounting, legal or regulatory issue that we believe warrants regulatory scrutiny. The nature of the issue or issues identified determines the periods we will review.

Issue-Oriented Reviews 2011

Of the 1,351 reviews that were completed in fiscal 2011, 68% of the reviews (as compared to 61% of the reviews last year) were issue-oriented reviews completed either as a CSA coordinated initiative or by local jurisdictions. Some jurisdictions did not conduct certain issue-oriented reviews but incorporated specific procedures in their full reviews to address topics or concerns identified in the issue-oriented reviews. The following issue-oriented reviews were completed this year by one or more of the jurisdictions:

IFRS Transition Disclosure

We conducted a review to assess the extent and quality of IFRS transition disclosure made by issuers in 2009 annual MD&A. We compared the disclosure of 196 issuers to the disclosure guidance provided in CSA Staff Notice 52-320 Disclosure of Expected Accounting Policies Related to the Changeover to International Financial Reporting Standards (SN 52-320). Based on the expectations of SN 52-320, 2009 annual MD&A should have provided a progress update to the issuer's changeover plan and a description of the identified accounting policy differences between the issuer's current Canadian GAAP financial statements and the IFRS policies they intended to adopt after transition. Sufficient IFRS transition disclosure would reduce investor uncertainty about transition readiness and inform users of the potential for volatility in future reported results.

Our review found that:

• 60% of issuers provided details of the key elements of their IFRS changeover plan;

• 82% of issuers provided a description of the identified accounting policy differences between the issuer's current Canadian GAAP financial statements and the IFRS policies they intend to adopt after transition; and

• issuers discussed their changeover plans and identified accounting policy differences but the discussion was often generic and did not provide the specific anticipated impact to the issuer's own financial statements and operations.

For additional reference, see CSA Staff Notice 52-326 IFRS Transition Disclosure Review.

Certification

During fiscal 2011 we conducted a follow-up review of issuers to evaluate the level of improvement in compliance with the provisions of National Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (NI 52-109). The fiscal 2011 review included the review of issuers identified in the previous fiscal year's review as not fully compliant and included the review of issuers that re-filed financial statements to correct accounting errors. Staff also reviewed the MD&A disclosure relating to the impact of the IFRS on Internal Control over Financial Reporting (ICFR) and Disclosure Control and Procedures (DC&P). The results of the fiscal 2011 review indicated moderate improvement in the level of issuers' compliance as compared to the results of the previous fiscal year's review. For the fiscal 2011 review, 22% of issuers reviewed were required to re-file their MD&A and/or the certificates compare to 30% of issuers in the previous fiscal year review. Common issues identified during this year's review include the following:

• issuers did not disclose or did not fully disclose the certifying officers' conclusion about the effectiveness of ICFR or DC&P in their MD&A or they qualified the conclusions;

• the wording on forms were amended; and

• venture issuers that filed basic certificates voluntarily discussed ICFR or DC&P in their annual MD&A but did not include cautionary language as discussed in part 15.3 of Companion Policy NI 52-109CP.

For additional reference, see CSA Staff Notice 52-327 Certification Compliance Update.

Oil and Gas Technical Disclosure

We conducted reviews on issuers engaged in oil and gas activities to assess compliance with requirements set out in NI 51-101. While there was general compliance among issuers, common issues identified include:

• Omitting some of the information required under Form 51-101F1 and disclosing units inconsistently throughout the oil and gas disclosure;

• Improper use of terminology set out in the Canadian Oil and Gas Evaluation Handbook (COGEH); and

• Boilerplate disclosure of important economic factors or significant uncertainties that affect particular components of the reserves data.

Corporate Governance Disclosure

In fiscal 2011, we conducted a follow-up review to assess compliance with National Instrument 58-101 Disclosure of Corporate Governance Practices. We reviewed the disclosure of approximately 75 reporting issuers and found that:

• 55% of the issuers reviewed were required to make prospective enhancements to their corporate governance disclosure, compared to 36% in a similar review conducted in 2007.

For additional reference, see CSA Staff Notice 58-306 2010 Corporate Governance Disclosure Compliance Review.

Material Contracts

In fiscal 2011, we completed a CD review of approximately 60 issuers to determine if they were complying with the material contract filing requirements under Part 12 of National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102). In 2008, significant changes were made to the filing requirements of material contracts. Prior to the changes, issuers were not required to file material contracts if they were entered into in the ordinary course of business. The changes do not permit the ordinary course exclusion in certain circumstances. Generally these are situations where it is determined the contract is important to understanding the issuer's business. There were also limits placed upon redaction of material contracts, where previously an issuer could redact any portion of the contract that an executive officer felt would be seriously prejudicial to the interests of the issuer or would violate confidentiality provisions. If the terms and conditions of the contract are necessary for understanding the impact of the material contract on the business of the issuer omission or redaction is not permitted.

Our review found that:

• 16% of issuers reviewed were required to file missing material contracts

• 3% of issuers reviewed were required to revise redacted provisions to comply with our requirements

Issuers should carefully consider the material contract filing rules in NI 51-102 and the related companion policy guidance. In particular, issuers should be aware that they must continually assess whether or not a given contract is material. For example, a contract that was not previously material to an issuer may become material if, due to changes in the issuer's business or other contracts, the issuer becomes substantially dependent on that contract.

Mining Technical Disclosure

Issue-oriented reviews are regularly conducted on mining technical disclosure. The following problem areas remain consistent with prior years:

• the name of the qualified person was not always included in documents containing scientific and technical information;

• required disclosure for historical estimates, such as the source and date of the estimate was not included;

• certificates or consents for the qualified person were not included; and

• corporate presentations or other content on the website did not comply with National Instrument 43-101 Standards of Disclosure for Mineral Projects.

Other

• Press Releases

Press releases, websites, corporate presentations and other promotional materials are regularly reviewed to assess compliance with NI 51-101 and COGEH disclosure requirements, and Forward-Looking Information (FLI) requirements in NI 51-102. Press releases are also reviewed to assess compliance with section 11.5 of NI 51-102 announcing a refiling or restatement (11.5 Press Release). Common issues identified include:

• non-compliant reserve and resource classification and disclosure;

• non-compliant use of oil and gas terminology;

• failure to file an 11.5 Press Release in a timely manner; and

• the common issues relating to FLI requirements identified in CSA Staff Notice 51-330 Guidance Regarding the Application of Forward-Looking Information Requirements under NI 51-102 Continuous Disclosure Obligations (SN 51-330).

• Complaints

Staff followed up on complaints referred by other areas of our respective Commissions. Complaints were also received from investors and other external stakeholders regarding specific disclosure issues. Generally, issue-oriented reviews were conducted to consider the issues raised and assess the potential impact to investors. In some circumstances, such complaints lead to further action being taken against an issuer.

COMMON DEFICIENCIES IDENTIFIED

Our reviews continue to focus on identifying material deficiencies and disclosure enhancements. To help issuers better understand their disclosure obligations we have provided guidance and examples of common deficiencies in the following appendices:

Appendix A: MD&A Deficiencies

1. Non-GAAP Financial Measures

2. Forward-Looking Information

3. Discussion of Operations

4. Liquidity

5. Fourth Quarter and Quarterly Discussion

6. Venture Issuer

Appendix B: Financial Statements Deficiencies

1. Inventory

2. Related Party Transactions

Appendix C: Regulatory Compliance Deficiencies

1. Statement of Executive Compensation (Form 51-102F6)

This is not an exhaustive list of deficiencies noted in our reviews, and issuers should be reminded that their CD record must comply with all relevant securities legislation.

AREAS OF FOCUS FOR FISCAL YEAR 2012

IFRS

For fiscal 2012, our main focus will be on IFRS transition. We will continue to use a risk based approach combined with a high level screening system to determine the issuers we will select for review and the type of review required. In addition, we will continue to be responsive to any market condition changes and address particular areas of concern in a timely manner.

Results by jurisdiction

The Alberta Securities Commission, the Ontario Securities Commission and the Autorité des marchés financiers publish reports summarizing the results of the CD review program in their jurisdictions. See the individual regulator's website for a copy of its report:

• www.albertasecurities.com

• www.osc.gov.on.ca

• www.lautorite.qc.ca

APPENDIX A

MD&A DEFICIENCIES

The quality of MD&A disclosure continues to be an area where we see deficiencies. MD&A is a narrative explanation through the eyes of management of how the issuer performed during the period covered by the financial statements, and what the issuer's financial condition and future prospects are. We often find boilerplate disclosure that does not change from period to period. Issuers frequently replicate disclosure from the financial statements without any analysis. Entity-specific disclosure provides investors with information that complements the financial statements so they are able to assess the current financial condition of the issuer and its future prospects.

There are six important areas where we continue to see boilerplate disclosure in the MD&A: non-GAAP financial measures, forward looking information (FLI), discussion of operations, liquidity, 4th quarter discussion, and venture issuer disclosure. For each, we have provided examples of deficient disclosure contrasted against more robust, entity-specific disclosure.

1. Non-GAAP Financial Measures

Issuers often provide key performance measures in continuous disclosure documents. If these measures are not permitted by an issuer's GAAP they constitute non-GAAP financial measures per CSA Staff Notice 52-306 Non-GAAP Financial Measures (SN 52-306). Note that SN 52-306 was amended in November 2010 to reflect the changeover to IFRS.

Non-GAAP financial measures are often provided in MD&A without the additional disclosure prescribed by SN 52-306. Issuers frequently omit the following disclosure:

• an explanation of why the non-GAAP financial measure is meaningful to investors and the additional purpose, if any, for which management uses the non-GAAP financial measure; and

• a clear quantitative reconciliation from the non-GAAP financial measure to the most directly comparable measure calculated in accordance with the issuer's GAAP presented in the financial statements.

In addition, issuers are reminded of their responsibility to ensure that information provided is not misleading. Therefore, adjustments should not be described as non-recurring or unusual if they are reasonably likely to occur within the next two years or have occurred in the previous two years.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

Our operating income before specific items rose 31%, reaching a new peak of $101 million.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

Our profit for the fiscal year was $50 million compared to $31 million in the previous fiscal year. Operating income before specific items (OIBI) rose 31%, reaching a new peak of $101 million. OIBI of the previous fiscal year was $77 million.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

OIBI is mainly derived from the consolidated financial statements but does not have any standardized meaning prescribed by Canadian GAAP. Therefore it is unlikely to be comparable to similar measures presented by other companies.

OIBI is used by management to evaluate the performance of its operations based on a comparable basis which excludes specific items that are non-recurring. When a specific item occurs in more than two consecutives fiscal years, it is no longer considered to be non-recurring by management.

We believe that a significant number of users of our MD&A analyze our results based on OIBI since it is a yearly comparable measure of the performance of the Company.

Reconciliation of OIBI to profit in thousands of dollars:

OIBI

$101

$77

Restructuring of distribution network

($6)

$0

Relocation of production

$0

($9)

Gross income as per financial statements

$95

$68

Sales and administrative expenses.

$23

$19

Financial expenses

$12

$9

Tax expenses

$10

$9

Profit as per financial statements

$50

$31

- - - - - - - - - - - - - - - - - - - -

2. Forward Looking Information (FLI)

Part 4A.3 of NI 51-102 sets out the disclosure requirements for FLI. Many issuers do not identify material FLI in their disclosure. Identification of material FLI is important to investors in order for them to understand that FLI is being provided. Disclosure of both the material factors or assumptions including material risk factors underlying the FLI is necessary for investors to understand that actual results may vary from FLI. Issuers continue to provide boilerplate disclosure and are reminded that the material factors or assumptions used to develop the FLI should be disclosed. Also, in light of the current transition to IFRS, issuers are reminded that Part 4B.2(2)(b) of NI 51-102 requires that FLI be based on the accounting policies that the issuer expects to use to prepare its historical financial statement for the period covered by the FLI.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

In order to attain its profitability objectives and ensure its continued operation, the Company must continue to increase cash flows from day-to-day operation. To do so, the Company expects sales to increase in 2011.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

In order to attain its profitability objectives and ensure its continued operation, the Company must continue to increase cash flows from day-to-day operation. To do so, the Company expects that the level of sales in 2011 will increase.

The following factors support management assessment about increase of sales:

• Economic recovery

• Seller network completed in the course of 2011

• Restructuration of some sale territories based on market sectors

• Customer development for private label.

Unknown risks and uncertainties could impact our expectation on sale increase such as, increase competition, pressure on sales prices and failure in launching new products. We will update our forward-looking statement for any adverse events that could materially impact management expectation of increase of sales.

- - - - - - - - - - - - - - - - - - - -

For additional reference, see SN 51-330.

3. Discussion of Operations

Issuers are required to analyze their operations in the most recently completed financial year, including a comparison against the previous completed financial year. The analysis should discuss and quantify all material variances. Common deficiencies include discussion of immaterial information without inclusion of information that maybe material to investors and insufficient analysis of why changes have occurred. Issuers are reminded that the MD&A should contain a balanced discussion of their operations. In the example below we highlight an element to be considered in the discussion of operations, the gross profit.

- - - - - - - - - - - - - - - - - - - -

Example of Deficient Disclosure

Gross profit was $75 million, compared with $100 million the preceding year.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

Gross profit for the fiscal year ended April 30, 2010 decreased by 25 percent to $75 million from $100 million for the corresponding period last year. The first eight months of the year were marked by contract cancellations and delays due to the prevailing economic situation. The unfavourable foreign exchange translation impact on gross profit for the year, when compared to the effective rates for the same period last year, is estimated at $5 million.

Canada-U.S.

Gross profit in Canada-U.S. decreased by approximately 10 million year-over-year as competitive pressures negatively affected pricing and margins. This was offset by an increase in gross profit of approximately $2 million as a result of cost cutting measures.

South and Central America

Gross profit in this geographic segment decreased significantly due to competitive pressures on pricing and higher repair costs relating to the ramp up near year end to fulfil new contracts. The impact on gross profit of each element was approximately $7 million and $1 million respectively.

- - - - - - - - - - - - - - - - - - - -

4. Liquidity

The MD&A should identify and discuss any known or expected fluctuations and trends in an issuer's liquidity, taking into account demands, commitments, events or uncertainties. Where applicable the discussion should also include disclosure of any defaults or risk of defaults on debt covenants and how the issuer intends to cure the default or otherwise address the risk as set out in the example below. The disclosure relating to expected liquidity fluctuations is required for all issuers but it is especially important when issuers have negative cash flows from operations, a negative working capital position or have breached their debt covenants.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

The Company's credit facility contains certain covenants that the Company must comply with . Otherwise the amounts outstanding are payable on demand. As at December 31, 2010 the Company violated such covenants.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

The Company's share capital is not subject to any external restrictions; however its credit facility is subject to periodic reviews. The credit facility also contains certain covenants, such that the Company cannot, without prior approval of the bank, hedge or contract petroleum or natural gas volumes, on a fixed price basis, exceeding 50 per cent of production volumes, nor can it monetize or settle any fixed price financial hedge or contract. The credit facility also contains a financial covenant that requires the Company to maintain a working capital ratio of at least 1:1. As at December 31, 2010, this ratio was 0.5:1. The bank has waived the breach and has allowed the Company six months to remedy the deficiency. The Company intends to acquire additional financing through private placements to fund current working capital needs and remedy the deficiency.

- - - - - - - - - - - - - - - - - - - -

5. Fourth Quarter and Quarterly Discussion

Issuers must discuss and analyze items or events that have had a material impact in the fourth quarter. Many issuers tend to overlook this area. Some issuers file a separate fourth-quarter MD&A and use the exemption available under section 1.10 of NI 51-102F1, however do not make appropriate reference to the separate quarterly MD&A.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

During August 2010, the Company reactivated exploration activities, initiating a drill program on its XYZ property. Also, during the fourth quarter of fiscal 2009, the Company incurred a write-down of resource properties of $1.1 million relating to the GHI property. Operating costs, excluding property write-downs, for the quarter totalled $0.2 million and consisted primarily of management salaries, management services and non-cash stock-based compensation expense.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

The Company recorded a net loss of $400,000 in the quarter compared to a net loss of $900,000 in the prior quarter. Operating expenses increased during the quarter, which was offset by foreign exchange gains of $300,000 and a tax recovery of $700,000. The increase in operating expenses is largely attributable to an increase in advisory fees and salaries of approximately $500,000. The increase in advisory fees is related to strategic alternatives that would enable financing of the ABC Project. The increase in salaries is attributable to the advancement of the ABC Project during the quarter. The Company will continue to incur operating losses until such time as the commercial development of the ABC Project results in positive earnings.

- - - - - - - - - - - - - - - - - - - -

6. Venture Issuer Disclosure

Section 5.3 of NI 51-102 requires venture issuers that have not had significant revenue from operations to provide a breakdown of material components of capitalized or expensed exploration costs. In staff's view the description of the component should be specific enough for a reader to understand its nature. For example, the descriptor "Consultant" is not specific enough for a reader to understand the nature of the costs incurred.

Furthermore, if the venture issuer's business primarily involves mining exploration, the analysis must be presented on a property-by-property basis. In some cases we have observed that venture mining issuers have not presented the required disclosure on a property by property basis.

APPENDIX B

FINANCIAL STATEMENT DEFICIENCIES

Common problems identified within the financial statements generally relate to note disclosure and measurement issues. A clear and concise description of the significant accounting policies of an issuer is considered an integral part of their financial statements as the policies provide a roadmap to investors for understanding the financial results.

Inventory and Related Party disclosure continues to be an area where we commonly see insufficient disclosure. Discussion in these areas tends to be boilerplate. In order for investors to understand the significance to the issuer's financial condition and operations we expect issuers to provide all the required disclosure. For each area we provide examples of deficient disclosure contrasted against more robust, entity-specific disclosure.

1. Inventory

The financial statement inventory note disclosure required by Part V of the CICA Handbook - Canadian GAAP (Pre-changeover Canadian GAAP) is now harmonized with IFRS. IFRS allows fewer alternatives for the measurement of inventories. It also permits reversal of write-downs, requires impairment testing at each reporting period, and has increased disclosure requirements. Issuers generally comply with the measurement of inventories but frequently do not provide all of the required disclosure.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

For the year ended December 31, 2010, the cost of sales was $1,032,485 ($984,502 in 2009). The cost of sale includes an inventory impairment reversal of $165,242 ($0 in 2009).

- - - - - - - - - - - - - - - - - - - -

Paragraph 3031.36 (g) of Pre-changeover Canadian GAAP and paragraph 36 (f) and (g) of IAS 2 Inventories requires the disclosure of the circumstances or events that led to the reversal of a write-down of inventories. In the above example, the disclosure was not provided.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

Raw materials and finished goods are recorded at the lower of average cost and net realizable value. The cost of inventory is recognized as an expense when the inventory is sold. Previous write-downs to net realizable value are reversed if there is a subsequent increase in the value of the related inventories.

- - - - - - - - - - - - - - - - - - - -

In the above example the issuer did not provide the cost formula to measure inventory as required by paragraph 3031.36 (a) of Pre-changeover Canadian GAAP and paragraph 36 (a) of IAS 2 Inventories.

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

Inventories of finished products, converted products, raw materials and materials & supplies are valued at the lower of cost and net realizable value. Costs are allocated to inventory using the weighted average cost method and include direct costs related to units of production as well as a systematic allocation of fixed and variable production overhead. Net realizable value for finished products, converted products and raw materials is considered to be the selling price of the finished product in the ordinary course of business less the estimated costs of completion and estimated costs to complete the sale. In certain circumstances, particularly pertaining to the company's materials & supplies inventories, replacement cost is considered to be the best available measure of net realizable value. Inventory is reviewed monthly to ensure the carrying value does not exceed net realizable value. If carrying value does not exceed net realizable value, a write-down is recognized immediately. The write-down may be reversed in a subsequent period if the circumstances which caused it no longer exist.

- - - - - - - - - - - - - - - - - - - -

2. Related Party Transactions

Issuers tend to be too generic in disclosure of related party transactions. Frequently, disclosure of the nature of the transaction and description of the relationship with the related party is omitted. In addition, when issuers have significant balances owing to related parties details provided in the financial statements notes do not contain all the required disclosure.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

Selling and administrative expenses includes $750,000 paid to directors and officers of the Corporation. Included in professional fees is $200,000 in fees paid and accrued to directors and officers of the Corporation. The due to related parties balance of $900,000 includes amounts owing to directors and officers of the Corporation for services rendered. The amounts owing to related parties are non-interest bearing.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

The related party payable of $900,000 at year end includes $400,000 of consulting services rendered by the Chief Information Officer in the current year for technical feasibility studies in relation to product XYZ. The remaining balance of $500,000 pertains to rent owing to an entity controlled by the Vice-President of Marketing for last 4 fiscal years. Given the Corporation's financial status, the related parties and the Corporation agreed to no fixed term for repayment.

Selling and administrative expenses includes $750,000 paid to directors and officers of the Corporation. Consulting services provided by the Chief Information Officer represents $550,000 of this expense and the balance is comprised of $200,000 in rent paid to the Vice-President of Marketing. Included in professional fees is $200,000 is fees paid to a director of the Corporation for legal services in connection with the litigation disclosed in Note 14. These related party transactions are considered to be in the normal course of business and are recorded at the exchange amount, which is considered to be equal to amounts agreed upon by the related parties.

- - - - - - - - - - - - - - - - - - - -

Issuers will have to revisit their related party transaction disclosure as part of their transition to IFRS, as the requirements differ from Pre-changeover Canadian GAAP. One of the major differences for issuers to consider is that Pre-changeover Canadian GAAP addresses both the measurement and disclosure of related party transactions, while IAS 24 Related Party Disclosures only addresses disclosure requirements. Other differences between IFRS and Pre-changeover Canadian GAAP include the following areas:

• the definition of related parties is broader under IFRS than under Pre-changeover Canadian GAAP; and

• compensation for key management personnel is a related party disclosure under IFRS, whereas executive compensation arrangements are generally not considered related party transactions under Pre-changeover Canadian GAAP but are governed by securities legislation.

APPENDIX C: REGULATORY COMPLIANCE DEFICIENCIES

The CD review program assesses issuer compliance with requirements in our securities laws. Our objective is to promote clear and informative disclosure that will allow investors to make informed investment decisions. We have identified the following areas where we continue to see lack of compliance: executive compensation and material contracts.

1. Statement of Executive Compensation (Form 51-102F6)

All direct and indirect compensation provided to certain executive officers and directors for, or in connection with, services they have provided to the issuer or subsidiary of the issuer must be disclosed. The objective of this requirement is to provide insight into executive compensation as a key aspect of the overall stewardship and governance of issuers and to help investors understand how decisions about executive compensation are made. Many issuers continue to provide insufficient disclosure of performance goals or similar conditions, as well as the benchmark group used for specific levels of compensation.

Benchmarking

Generally, benchmarking is the process of setting a target for executive compensation at a level relative to the issuer's peers. If an issuer benchmarks, it must: (i) disclose the name of all of the individual companies included in the benchmark group; and (ii) discuss why those companies were selected to be part of the peer group.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

Compensation for the named executive officers (NEOs) is composed primarily of three components: base fees, performance bonuses and stock based compensation. The determination of each component is based on industry standards. In establishing compensation, the Company takes into consideration levels of compensation provided by industry competitors.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example of entity-specific disclosure

In order to promote competitive compensation practices, the board evaluates compensation of the NEOs, relative to a peer group of 10 publicly traded Canadian companies (the "Canadian Group"). These companies are selected on the basis of a number of factors, including similar industry characteristics, revenue and market capitalization. The objective of the executive compensation policy is to position the total compensation package at the median of the Canadian Group. Each of the elements of the compensation package (base salary, short-term incentives and long-term incentives) is separately considered in the benchmarking in order to be consistent with general market practices. The 10 companies included in the Canadian Group in 2010 were: [List of companies].

The Canadian Group is reviewed on an annual basis to ensure that the inclusion criteria and companies on the list are still pertinent. Changes may be made, if necessary.

- - - - - - - - - - - - - - - - - - - -

Performance goals or similar conditions

Issuers should provide disclosure of a performance goal or similar condition that is either a quantitative or qualitative performance target achieved by the issuer on which the issuer has based its decision to award compensation. For subjective targets, the issuer may describe the target without providing specific measures. In this situation, the issuer's compensation, analysis and disclosure should clearly disclose that compensation decisions are not based on objective identifiable measures. For targets that are based on objective identifiable measures, issuers must disclose them unless a reasonable person would consider that disclosing them would seriously prejudice the issuer's interests.

- - - - - - - - - - - - - - - - - - - -

Example of deficient disclosure

To determine short term incentive compensation, the Board of Directors reviews the performance of the NEOs and considers a variety of factors, both objective and subjective, when determining compensation levels. These factors include the long-term interests of the Company and its shareholders, the financial and operating performance of the Company and each NEO's individual performance, contribution towards meeting corporate objectives, responsibilities and length of service.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example 1 of entity-specific disclosure

The compensation paid to directors and NEOs of the Company is determined on a case-by-case basis with reference to the role that each director and NEO provides to the Company. The Company does not currently prescribe a set of formal objective measures to determine discretionary bonus entitlements. Rather, the Company uses informal goals typical for development and early production stage companies such as strategic acquisitions, advancement of exploration and other transactions that serve to increase the Company's valuation. Precise goals or milestones are not pre-set by the board of directors of the Company.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Example 2 of entity-specific disclosure

Bonuses paid pursuant to the short term incentive compensation program depend on the level of achievement of financial objectives of the Company. The Company attributes to each NEO, depending on his hierarchic level, a bonus target level set as a percentage of his salary, representing the amount which will be paid if all objectives are achieved according to the targets set. Depending on the performance, actual bonuses may vary between zero and twice the target bonus, based on the level of achievement of the objectives set out at the beginning of the fiscal year.

For the fiscal year ended October 31, 2010, the financial objectives used for purposes of the short term incentive compensation were earnings per share and earnings before interest and taxes of the sector. These objectives are meant to tie the performance of the executive with the financial performance of the Company.

The following table presents the objectives for 2010 approved by the Board of Directors and the results achieved by the Company:

Performance measure

Objectives

Results

Earnings per share

$1.32

$1.50

Earnings before interest and taxes sector A (millions of dollars)

$162

$189

Earnings before interest and taxes sector B (millions of dollars)

$79

$98

Earnings before interest and taxes sector C (millions of dollars)

$83

$91

Incentive compensation as a percentage of salary:

NEO-1

NEO-2

NEO-3

NEO-4

NEO-5

Minimum

0%

0%

0%

0%

0%

Target

100%

100%

50%

75%

50%

Maximum

200%

200%

100%

100%

75%

For additional reference, see CSA Staff Notice 51-331 Report on Staff's Review of Executive Compensation Disclosure.

FOR MORE INFORMATION

Contact any of the following:

|

Alan Mayede

|

Lisa Enright

|

|

Senior Securities Analyst

|

Manager, Corporate Finance

|

|

British Columbia Securities Commission

|

Ontario Securities Commission

|

|

604-899-6546

|

416-593-3686

|

|

Toll-free 800-373-6393 (in BC and Alberta)

|

|

|

|

|

|

|

|

|

|

Ritu Kalra

|

|

|

Senior Accountant, Corporate Finance Ontario Securities Commission

|

|

|

416-593-8083

|

|

|

|

|

|

|

|

Jonathan Taylor

|

Johanne Boulerice

|

|

Manager, CD Compliance & Market Analysis

|

Manager, Continuous Disclosure

|

|

Alberta Securities Commission

|

Autorité des marchés financiers

|

|

403-297-4770

|

514-395-0337 ext. 4331

|

|

Toll-free: 1-877-525-0337, ext. 4331

|

|

|

|

|

|

|

|

|

Ian McIntosh

|

Kevin Redden

|

|

Deputy Director, Corporate Finance

|

Director, Corporate Finance

|

|

Saskatchewan Financial Services Commission

|

Nova Scotia Securities Commission

|

|

306-787-5867

|

902-424-5343

|

|

|

|

|

|

Junjie (Jack) Jiang

|

|

|

Securities Analyst, Corporate Finance Nova Scotia Securities Commission

|

|

|

902-424-7059

|

|

|

|

|

|

|

|

Bob Bouchard

|

Pierre Thibodeau

|

|

Director, Corporate Finance Manitoba Securities Commission

|

Senior Securities Analyst & Acting Chief Financial Officer

|

|

204-945-2555

|

New Brunswick Securities Commission

|

|

506-643-7751

|

|

|

|

|